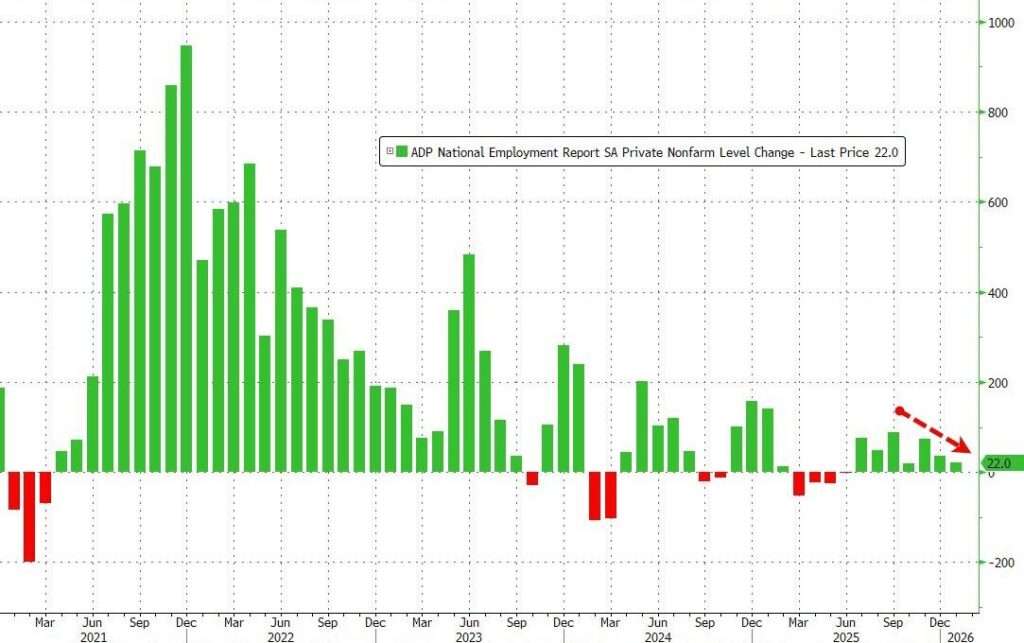

Statistics show that, one year into Donald Trump’s second term, the economic lassitude of the Biden Recession is still weighing down the American economy, as it isn’t creating jobs.

While we will not be getting the payrolls report this week (due to a very brief govt shutdown), ADP’s Employment report paints a poor picture for hiring (even if jobless claims paints a healthy picture for ‘not firing’) adding just 22k jobs (well below the 45k expected).

22 thousand jobs isn’t even a dead cat bounce, it’s a rounding error. And the low jobless claims are just because most of the workers fired/laid off during the Biden Recession have run out of eligibility.

Goods producing firms added just 1k jobs (Construction +9k, Manufacturing -8k – which has lost jobs every month since March 2024) while Services firms saw only 21k jobs added (with health care a standout, adding 74k job, while Professional Services lost 57k jobs).

“Job creation took a step back in 2025, with private employers adding 398,000 jobs, down from 771,000 in 2024,” said Dr. Nela Richardson Chief Economist, ADP.

Interestingly, small firms saw job additions while large firms saw job losses…

We’re not seeing the massive manufacturing job losses critics of President Trump’s tariffs predicted, but we’re also not yet seeing any gains from the lowering of foreign tariffs.

Job seekers are discouraged by a plague of ghost job listings intended to provide the illusion of growth, with no intention of anyone ever being hired.

Inflation is low, yet consumer confidence is at the lowest level in more than a decade. Stocks are booming, yet no one seems to be hiring. (This seems to be my personal experience as well.) Trump and congressional Republicans have managed to lower taxes, yet the “animal spirits” of the American economy do not seem like they’re been unleashed.

Is AI eliminating jobs? Maybe, especially in the service sector (those AI agents everyone hates have probably replaced some humans on support lines). But tech has been a job growth driver for much of this century, and an AI infrastructure build-out seems to be sucking up all available venture capital (and then some) with very little to show for it in the way of actual profits thus far.

