It’s hard to know just what the state of the Chinese economy is, given the CCP’s constant lies, but this Joe Blogs video suggests that Chinese manufacturers are in a world of hurt, with four straight years of deflation and falling profit margins.

“Chinese businesses are continuing to suffer from margin erosion. And this is an absolute disaster from China’s perspective, because Chinese businesses have very thin margins in the first place. And if these margins are now being cut, then many businesses in China have now actually fallen into a loss-making situation.”

“More than 50% of the companies in China are now estimated to be banking losses.”

“If you’re posting losses, you don’t pay any taxes, and that will drag down GDP growth in China. The Chinese authorities have said that they’re going to hit 5% again in 2026, but I think there is a major question mark over whether or not that is realistically achievable.” My working assumption is they just lied about hitting that target last year as well. And probably meany years before that.

“If we have a look at this table, it shows what’s been happening with producer prices over the past 12 months. And the scale on the right hand side here starts at zero and goes down to minus 4%. And as you can see, in every single one of the past 12 months, Chinese producers have been cutting their prices. This chart is also referred to as the factory gate prices. So this is the price of products when they’re leaving Chinese factories. And the latest data for January 2026 shows that year on year prices were down by 1.4%.”

“If you put that into the context of your economy, if prices were going down by 1.4%, then you’d be very happy as a consumer, because that means that you’re paying less at the tills.”

“But as a company, this is an absolute disaster. Because the reason why we want some form of inflation in the economy is because it allows companies to pass on their cost increases.”

“But if your end price is going down by 1.4%, then clearly you can’t pass on those cost increases. You have to absorb them. And this is why Chinese businesses are seeing their profit margins being wiped out.”

“And if we widen the scale of this chart to show the last five years, you can start to see the scale of the problem in China, because producer prices, factory gate prices have now been falling since May 2022.”

“What we’ve got here is a compounding of year-on-year falls in factory gate prices.”

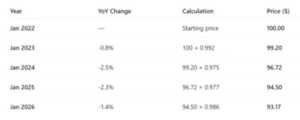

“We have a look at this table I’ve put together. It shows what the impact of this has been on the sales price for a product. So if we assume that January 2022, which was the last time that we saw a price increase year-on-year in China, if we assume that a product that Chinese company was selling for $100 at that time, this shows what the impact has been on that product. So in the year to January 2023, prices fell by 8% producer prices. So that means that that $100 product would have then been selling for $99.20. In January 2024, the year-on-year fall was 2.5%. So that $100 product would then be have sold would have been been selling for $96.72. In 2025 there was a 2.3% fall in producer prices. So that product by then would have been down to $94.50. And the 1.4% that we’ve just seen posted means that that $100 product that was being sold in 2022 would now be selling for $93.17.”

Is this deflation mirrored in Chinese consumer inflation prices? No. “It has been a bit of a mixed story. The scale on the right hand side here goes from 1% positive at the top to 1% negative at the bottom. And as you can see, in six out of the past 12 months, prices did actually fall, but they’ve been increasing over the past four months. And you can see that the latest data that we have for January 2026 shows that year on year prices are up by .2%. So that doesn’t explain the 1.4% fall in producer prices in January 2026.”

“And we widen the scale of this chart to show the past five years. You can see that whilst there has been a few months where we’ve seen deflation, it’s predominantly been inflation in China. It’s a relatively low level compared to other countries, we’re talking between 1% and 2%. So a lot less than we’ve seen in the West over the past five years. But we’ve still seen prices going up.”

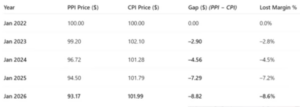

“And if we have a look at this table, it shows what’s happened to prices over the same period. So if we assume the same $100 product in January 2022 that we just looked at for producer prices, in 2023 prices actually went up by 2.1%. So that product would have been selling for $102.10 at that time. We saw deflation in January 2024, which would have brought the price back down to $101.28. In 2025, we saw a year-on-year increase of .5%. So it would have pushed that that price to $101.79. And the most recent data for January 26 of 2% increase tells us that that product would now be selling for $101.99. So an increase in the price.”

“And if we have a look at the comparison between those two tables, then you can see here the producer prices between January 22 and 26, the $100 product has gone from $100 to $93.17. That’s what the companies are receiving for that same product. At the same time, inflation has gone up by 1.99% over that period. That pushed up the price to 101.99. So the gap between those two metrics, what’s been happening with inflation? If producer prices had just been moving at the same rate as inflation, the difference between the two is $8.82 over the past five years. That represents lost profit margin for Chinese businesses over the past five years of 8.6%. So that’s how much profit has been taken out by the fall in producer prices compared to what should have been happening if they were matching inflation.”

“Now why is this happening?”

“Why are Chinese businesses constantly cutting their prices when prices in the domestic market are going up? Well, there’s a number of reasons for it, but one of the main reasons is down to overcapacity.”

“Chinese industry has been gearing up heavily over the past 20 years. So in areas where China believes that it’s strong, it’s put a lot of investment and the government has subsidized a lot of these companies in many situations to enable them to grow rapidly to take a dominant global market position. So we have got some huge businesses in sectors where China has tried to become dominant.”

