Posts Tagged ‘Europe’

Sunday, June 17th, 2012

Feeling less suicidal than usual, Greek voters have opted for the conservative (for Greece) New Democracy party in parliamentary elections, beating out the radical-left Syriza, which insisted Europe keep shoveling money into the black hole that is the Greek budget, but rejected even the fake austerity the Eurocrats demanded. New Democracy leader Antonis Samaras has his work cut out for him, convincing the Eurocrats that yes, this time, they really are implementing austerity. This time for sure!

Look for this to help forestall the inevitable “grexit” for, oh, maybe three months. Which is when I bet Greece will find out it can’t pay it’s bills again after the latest infusion of cash, the money Europe kicked in will have strangely disappeared without seeming to have been spent on any fundamental government services, and insiders will have managed to transfer another few months of funds into their out-of-country banks accounts in advance of the next crisis…

Tags:2012 Election, Antonis Samaras, Budget, Elections, Euro, Europe, European Debt Crisis, Foreign Policy, Greece, grexit, Welfare State

Posted in Budget, Elections, Foreign Policy, Welfare State | No Comments »

Friday, June 15th, 2012

So Greeks head off to the polls this weekend to (theoretically) choose whether to muddle along with a “right” (for Greece) government that will actually attempt to carry out something vaguely resembling austerity, or for Alexis Tsipras’ far-left Syriza party, who intends to re-enact Clevon Little’s scene from Blazing Saddles: “Drop the austerity demands, or I’ll drop out of the Euro and refuse to let Germany bail us out anymore!” “Do what he says, do what he says, that Greek’s crazy!” It’s anybody’s guess whether Greece will opt to keep the farce going for another few months, or finally set the whole house of cards tumbling down.

My guess is that there are still enough insiders who can benefits from dumping PIIGS bonds onto various sets of European taxpayers, so I expect that, one way or another, the Eurocrats will find a way to keep the charade up for another two or three months.

In light of that, here’s a roundup of Euro debt news:

Forget grexit. The new hotness is Spexit and Spanic.

Which is why the EU just gave Spain a €100 billion life preserver. That should be good for, what, three months?

Which is why Fitch and Moody’s downgraded Spanish banks and debt.

Which is why Spanish borrowing costs have soared.

And Spain’s deal? Ireland wants some of that. And given the way Irish taxpayers were made to eat Anglo Irish Bank’s debts, I can’t say that I blame them.

And did I mention that Italy’s debt market might collapse?

Which explains why Italy is making noises about actual budget cuts and selling off state owned assets. Naturally, Italian unions are threaten to strike.

“By any objective criteria the Euro has failed, and in fact there is a looming, impending disaster.”

Tsipras has all but flipped Merkel off.

And Merkel fliped him off back.

Europe prepares for an influx of Greek refugees. And by “prepares,” I mean “prepares to keep them out.”

France and Spain want to dig faster.

Obama is boned because Europe is boned.

How the Euro will end: “Greece will simply run out of cash. Then Spain’s real-estate bubble will ruin an economy that really matters.”

Still not completely depressed about Europe’s prospects for escaping the trap created by their bankrupt cradle-to-grave welfare states? Well then, here’s some Mark Steyn to cruelly stomp on those last flickering embers of hope.

Have a happy weekend!

Tags:Alexis Tsipras, Angela Merkel, Budget, Euro, Europe, European Debt Crisis, Germany, Greece, Ireland, Mark Steyn, PIIGS, Spain, Syriza, Welfare State

Posted in Budget, Economics, Foreign Policy, Welfare State | 2 Comments »

Friday, June 1st, 2012

How about a nice slice of EuroDoom to ease you into the weekend?

With all the post-primary news, the European Debt Crises news has been chugging along for a while now. let’s look at some, shall we?

Heh. “The Euro cannot be destroyed by any craft that we here possess. It was made in the fires of Frankfurt. Only there can it be unmade. It must be taken deep into the heart of the European Central Bank, and cast back into the fiery chasm from whence it came!”