Maybe job creation will only resume after California’s billionaires have finished fleeing to avoid the proposed wealth tax.

Would aggressive rate cutting by the Fed help? Probably, but outgoing Fed chair Jerome Powell seems to be pursuing rate cuts with all the vigor of Æthelred the Unready.

The American economy seems becalmed in Hell, and no one seems to know why.

Russian lawmakers have proposed introducing food ration cards across the entire country in response to rising prices, claiming the idea has a “healthy foundation”, the Moscow Times wrote on Dec. 15.

Anatoly Aksakov, head of the State Duma’s Committee on Financial Markets, endorsed the idea of reintroducing food vouchers reminiscent of those used in the Soviet Union – the proposal, initially suggested by the Russia’s Kaliningrad Oblast governor.

Aksakov believes the initiative should be expanded nationwide. The Russian official stated that food vouchers would help “support socially vulnerable groups,” though he did not specify a potential monthly allowance for these cards.

“As of Dec. 9, the Russian Ministry of Economic Development reported annual inflation reaching 9.2%, the highest level since February 2023. However, alternative metrics indicate significantly higher figures,” the publication noted.

Food ration cards in Kaliningrad Oblast are set to roll out in 2025, targeting pensioners with incomes below the subsistence minimum.

On Dec. 10, it was reported that the Kremlin had significantly increased military spending amid a catastrophic collapse of the ruble. The Russian government has allocated unprecedented funds for the war against Ukraine.

For 2025, Russia’s budget includes a 25% increase in military spending, bringing it to 13.49 trillion rubles ($175.37 billion). Military expenditures will account for 32.5% of the budget, an unprecedented level since the Soviet era. By comparison, during the first year of the war against Ukraine, the government spent 17% of its budget on the military. In 2023, this figure rose to 19%, and the 2024 year’s allocation stands at 29.5%.

And how is the rest of the Russian economy doing? The parts supporting the war are doing great, but the rest is overheating due to inflation and crumpling under the load of high interest rates.

Interest rates are expected to hit 23% this month.

Despite the high interest rates, inflation isn’t going down, running at an official rate of 9% (and unofficially much higher).

Food staples are up even more, from 12% for bread to 74% for potatoes. Stores are locking up butter to prevent theft.

Russian business bankruptcies are up 30%.

Russia’s rail system can’t afford preventive maintenance due to higher interest rates.

Russia’s current low unemployment is driven by government spending on its war economy, and its not sustainable.

The military sector is sucking in more and more manpower, leaving fewer and fewer workers for other sectors of the economy hit by higher labor costs, higher interest rates, and higher inflation.

Unequal distribution of the gusher of war economy money is screwing the poor even harder.

Even Putin says Russia needs another million workers.

“There is a shrinking number of people who can keep Putin’s war machine running.”

Speaking of Russia’s illegal war of territorial aggression, just how is that going? Given that Russia now has 63-year old recruits, I’ve got to guess not that well.

Also, two Russian oil tankers sank in the Kerch Strait, reportedly because they were river going vessels, and thus not rated for seaborne stresses. That suggests that Russia’s oil transportation capability is in serious trouble.

Also in serious trouble: Russia’s arms export industry, thanks to how poorly their arms have performed in Ukraine.

Finally, largely (though not entirely) unrelated to the Ukraine quagmire—

—is the collapse of Assad’s Syria, an important client state for Russia:

Russia is in a pickle getting its men and equipment home, because it can’t overfly nations hostile to it (most of them), it can’t sail ships home through the Bosporus (Montreux Convention), and it probably can’t get them all the way home up to its Baltic ports because it can’t refuel and resupply at hostile NATO ports (I wonder if a combination of Mediterranean African ports and at-sea resupply could get the job done). Plus Russia has been resupplying its mercenary army supporting Africa’s League of Assholes (Niger, Mali and Burkina Faso) from Syria, and Assad’s fall puts the entire operation in jeopardy.