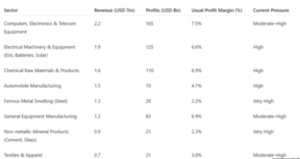

“If we have a look at this table, it shows the different industries in China that are the biggest in terms of revenue and what that should mean in terms of profitability for those businesses.”

“So the biggest sector in terms of manufacturing is computers, electronics, and telecom equipment. So I’m sure you’ve seen lots of different equipment that’s been made in China over the past 20 years. It’s estimated that that sector has revenue of around about $2.2 trillion US, and that should be equating to around about $165 billion of profits. The usual profit margin is around 7.5% for Chinese businesses in those sectors. But those sectors are currently under a lot of pressure.”

“Firstly, we’ve seen its biggest single market, the USA, applying tariffs against Chinese imports. So, that’s causing problems because it’s pushing up the price. And in order to counteract those tariff increases, some Chinese businesses have actually been cutting their cost to absorb some of those tariffs. But also, we’re seeing competition from the rest of the world.”

“So Chinese businesses are constantly slashing their prices to be the cheapest on the shelf because, realistically, that’s why a lot of consumers choose the Chinese option.”

“So that sector is under pressure at the moment. So that’s one of the reasons why those companies are cutting back on their prices.”

“Now another area which is absolutely huge for Chinese businesses is electric vehicles, batteries and solar. So this is an area that China has really specialized in. It’s cornered the market in batteries and solar panels. Most of them are made in China these days. But also electric vehicles. It decided to take a big slice of the global market and those electric vehicles are being sold at very low prices compared to local competition. So if you compare a Chinese electric vehicle the actual list price of that versus things like BMW, Volkswagen, Ford, they are a lot cheaper.”

“That’s one of the reasons why a lot of countries have been applying tariffs on the electric vehicles. So this is aside from Donald Trump’s tariffs. We’re talking about the whole industry globally is saying that it’s not fair that EVs are being subsidized. In terms of revenue, it’s around about $1.9 trillion for China and the usual profit margins around about 7% on that. But they’re under a lot of pressure because of the tariffs. Now a lot of countries are saying that China is trying to put the rest of the world out of business so that it can become completely monopolistic in these areas. So they’re under high pressure, and that’s another reason why Chinese companies are cutting their prices.”

“Jump down to some of the things that are related to property. Look at ferrous metals, which are basically steel. China has some of the biggest steel smelting plants in the world. It’s a big producer of steel. The revenue is about $1.3 trillion. Now the profit margin on steel is wafer thin. 2.2%. And the problem that China has is twofold at the moment.”

“Firstly, a lot of that steel was being sold into the Chinese market for the property market, because the property market over the past 25 years was booming the first 20 years of the 20th century. It was absolutely on fire. Lots of massive property developers like Evergrande were building whole cities all across China and they were using a huge amount of steel to do that. They building these huge tower blocks and you have to put a lot of steel in there.”

“The properties sector has absolutely crashed in China over the past few years, since the government changed the rules and made it more difficult for property developers to borrow money. There hasn’t been anywhere near as much production. So that’s caused a huge drop off in demand in China for steel itself.”

“So that’s meant that Chinese steel businesses have had to look to the export markets. But similar to what’s been happening in the electric vehicle market, a lot of countries, including the USA, have pushed back on Chinese steel imports because they are so cheap that they are killing local steel production. And in the UK, the British government had to recently take over the last virgin steel producer in the UK to make sure that it could actually produce steel that was needed for things like the defense sector. So we’ve seen a major attack globally on the whole steel industry, and lots of countries have pushed back on that.”

“So the steel industry in China is now under a lot of pressure. It’s struggling with regards to demand and those profit margins have been wiped out.”

“But we’ve got a lot of different sectors here that are under intense pressure at the moment from competition. And that’s one of the factors why Chinese businesses are cutting their prices.”

“In addition to that, Chinese businesses are also seeing weak demand at home. Chinese consumers are not buying as much stuff as they used to. So Chinese companies are cutting their prices to try to encourage consumers to keep buying.”

“And as that demand falls at home, what that means is that Chinese businesses are having to depend on the export markets more. So, Chinese companies are struggling with regards to its biggest single market, because the USA has hit all Chinese imports with additional tariffs. So, that’s led to a further cutting of prices and Chinese businesses basically across the board are geared up for high volume, low margin. And when demand starts to fall, then the only thing that you can do is cut your price.”

“Because if you’ve got a huge fixed cost business, if you’ve spent billions building up your business, maybe it’s lots of machinery, you’ve got lots of people, you’ve got huge factories, you need to hit those volume numbers just to keep the wafer thin profit margins going.”

“If demand starts falling, you can’t cut back on your costs because these are very high fixed cost businesses. So what Chinese businesses are doing instead is slashing their prices to maintain their volume of sales. But that is wiping out their profit margins. And that’s why many Chinese businesses, over 50%, are now banking losses.”

“And of course, this is an absolute disaster from the Chinese economy point of view, because it needs those companies to keep contributing to make profits to pay taxes to contribute to GDP in order to hit that 5% GDP total.”