If the Leftists win the next round of voting in Greece, they promise to cancel the EU-sponsored bail-out and re-nationalize banks and companies. Way to calm the markets, dude! Not to mention reenacting Clevon Little’s famous scene from Blazing Saddles. “Experience is a dear teacher, but fools will learn from no other.”

“It is no longer a question of if, but how, Greece will leave the euro.”

The money flight from Greek banks continues.

And there’s this: “I can see only one mechanism that could force a collapse of the eurozone: a generalised bank run in several countries.”

In the showdown between Greece and the IMF, both sides deserve to lose.

NEIN! “Almost 80% of Germans reject eurobonds and 60% are against Greece remaining in the euro.”

Germany and Greece play chicken over the euro. That’s like a Mercedes playing chicken with a [ERROR: NO GREEK AUTOMAKER FOUND. ANALOGY ABORTED.]

Ireland votes yes on the Fiscal treaty, and then turns around with an implied “Now fork it over, Otto.”

Why Germany is great and Spain is totally screwed.

It’s a winner-take-all world. Countries that do well have to do a few things extremely well. Germany makes the world’s best machine tools, some of the best heavy engineering equipment, not to mention autos. German manufacturing dominates innumerable key niches. The Spanish don’t do anything well. They haven’t done anything well since the Spanish Empire outsourced its manufacturing to Flanders in the 16th century.

And Spain is really screwed.

Which is why the Germans seem inclined to let them have more rope.

Though at least one source says reports of Spanish bank runs are exaggerated.

But even Germans are getting nervous. Also this:

As a journalist told me yesterday, he worries whether the money in his pocket will be worth anything a year from now. Others worry about Germany’s increasingly negative image among recession-hit southern and eastern Europeans. Americans will understand this feeling well: you pay and pay to help others, only to have them turn on you in hatred and wrath, accusing you of horrible hidden motives and denouncing your selfishness.

Eurobills instead of Eurobonds?

Tags:Euro, Europe, European Debt Crisis, Germany, Greece, Ireland, Spain, Welfare State

Posted in Budget, Economics, Elections, Foreign Policy, Waste and Fraud, Welfare State | 1 Comment »

Thursday, May 24th, 2012

Are the Greeks already printing Drachmas? So says a completely unverified tweet from a random Twitter user. Really, what better source could you possibly ask for?

The Internet is alive with buzz on Greece exiting the Euro (see #grexit for a sip from the firehose). Sadly, there seems to be no buzz at all on reigning in the cradle-to-grave European welfare state that caused the crises in the first place.

More Grext/European debt crises news:

The Fraud of Austerity.

The European debt crises as the world’s longest root canal with the world’s dullest dental drill.

How lovely: diseases unknown to Europe are making a comeback thanks to the Greek government’s colossal mismanagement.

Problem: Greece’s government will seize their citizens’ Euros to forcibly convert them into Drachmas. Solution: Withdraw your cash in Euros. Problem: Burgler’s have figured this out too.

Spain’s Prime Minster: Screw the long term Euro plans, I need the European Central Bank’s sweet low rates right now.

Maybe because his government just pumped €9 billion into failing banks.

Who’s most exposed to the grexit? Italian and Spanish insurers.

There’s no conflict between real austerity and pro-growth polices. Too bad no one in Europe is willing to try them.

Wait, The Guardian actually printed an editorial by John Bolton? (“And the moon became as blood…”) It’s a good one, too:

“Growth” to social democrats means growth in government’s size and reach, not growth in the real economy. This approach directly contributed to our current predicament; and more of the same will only exacerbate it.