The stresses on Russia are only going to get worse moving forward. For all the talk that Trump is going to bail Russia out, Volodymyr Zelenskyy evidently doesn’t think so. Plus one of Trump’s key negotiating tactics is to threaten whatever the other party holds most dear to force them to agree to a deal. And given Russia’s numerous manifest weaknesses, Trump is going to go into talks with an awful lot of leverage points…

Indeed, this is the first interest rate hike for Japan in 17 years.

According to Keynesian economics, Japan should have experienced an economic boom from all that monetary stimulus. It did not. Prices were stagnant. Wages were stagnant. GDP growth was anemic.

Yet deficit spending remains the preferred policy solution of just about every damn country in the world.

Back in the dim mists of time (i.e., the 1980s), Japan Inc. was going to take over the world. That didn’t happen either. Instead, the Japanese bubble, based in huge measure on wildly unsustainable real estate valuations (“At the peak of the bubble economy, Tokyo real estate could sell for as much as US$139,000 per square foot, which was nearly 350 times as much as equivalent space in Manhattan. By that reckoning, the Imperial Palace in Tokyo was worth as much as the entire US state of California.”) popped. There then followed three decades of economic stagnation.

The Biden recession and other trends made 2023 a horrible year for startups.

“Big startups are shutting down. According to PitchBook, more than 3,000 private venture backed startups failed in the last year.”

“Of the startups raising money, 19% were funded at a lower valuation than in prior funding rounds.”

“38% of VCs disappeared from dealmaking last year and more than a quarter of a million workers at tech companies were laid off over the same period.”

“US corporate bankruptcy filings closed out 2023 with the most filings since 2010. The year has been described as a mass extinction event for startups in the press.”

Some of the startup failures Boyle namechecks (Hyperloop, Bird) seemed like stupid ideas from the git-go. “Bird the electric scooter rental company—which was also supposed to reinvent public transportation—filed for chapter 11 bankruptcy protection. It was the fastest startup to ever land a billion-dollar valuation, and at its peak was worth two and a half billion dollars. It was delisted from the New York Stock Exchange in September after failing to maintain a market cap of above $15 million dollars for 30 consecutive days.”

“Who would have thought that renting scooters to drunk people for a dollar (who would then throw them in a canal on their way home) would be a money losing business? Bird ran up more than $1.6bn in net losses since 2018 before finally running out of money.”

Smile Direct Club: $8.9 billion valuation at 2019 IPO. “The stock fell in value over time as the company proved to be unprofitable year after year. The company shut down last month $900 million dollars in debt.”

One I never heard of: “The health tech startup Olive AI which reached a peak valuation of $4 billion dollars in 2020 driven by the need for automation in healthcare during the pandemic. The company raised over 900 million dollars from investors. In 2022 the company began laying off staff citing ‘tough economic conditions.’ The company was allegedly trying to raise money when it abruptly shut down in November. Going out of business in 2023 was particularly surprising for a company with AI in its name.” Indeed, AI seems to be the current space where stupid money goes to die.

Another one I never heard of: Zume.

No.

“Zume – the robot pizza delivery company which had raised $445 million dollars in VC funding, the majority of which came from SoftBank in 2018 at a two and a quarter billion-dollar valuation, shut down this summer.” Stupid, but at least I can see why California companies would invest heavily in food automation with that $16 (and rising) minimum wage.

WeWork “set out to revolutionize office real estate – by having an app – which I’m told didn’t work very well, and free beer on tap filed for bankruptcy in November.” I’ve covered WeWork previously.

“WeWork and its founder Adam Neumann were the poster boys of how a blitzscaled business model led by a charismatic founder could apply a veneer of technology to an old business idea and attract venture capital funding to achieve a multibillion dollar valuation.”

“At its peak, WeWork was valued in private markets at $47 billion dollars. Softbank alone invested 16 billion dollars into the company. Masayoshi Son, SoftBank’s founder, allegedly invested his first $4.4 billion dollars in the shared office space company after Neumann gave him a 12-minute tour of a WeWork in 2016. With such a short tour, it’s unlikely that the free beer even had an impact.”