“What we’re seeing from the data that’s just been published is that producer prices are continuing to fall.”

“Inflation is still very, very low in China. Consumer demand is very weak. So China remains dependent on the export markets. Many export markets are pushing back against Chinese imports.”

“Chinese businesses are having to cut their prices, which is further reducing their profit margins. Many have moved into losses, and this is a complete nightmare, vicious circle from many of these companies’ perspective. And I can’t see how they’re going to get out of this situation.”

China’s economy has long been smoke and mirrors all the way down. To be sure, China has made real gains, joining (and gaming) the world economic system just in time to see explosive growth thanks to global trade deals, the container ship era, rampant IP theft, and western capitalists eager to exploit cheap labor. But the rest of the world slowly caught on to China’s tricks, especially since China thought they could get away with belligerent, militarist, expansionist rule-breaking aggression against at the same time it was striving to become the world’s manufacturing hub.

Now that the world’s caught on, people are starting to realize that much of China’s “economic miracle” was an illusion. The opaque banking rules, the government subsidies, the insane “ghost cities” property boom and the regime’s strict currency controls all helped to hide the manipulations, making China’s economy look healthier than it actually is. But now the entire house of cards is tumbling down, and China has no one to blame but itself.

An important but less dramatic aspect of the Russo-Ukrainian War is just what effects the war and resulting sanctions are having on the Russian economy. It’s hard for outsiders to get a handle on just how badly the Russian economy is doing. Since Russia was a net grain and oil exporter before invading Ukraine, it’s not likely to have obvious shortages in food and fuel.

One economic proxy is exchange rates on the Russian ruble, which is now stuck right around 100 to the dollar. But as Joe Blogs explains, Russia has recently undertaken several actions that indicate the situation is worse than just the exchange rates would have you believe.

“The Russian authorities have now imposed additional currency controls, which restrict Western companies that sell their Russian assets from taking the proceeds in dollars and Euros. International companies that want to exit Russia now have to sell their assets in rubles, and if they insist on receiving foreign currency for their assets, they face delays or even losses on the sums that can be transferred abroad.” Obviously I have zero sympathy for any western company still doing business in Russia, as they should have extracted themselves shortly after Russia launched their illegal war of territorial aggression in 2022, but it’s hardly going to encourage the ones that remain to put more resources into their businesses there.

Russia first started slapping currency controls down when the ruble weakened in July, with various repatriation restrictions and limiting schemes. Also, businesses wanting to get their money out were forced to pay “a contribution to the Russian budget, which is deemed to be ‘voluntary’ but in reality is mandatory, which was recently raised from 10% to 15% of the total transaction value.” The line item on that should probably read “Vlad’s Protection Money.”

Plus: “The sale of any Russian assets must take place at a discount of at least 50%.” You lie down with jackals and you wake up with fleas.

Various other indignities visited upon foreign businesses doing Russia snipped because, really, screw those guys.

Then there are the foreign income controls:

On October 11 “President Putin signed a decree mandating the reintroduction of capital controls for an undisclosed list of 43 exporting firms. The controls will last for six months, and Russia has not published the list of which companies these measures will apply to. However, they are companies in the fuel, energy, metal, chemical, timber and grain industries. Starting from October the 16th, certain Russian exporters within 60 days from the moment of receiving funds are obliged to credit their accounts in Russian banks with no less than 80% of all foreign currency received in accordance with the conditions of their export contracts. They also required within two weeks to sell on the country’s domestic market no less than 90% of foreign currency revenues credited to their accounts at Russian banks.

“President Putin believes that this will solve the problems with the ruble, and stated there are reasons to believe that the ruble rate is fluctuating because foreign currency earnings are not being returned in sufficient volume to mobilize the money supply on the domestic market.” Or, and here’s an alternate theory, rubles are worthless because no one inside or outside the country wants to keep them.

“Twelve months ago, one US dollar was trading for 61 Russian rubles, to today it’s trading for 93, which represents a fall in value of more than 50% in the last year, which is an absolute disaster from a currency perspective. The long-term value of the ruble has declined significantly.”

“There is absolutely no way that the Kremlin is happy with an exchange rate of 93 to 1.”

“Let’s not forget that the current exchange rate has only been achieved after four interest rate rises over the last three months, which means that it’s doubled in a three month period.” Russia’s interest rate is currently at 15%, which is one of the highest in the world.

Had Russia not intervened, “the ruble [to dollar exchange rate] could have hit 120 or 130. So Russia is currently doing everything within its powers to maintain the value of the ruble. But even after all of that effort the ruble is trading at its worst level at any time in history” save that right after the Ukraine invasion.

With all those rules and declining ruble values, Russian companies have less and less money to spend in international markets, which demand hard currency.

Even though sanctions are leaky, Russia’s crashing economy means the ruble is worth less, and Russian companies will find it harder and harder to buy things (like computer chips) on the international market that requires hard currency. And remember that that BRICS currency idea is going nowhere.

Expect Russia’s economy to continue declining as long as Russia is still trying to occupy Ukraine.