Tags:Euro, Europe, European Central Bank, European Debt Crisis, Greece, grexit, Italy, John Bolton, Spain, Welfare State

Posted in Budget, Economics, Foreign Policy, Waste and Fraud, Welfare State | No Comments »

Monday, May 21st, 2012

Though markets have calmed a bit, the desperate search for a lever that will actually steer Europe away from the looming wall of a EuroCrash continues. Meanwhile, certain repeating motifs are detected:

“Now that times are bad, the single currency has turned into an unbridled doomsday machine. Merkel continues to insist that she’ll do whatever it takes to save Europe’s “destiny”. The continued insistence on fiscal austerity and debt repayment tells a different story. Is Germany really prepared to bankroll a wider monetary union by putting its money where its mouth is, or is the game finally up?”

Boris Johnson also calls the Euro a Doomsday Machine:

Europe now has the lowest growth of any region in the world. We have already wasted years in trying to control this sickness in the euro, and we are saving the cancer and killing the patient. We have blighted countless lives and lost countless jobs by kidding ourselves that the answer to the crisis might be “more Europe”. And all for what? To salvage the prestige of the European Project, and to spare the egos of those who were wrong and muddle-headed enough to campaign for the euro.

Johnson is right about the cancer, but slightly wrong about the cause: The European cradle-to-grave welfare state is the cancer; the Euro just made it slightly more malignant.

But with two separate commentator’s calling the Euro a Doomsday Machine, I feel a new meme coming on:

Not to mention much better chances of being linked by Jonah Goldberg and James Lileks…

Europe is awakening from its Utopian dream.

Greece’s invisible bank run.

Greece is happy to stay in the Euro…as long as other countries are footing the bill. They want more subsidies and an end to even the #fakeausterity. Not only do they want to continue to dig their deficit spending grave, they insist on digging it as fast as possible. How to get Germany to agree to continue footing the bill is the one flaw in their otherwise cunning plan…

Why the Blue State model doesn’t work: Cheap money doesn’t mean welfare states balance their budgets, it just means they spend that much more:

Greece, Spain, Ireland, Portugal and Italy (and California). In each case, the promise of more bailouts and a steady flow of cheap money only produced more reckless behavior, excessive levels of government spending and record levels of debt.

Johan Norberg, a senior fellow at the Cato Institute, summarizes the results: “From 1997 to 2007, government expenditures increased by around 6 percent annually in Spain, Portugal and Greece, while population remained mostly stable. Spending increased by 4 percent a year in Italy — even while the economy shrank.”

Consequently, “Between 2000 and 2010, Portugal increased its public debt as a share of GDP from 49 percent to 93 percent, France from 57 percent to 82 percent, Italy from 109 percent to 118 percent, and Greece from 103 percent to 145 percent,” reports Norberg.

Greece and California are headed down the same path to disaster, and for the same reason.

In addition to budget deficits, the EU suffers from a deficit of democracy:

The European crisis is as much a crisis of politics as economics. The current paralysis of the Greek political system demonstrates the point very clearly. EU policy has actively contributed to this crisis by effectively sealing off discussion of the political problems thrown up by austerity.

Budgetary policy is at the core of traditional democratic politics in Europe but the management of the euro zone is increasingly being effected not through democratic institutions but via a centralised and depoliticised form of technocratic fiat. The “stability” narrative has triumphed over the need for legitimacy as the crisis in Europe has deepened.

Ivan Krastev, the eminent political scientist, argues that we have now arrived at a point where national governments have politics but are no longer in control of policy, including budgetary policy, which is moving via the fiscal treaty and other measures to the EU level.

On the other side of this divide the European Union has policies but no politics, since decisions are increasingly being made by technocratic managers rather than directly elected representatives of the European public. The euro zone crisis has thus amplified an existing problem – the absence of both a European citizenry and a transparent European level political process.

A long meditation on what a Greek exit would mean involving Frankenstein, Old Maid, and David Brin.

The EU sends inspectors to find out why Spain’s deficits are so high. Offhand I would say the solution to the mystery might be “because they’re spending more money than they’re taking in.” Obviously such thinking will never get you anywhere in the EU civil service…

Tags:California, Doomsday Machine, Euro, Europe, European Debt Crisis, Greece, pics, PIIGS, Spain, Star Trek

Posted in Budget, Economics, Foreign Policy, Waste and Fraud, Welfare State | 1 Comment »

Saturday, May 19th, 2012

Good evening. I’m not Chevy Chase, and you’re not either. (Unless the real Chevy Chase is reading this, in which case: 1. Loved you on the original SNL, and 2. Stop being such a total dick.)