“Softbank – run by Masayoshi Son (Japan’s Cathie Wood) was one of the biggest startup investors in the last decade. They invested in all sorts of non tech companies that were made to look like tech in order to attain a sky-high valuation. According to Bloomberg, the SoftBank Vision Fund alone lost $53 billion dollars over the last two years on startup investments.”

“We have seen a very difficult period for startups over the last year or two, but it comes in the wake of probably the best period for VC backed startups in decades. During the decade from 2011 to 2021 VC investment in private start-ups grew more than sevenfold, from 46 billion dollars in 2011 to $345 billion dollars in 2021.”

“In 2022 when the federal reserve began hiking interest rates, this money began drying up as investors lost their taste for unprofitable, but high growth, investments.”

That investment boom was driven by two things: Low interest rates and “a recent history of profitable exits from VC funded startups like Facebook, Google, Whatsapp and Snap meant that investors were suddenly paying a lot of attention to tech startups – hoping to repeat those successes.”

“Venture capital went from being a small asset class run out of offices on Sand Hill Road that had burned investors in the dot com bubble to a massive global asset class like hedge funds or private equity.”

The Flu Manchu lockdowns brought investment from “‘working from home’ companies like Zoom and Peloton.” I always thought of Peloton as a lifestyle luxury brand.

“People were using apps like Uber and DoorDash for food delivery, and booking rentals on Airbnb to get out of big cities now that they no longer had to turn up in the office.”

“While the prior wave of profitable high growth tech stocks had been (one way or another) in the advertising space, or in businesses like cloud computing, the new wave of startups had untested business models—gig economy businesses which attracted a lot of competition and might never flip to profitability—or robot-made pizza which would be cooked on route to a customer’s home.”

“A lot of the VC’s possibly believed in many of the questionable investments that have since gone bust, but a venture capital fund isn’t really there to hold on to these investments until the underlying business flips to profitability. They invest at the idea stage with the goal of selling these businesses on to the public when the hype is at its peak.”

“They did manage to unload a number of the biggest flops like WeWork – but not at the valuations they were hoping for, and have found themselves holding the bag on a lot of investments that they bought into at peak valuation.”

“The huge valuations many of these companies were attaining in the private market may have been more of a function of how much money had flowed into the private tech startup market since 2011 rather than necessarily reflecting the quality of these companies and their business models.”

“According to Erin Griffith at The New York Times, $27.2 billion dollars in VC funding had gone into the 3,200 venture-backed companies that went out of business in the first 11 months of 2023.” And that’s just the firms trackable on PitchBook. The true total is almost certainly higher.

“That 27.2 billion dollar number excluded many of the largest startup failures that went public, like WeWork, or that found buyers at much lower prices than VC investors had invested at.”

“The hype around AI that we have seen in the last year has masked a lot of the losses in the tech space.”

“Meta was up 178 percent last year due to a combination of AI hype and cost cutting within their core business. This covers up the 46.5 billion dollars lost on the Metaverse – which no one will venture into, for fear that they run into Mark Zuckerberg.” I strongly suspect that a lot of those VR losses are actually money siphoned off for something else.

Despite this, stocks like Meta, Microsoft and Nvidia have hit all-time highs.

“One of the negative economic effects of startup shutdowns is that in such an environment it becomes harder for founders with good business ideas to get funding.”

“According to PitchBook, the number of active investors in US Venture Capital, which was defined as firms that made two or more deals in the last year, plummeted by 38% in the first three quarters of 2023 compared to the same period the prior year.”

Many of the startup failures were zombie companies, those that should have failed earlier but were kept alive by VC money and low interest rates.

“No one wants to see firms going out of business, especially startups which are often the most exciting and innovative firms, but if a business model makes no sense, or only works in a zero-interest rate environment, then its disappearance means that capital can again flow in the direction of the best businesses.”

The startup bust has direct negative effects on me personally, as I’m still between technical writing positions, and a lot of the jobs I’ve gotten over the past two decades have been with startups.

An important but less dramatic aspect of the Russo-Ukrainian War is just what effects the war and resulting sanctions are having on the Russian economy. It’s hard for outsiders to get a handle on just how badly the Russian economy is doing. Since Russia was a net grain and oil exporter before invading Ukraine, it’s not likely to have obvious shortages in food and fuel.

