The Venezuelan Parliament just passed an “enabling law” to give Socialist President Nicolas Maduro dictatorial powers.

Gee, you know what other Socialist President had his country pass an “Enabling Law” to give him dictatorial powers?

Go ahead.

Maduro’s opponents? Not happy.

Earlier this month, Maduro sent the army to seize electronics store and force them to sell goods below cost, i.e. at the laughable “official exchange rate” of 6.3 bolivars per dollar rather than the real black market rate, which is some eight times higher. (They even tried to get Twitter to block unofficial exchange rates.) And Maduro is looking to loot more stores ahead of the December 8 elections. Given that Hugo Chavez has been hollowing out the country since 1999, I’m not even sure it’s possible for the opposition to win a large enough victory to escape the margin of voter fraud anymore.

Inflation is running at 54%. Oil prices are at 16 month lows, and the country’s oil production has been declining for a while. That, and the crazy Socialist looting, have sent Venezuela bond prices into a tailspin and sent their interest rates to an all-time high. Crime is also high, with Caracas being the murder capital of the world (yes, even worse than Chicago).

Maybe that’s why Goldman Sachs has a scheme to help Venezuela swap gold for dollars.

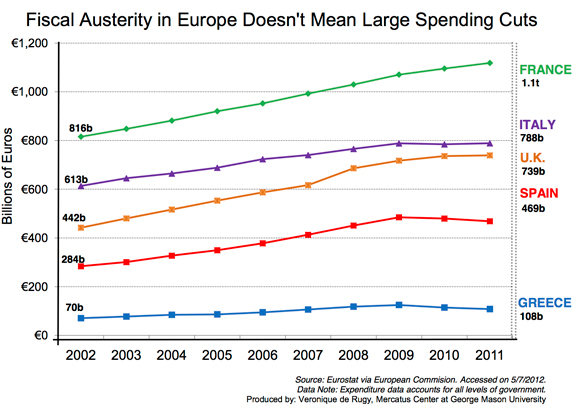

It’s almost as if Maduro read Atlas Shrugged and saw it as a blueprint rather than a cautionary tale. Imagine Greece, if hyperinflation was just getting started and they didn’t have German taxpayers to bail them out.

You can decree imaginary exchange rates the same way you can decree that π be set to exactly 3, and the reality will ignore and punish your delusion. Watch inflation skyrocket and business collapse as sellers are unable to buy goods and unwilling to sell at a loss, guaranteeing that a far-from rich country is about to get a whole lot poorer.

The only question now is whether Venezuela’s economic collapse will bee Argentina bad, or Weimar Germany bad.