The EuroZone crises has now reached the stage where European media is doing live updates.

Take a look at this update: “German Chancellor Angela Merkel has mooted the idea that Greece should hold a referendum on the euro alongside its second round of elections next month.” Well, no use even pretending that the Greeks have a say in their own future, is there?

The Zuckermutterobergroupenführer has spoken!

In other EuroDoom news:

Paul Krugman is hardly a fat lady, but when even he says the Euro may end “in months, not years,” then maybe maybe the Euro’s opera bouffe is finally nearing the curtain. And just think: This Nobel Prize-winning economist is only two years behind Mark Steyn (not to mention myself).

The G8 leaders are trying to be more generous with Germany’s money.

The Wall Street Journal staff cover endgame scenarios.

Bank runs continue in Greece…

…and in Spain.

While the European Central Bank has cut off loans to four (unnamed) Greek banks because they’re insolvent. The only wonder is that any Greek banks are considered solvent.

No wonder Moodys is downgrading Spanish banks.

How bad will the Euro-collapse be? “This type of shock could produce instability at least as extensive as the aftermath of the collapse of Lehman Brothers.”

Why the Euro is doomed to fall apart. Besides all the obvious reasons.

Der Spiegel goes all Amityville Horror on Greece: GET OUT.

Speaking of prominent German media outlets slamming Greece (insert your own Cartman’s Mother joke here), can anyone tell me why the Greek finance ministry offices look like an episode of Hoarders? My German is a bit rusty to watch a 45 minute documentary, but what are in the garbage bags? Tax returns?

Spain is going to miss its deficit targets Also, unemployment is going to top 25%.

The difference between America and Spain.

Spain’s housing bubble gets compared to Ireland’s housing bubble, including how it’s getting ready to drag down the banking sector. Actually, it also sounds an awful lot like Japan’s housing bubble. But Spain’s economy isn’t nearly as strong as Japan’s…

One of the many ways France screws growing businesses.

No matter what Greece does, “the country faces years of austerity after years of mismanagement, whatever the election result. Even at the height of the global financial crisis, it was obvious the museum-piece economies of Europe, weighed down by bulging public payrolls, entrenched welfare state systems and archaic work practices, faced greater upheavals and decades of poorer living standards than the US.”

Record shorting against the Euro.

Obama wants Europe to keep digging. After all, the longer they can keep up the charade, the brighter his already-dimming re-election chances…

And given how much America is spending under Obama, we’re in no position to cast stones.

Tags:Angela Merkel, Budget, Economics, Euro, Europe, European Central Bank, European Debt Crisis, Eurozone, Greece, Ireland, Japan, Paul Krugman, PIIGS, Spain, Welfare State

Posted in Budget, Economics, Waste and Fraud, Welfare State | No Comments »

Wednesday, May 9th, 2012

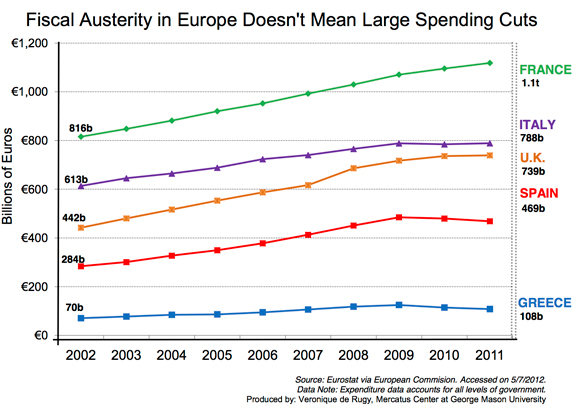

Over on Big Journalism, Joel Pollack makes a point I’ve been emphasizing in my EuroDoom roundups: Austerity hasn’t failed in Europe, it hasn’t even been tried:

The media insists on describing recent election results in Europe as a blow to “austerity,” when in fact Europe’s recent policies are anything but. Government spending has continued to rise across much of Europe, and even those countries that have made small cuts have not reduced government spending to pre-recession levels.