One economic proxy is exchange rates on the Russian ruble, which is now stuck right around 100 to the dollar. But as Joe Blogs explains, Russia has recently undertaken several actions that indicate the situation is worse than just the exchange rates would have you believe.

“The Russian authorities have now imposed additional currency controls, which restrict Western companies that sell their Russian assets from taking the proceeds in dollars and Euros. International companies that want to exit Russia now have to sell their assets in rubles, and if they insist on receiving foreign currency for their assets, they face delays or even losses on the sums that can be transferred abroad.” Obviously I have zero sympathy for any western company still doing business in Russia, as they should have extracted themselves shortly after Russia launched their illegal war of territorial aggression in 2022, but it’s hardly going to encourage the ones that remain to put more resources into their businesses there.

Russia first started slapping currency controls down when the ruble weakened in July, with various repatriation restrictions and limiting schemes. Also, businesses wanting to get their money out were forced to pay “a contribution to the Russian budget, which is deemed to be ‘voluntary’ but in reality is mandatory, which was recently raised from 10% to 15% of the total transaction value.” The line item on that should probably read “Vlad’s Protection Money.”

Plus: “The sale of any Russian assets must take place at a discount of at least 50%.” You lie down with jackals and you wake up with fleas.

Various other indignities visited upon foreign businesses doing Russia snipped because, really, screw those guys.

Then there are the foreign income controls:

On October 11 “President Putin signed a decree mandating the reintroduction of capital controls for an undisclosed list of 43 exporting firms. The controls will last for six months, and Russia has not published the list of which companies these measures will apply to. However, they are companies in the fuel, energy, metal, chemical, timber and grain industries. Starting from October the 16th, certain Russian exporters within 60 days from the moment of receiving funds are obliged to credit their accounts in Russian banks with no less than 80% of all foreign currency received in accordance with the conditions of their export contracts. They also required within two weeks to sell on the country’s domestic market no less than 90% of foreign currency revenues credited to their accounts at Russian banks.

“President Putin believes that this will solve the problems with the ruble, and stated there are reasons to believe that the ruble rate is fluctuating because foreign currency earnings are not being returned in sufficient volume to mobilize the money supply on the domestic market.” Or, and here’s an alternate theory, rubles are worthless because no one inside or outside the country wants to keep them.

“Twelve months ago, one US dollar was trading for 61 Russian rubles, to today it’s trading for 93, which represents a fall in value of more than 50% in the last year, which is an absolute disaster from a currency perspective. The long-term value of the ruble has declined significantly.”

“There is absolutely no way that the Kremlin is happy with an exchange rate of 93 to 1.”

“Let’s not forget that the current exchange rate has only been achieved after four interest rate rises over the last three months, which means that it’s doubled in a three month period.” Russia’s interest rate is currently at 15%, which is one of the highest in the world.

Had Russia not intervened, “the ruble [to dollar exchange rate] could have hit 120 or 130. So Russia is currently doing everything within its powers to maintain the value of the ruble. But even after all of that effort the ruble is trading at its worst level at any time in history” save that right after the Ukraine invasion.

With all those rules and declining ruble values, Russian companies have less and less money to spend in international markets, which demand hard currency.

Even though sanctions are leaky, Russia’s crashing economy means the ruble is worth less, and Russian companies will find it harder and harder to buy things (like computer chips) on the international market that requires hard currency. And remember that that BRICS currency idea is going nowhere.

Expect Russia’s economy to continue declining as long as Russia is still trying to occupy Ukraine.

Here’s hedge fudge manager/university professor Patrick Boyle goes into detail of just how it went down.

“Silvergate’s importance in the recent crypto boom is possibly best described by a now-deleted testimonial from the bank’s website: ‘Life as a crypto firm can be divided up into before Silvergate and after Silvergate.It’s hard to overstate how much it revolutionized banking for blockchain companies.’ The testimonial was written by a millennial who still lives in his parents’ basement playing video games and has had some recent run-ins with the law. His name is Sam Bankman Fried.”

“If we go back ten years, Silvergate was a small San Diego based real estate lender that transformed itself into the go-to bank for the crypto industry.”

“Silvergate invited in crypto entrepreneurs and asked them what problems they were trying to solve and how the bank could be helpful. After this, the bank transformed itself and grew rapidly. It went public in late 2019 at a share price of $13, and a year later the stock price had risen by 1,580% as it became a key interchange point between dollars and cryptocurrencies.”

“Major Silverlake clients included Paxos, bitFlyer, Kraken and also innovators in atonal rock music – Mars Junction…” [This is an inside joke. Mars Junction is the band of Cameron & Tyler Winklevoss, AKA the WInklevoss Twins of Facebook investing controversy] “…who also had some involvement in the Crypto industry. FTX and Alameda were also big customers.”

“The bank’s growth mirrored the growth of the crypto industry, and it declined alongside that industry too, announcing in a regulatory disclosure earlier this week that it plans to wind down operations in the face of ‘turmoil in digital currency markets.'”

Last week Silvergate had announced that they would be unable to file an annual report with the SEC on time due to a weakening in their capital position. They announced that they might be forced to close at that time, blaming growing problems, in part on pending investigations into their operations. The filing confirmed that Silvergate is being investigated by the US Department of Justice.”

“Customers rushed over the last few months to pull money out of Silvergate. In January they reported that customers had withdrawn more than $8 billion, forcing them to sell held-to-maturity assets to fund the run, accruing losses on the sale of those securities of $718 million dollars.”

Why was Silvergate so important in the world of crypto? Well, people who trade cryptocurrencies often want to use dollars to buy crypto, or they want to sell crypto and receive dollars and the dollar side of those transactions is where things get bogged down. If you are transferring large sums of money to buy crypto, you need to deal with the US banking system, who might ask you a lot of questions relating to anti money laundering regulations. Crypto people hate questions like this. Similarly, if you just sold some crypto and want to deposit the dollars you received, most banks will have a long list of questions about the source of your funds, and there is a really good chance that they will simply refuse to do the transaction. It is going to be a struggle for a US regulated financial institution to show their regulator that they have done enough due diligence to be sure that your funds are not the proceeds of crime. And the last thing a bank needs is to be accused of money laundering; they would rather just simply not deal with suspicious transactions.

“For this reason, stablecoins like Tether and Terra exist – or existed.” If you weren’t paying attention, the value of theoretically stable Terra crashed hard last year.

“If you can convert your dollars into crypto once, you can then buy stablecoins that are supposed to always be worth a dollar, and then instead of buying and selling crypto, with actual dollars you buy and sell crypto with dollar-denominated stablecoins, your money can stay ‘on chain.’ The problem with that, is that you have to trust the stablecoin issuers, and they, for some reason, don’t always seem trustworthy. They won’t really tell you where the money is.”

“They’ll sometimes announce that they are going to be audited by a top 12 auditor (I’m not really sure what a top 12 auditor is – but when you hear that – you know you are getting number 12 on the list), and you start to wonder if Friehling & Horowitz made that list.” Friehling & Horowitz were Bernie Madoff’s auditors.

“If you have deposited your dollars with a crypto exchange or a stablecoin provider, they still need to deposit them somewhere. They need a bank too. Now (of course), another way of dealing with this banking issue, might be to lie to your bank about what your account is being used for (SBF and the team at FTX did that), but the technical term for ‘lying to your bank’ is Bank Fraud (as Sam Bankman-Fried just found out) – and you can get in trouble for that.”

“There was significant demand for a “crypto friendly bank” and Silvergate was willing to fill that role, when no other bank was willing to take that risk. Silvergate weren’t just crypto friendly either, they built their own payments network called the Silvergate Exchange Network to (according to their marketing documents) enable the efficient movement of U.S. dollars between participants 24 hours a day, 7 days a week, 365 days a year.”

“As you might imagine, Silvergate (being the only bank that would deal with them) attracted a lot of big crypto customers, as these customers were able to open up accounts without lying too much.”