He in turn references this Veronique de Rugy piece at NRO (though the link is broken, so I had to go Googling) which also gives us this handy chart:

None of these “austerity” measures eliminated deficit spending, and none addressed the issue that’s driving all of Europe (and us) bankrupt, namely unwillingness to carry out structural reforms of the welfare state. The few tiny reforms that have been undertaken have been, as NRO’s Michael Tanner notes, ridiculously timid, and even those have been heavily weighted in future years. “So far, European governments haven’t even been willing to take a penknife to the welfare state, let alone an axe.” Plus a huge round of tax hikes:

It should come as no surprise that all those new taxes, combined with a lack of spending restraint, has threatened to throw Europe back into a double-dip recession. Is it any wonder that French, Greek, and British voters were anxious to “throw the bums out”?

Wait, this sounds familiar. Tax hikes on the rich accompanied by vague promises of future spending restraint, while refusing to restructure entitlement programs. That sounds a lot like . . . Barack Obama.

Actual austerity would mean (at a minimum) reducing spending to the amount of money actually taken in. As best I can tell, none of the PIIGS, or France, or the UK has undertaken such real austerity. That “severe” Greek austerity that just caused a change in government? It reduced Greece’s official deficit spending from 9.0% of GDP to 7.5% of GDP. They didn’t even want Greece to stop digging a hole, they just wanted them to dig more slowly.

I suspect that some 20-30 years hence, this mania for deficit spending will be seen as absolute madness, with future generations unable to fathom how politicians were so resolute in destroying their countries economies in order to maintain the welfare state, a folly for the ages. Hyperinflation is probably already baked into the Greek pie for its inevitable exit from the Eurozone, the only question is whether it will be Argentina 1999-2002 style hyperinflation, or Weimer Germany 1919-1923 style hyprinflation, and how much of Europe (and the rest of the world) will follow in their tracks.

Tags:austerity, Budget, Economics, Europe, European Debt Crisis, Eurozone, hyperinflation, Veronique de Rugy, Welfare State

Posted in Budget, Economics, Welfare State | 2 Comments »

Sunday, May 6th, 2012

Chances are good that Europe’s interesting Eurozone times are about to get more interesting still with elections scheduled across the continent today, including those in France and Greece. So what does all this mean? Well, for one thing, the French socialist candidate (who has a good chance to kick Nicolas Sarkozy out of office) wants to renegotiate the fiscal discipline treaty. Perhaps even a socialist can tell a rotting fish when he smells one. And in Greece, the anti-bailout parties are expected to make dramatic gains at the expense of the “center-right” New Democracy (Tweedledee) and “center-left” Pasok (Tweedledum) parties who managed to bring Greece to this lovely pass in the first place.

Opposing Tweedledee and Tweedledum are a motley collection of small parties, including the Neo-Nazi Golden Dawn. Now in Europe, everyone to the right of the Christian Democrats seems to be labeled a “neo-Nazi,” be they libertarians, Geert Wilders, or the British National Party, but Golden Dawn appears to be the real thing. Take a look at their flag:

The overall color scheme seems vaguely familiar. Where have I seen that before? Let me think…

Of course, Golden Dawn is unlikely to gain enough votes to be a real player in the Greek parliament, so we may be denied the irony of seeing neo-Nazis oppose Greece’s German overlords.

There are also elections in Serbia and Armenia, lower level elections in Italy, and in Germany, regional elections in Schleswig-Holstein. While “regional elections in Schleswig-Holstein” must be almost as exciting a topic to American readers as enhanced rescission authority, it might go a long way toward determining whether Angela Merkel will continue in her role as Europe’s Sugar Momma Dominatrix.

Could the ruling parties lose everywhere? Well, since the ruing parties have collectively lost every single election since 2009, yeah. Now, whether the Eurocratic elite are will to let a little thing like “democracy” derail their dreams for an integrated Europe remains to be seen.

Other Eurozone news from the last month or so:

Eurozone jobless rate hits record high.

Capital flight from the PIIGS continues apace.

The central bank of Germany will no longer accept bank bonds backed by Ireland, Greece and Portugal as collateral.

European manufacturing continues to decline.

Spain is still going broke:

With government debt expected to hit 80% of GDP by the end of 2012, Spain has become like a family with a big mortgage where the primary breadwinner has lost his job. Unless they find a way to increase their income, they are going to go bankrupt. It is only a matter of time.

If people want to know what life looks like in the “Prohibitive Range” of the Laffer Curve, all they have to do is to visit Athens. Greece is literally falling apart. Unfortunately, by raising taxes, Spain is making exactly the same mistake that the Greeks made.

And that’s despite putting a ban on cash transactions over € 2,500 in a vain attempt to cut down on tax evasion. They’re also considering hiking their VAT tax, which I’m sure will do wonders for their recession-stricken economy.

Of course, whatever the outcome of today’s elections are, we can be pretty sure they won’t do the one thing that might help get them out of the crises: rolling back the European welfare state.

The a persistent drumbeat among American liberals that in Europe austerity has failed. This is a myth. In fact, it’s never been tried.

Tags:Angela Merkel, Budget, Elections, Euro, Europe, European Debt Crisis, France, Germany, Greece, Spain, UK, Welfare State

Posted in Budget, Elections, Foreign Policy, Welfare State | No Comments »

Tuesday, March 27th, 2012

News! in tiny, bite-sized portions!

Kay Bailey Hutchison tries to walk back her comments, unsuccessfully. She says she opposes abortion, but supports taxpayer funding of Planned Parenthood. That’s like saying you support the Second Amendment, but also support the Coalition to Stop Gun Violence. You can believe one or the other, but not both at the same time.

Hey, how about sending some of that military surplus to the Mexican border?

Even The New York Times has noticed the absurdity of the Obama Administration’s position on ObamaCare: “The Justice Department is essentially arguing that the penalty is not a tax, except when the government says it is one.”

“Europe will never forgive the Jews for Auschwitz.” The new Europe will be Judenfrei.

Escape from North Korea.

Thanks to Muslim pressure, SUNY Stony Brook will no longer celebrate Good Friday, Rosh Hashanah, Yom Kippur, or Passover.

Speaking of New York, here’s another case of insider looting at a Brooklyn hospital. (Hat tip: Dwight.)

Still no signs of Global Warming.

Tags:abortion, Auschwitz, Europe, genocide, Global Warming, Jews, Jihad, Kay Bailey Hutchison, LinkSwarm, Media Watch, Muslim, New York City, North Korea, ObamaCare, Supreme Court

Posted in Border Control, Global Warming, Jihad, ObamaCare, Supreme Court, Texas | No Comments »

Wednesday, February 29th, 2012

Monty, the guy who does the Daily Doom over at Ace of Spades, is taking a break, which means that I have to do my own damn research step into the breach, so here a roundup of European Debt Crises news:

After much hemming and hawing, Germany finally ponies up 130 billion Euros for the latest Greek bailout funds. “Nobody can give a 100 percent guarantee of success” says Merkel. Actually, just remove the “10” and you have the true chance of the latest bailout succeeding in solving Greece’s problems…

And the Greeks, in turn, pass “tough spending cuts”. Presumably those “tough cuts” would be the ones reducing the annual budget deficit from 9% to 7.5% of GDP. They’re don’t even require Greece to stop digging, they just want them to dig slower. And even that assumes that such cuts will actually be implemented.

But despite all that frantic activity, Standard and Poor’s still downgraded Greece’s bond ratings to “Selective Default.” You get the feeling they’ve seen this particular tragedy before, and know exactly how it ends.

Among the austerity measures were a reduction in the minimum wage, including a 22% cut on the standard minimum monthly wage of 751 euros, and a 32% for those under 25. A good idea and necessary, but once again the sons are paying for the sins of the fathers.

Unions, realizing their role in helping bankrupt Greece, have meekly accepted the cuts. Ha, just kidding. They’re going on strike.

Following the downgrade, the European Central Bank announced that they would stop taking Greek debt as collateral, at least until the new Greek bailout package goes into effect.

How bad is Greek bureaucracy? The FDA is a model of efficiency by comparison. At least the FDA didn’t require stool samples from investors.

Germany is thinking of sending German tax collectors to Athens. I’m sure it’s impossible that Greeks would take this in the wrong way.

Speaking of Germany, their high court has ruled yet again that a parliamentary panel set up to approve action by the euro zone bailout fund is unconstitutional.

Portugal is also digging more slowly, having cut its budget deficit from 5.9% of GDP last year to 4.5% this year. Meanwhile, it’s economy also contracted by 3.3%.

The Finns are in, supporting the Greek bailout to the tune of 2.3 billion Euros.

Ireland is actually allowing its citizens to vote on the European stability treaty. Of course, if they vote no, expect them to have to keep voting until they ratify the result the Eurocrats have already chosen for them.

Seeking Alpha makes the obvious point that you don’t want to hold any of the PIIGS sovereign debt. I would go further and suggest that you don’t want to hold any sovereign debt denominated in Euros…

So who, above all, wants to avoid a Euro default among the PIIGS? Would you believe Goldman Sachs? “At the end of 2011, Goldman Sachs had sold $142.4 billion of single-name swaps, contracts that pay out in the event of a default, on the five countries.” That’s an awful of of incentive to keep the game running until all the rubes taxpayers can be fleeced…

Even big-spending, welfare state cheerleader and all-around leftwing mouthpiece Paul Krugman thinks Greece will have to leave the Euro. So it only took two years for Krugman to come part of the way toward realizing what what Mark Steyn did two years ago. Of course, Krugman’s analysis is short term and technical, whereas Steyn saw the unsustainable nature of the welfare state a long time ago. Do you think Kurgman might want become a bit less of a cheerleader for big government? I wouldn’t hold your breath…

EU council president Herman Van Rompuy: All your national parliaments are belong to us.

Spain balks at letting their government reduce spending by 4%of GDP. Problem: Their annual budget deficit is 8% of GDP. That’s the problem when you get that far down the hole to serfdom: Even slowing the digging becomes unacceptable, much less stopping…

“Decades of cradle-to-grave socialism, a short work week and long vacation periods for European Union workers have taken a toll on the treasuries of the nation states. The good life lived in Europe without a thought of tomorrow has brought on these days of reckoning. Greece is an example of the limits of a European welfare state.”

What would a real solution to Greece’s problems look like? “They must roll back bureaucracy, free up entrepreneurs and reduce the burden of the welfare state, so that the private sector can begin to grow….Regrettably, this is not the approach that has prevailed so far. Indeed, as things stand a whole host of European Union and European Central Bank policies are pushing things in precisely the opposite direction.”

American liberals love to talk about Northern Europe’s welfare states, but don’t like mentioning Southern Europe. “For all their fascination with Europe, southern Europe doesn’t loom large for the American Left. But France, Italy, Spain, Belgium, Portugal and Greece are more representative of European outcomes than Sweden, Denmark, and Finland, and have equally sized welfare states. Their failure should not be ignored in the American debate.”

Tags:Euro, Europe, European Central Bank, European Debt Crisis, Goldman Sachs, Greece, Paul Krugman, PIIGS, Portugal, socialism, Spain, Welfare State

Posted in Budget, Democrats, Economics, Foreign Policy, Welfare State | 3 Comments »