“Silvergate dealt with most of the big players in the industry and they were an actual US regulated bank with excruciatingly detailed audited financial statements and capital regulation. This meant that your money was safe at Silvergate, unlike at the other venues we just went over.”

“The beauty of dealing with these crypto customers, crypto exchanges, [was] that because you don’t have any real competition in this space, you don’t really have to pay them any interest on their deposits. You could take the billions of dollars they deposit with you, put it all in treasuries, and you get to keep all of the interest. You’ll probably have to spend some of the profits on lawyers to keep the regulators at bay, but overall you might have a profitable business. But that’s boring right? And no one gets involved in crypto for a boring life…”

“They had a product called SEN Leverage direct lending, where they would lend people money collateralized with bitcoin. Exchanges could also borrow dollars collateralized with bitcoin for corporate treasury and other business purposes. In January, they announced that total SEN Leverage commitments were $1.1 billion dollars and that all of their SEN Leverage loans ‘continued to perform as expected, with no losses or forced liquidations.’ So, as crazy as that business might sound, it was not really the source of their problems.”

“As of September, 2022 their balance sheet showed about $11.4 billion of ‘securities,’ meaning bonds: Treasury securities, mortgage-backed securities, agency bonds and so on and $1.4 billion of ‘loans,’ meaning the Bitcoin loans and some other real-estate lending. They had $13.2 billion worth of deposits at the end of September, most of them being from crypto companies – so non-interest paying deposits, the best kind.”

“The problem for Silvergate was that when FTX was exposed as being insolvent, crypto investors were considerably less willing to leave their cash on exchanges.”

“They asked for their money back from the exchanges, meaning that the crypto companies had to ask for their money back from Silvergate, so Silvergate was faced with a good old fashioned bank run – driven not by a loss of faith in Silvergate, but by a loss of faith in crypto exchanges. By the end of December, noninterest bearing deposits at Silvergate fell from $13.2 billion dollars to just $3.9 billion dollars.” Yowzers! It’s hard to expect any bank to survive an outflow of 2/3rds of their deposits in such a short period of time.”

“There is a good chance that if you had an account at a crypto exchange, that exchange banked with Silvergate, and if you closed your account and cashed out, the cash came from a deposit at Silvergate.”

“There were other FTX related problems too. When prosecutors started looking into the collapse of FTX, their attention was drawn to their banker – Silvergate, for hosting accounts connected to Sam Bankman-Fried. Now, a big problem for Silvergate, was that – with their money all tied up in bonds or lent out, Silvergate had to come up with around 9 billion dollars to pay out these withdrawals.”

“Their accounts show that by the end of December they had sold half of their bonds and had controversially borrowed $4.3 billion from the Federal Home Loan Bank of San Francisco, a government institution that is in place to give short-term secured loans to banks that have a short-term liquidity problem.” That, and the FTX connection, attracted the attention of Washington D.C.

In September Silvergate had shown 3.1 billion dollars’ worth of bonds as being “held to maturity” and 8.3 billion dollars’ worth of bonds as being available for sale. The difference between these two classifications (from an accounting perspective) is that the available for sale bonds have to be marked to market – or held on the books at their fair market value, while the “held to maturity” bonds could be marked at their cost price. By the end of December there were no “held to maturity” bonds left on the balance sheet, meaning that they had either been sold, or reclassified as available for sale. One way or another, interest rates had gone up a lot in 2022, and these bonds were worth a lot less than they were being carried on the balance sheet at.

So they might have skated by if rising interest rates hadn’t wrecked their mark-to market.

The sale resulted in a loss of $751.4 million during the fourth quarter of 2022 and in addition, the company recorded a $134.5 million dollar impairment charge related to an estimated $1.7 billion dollars of securities it “expects to sell in the first quarter of 2023 to reduce borrowings.” This is because reclassifying some of the bonds to “available for sale” meant that they now had to be marked to market and that the loss had to be recognized under GAAP accounting rules. Silvergate also had to write down a $196 million dollar investment in “certain developed technology assets related to running a block-chain-based payment network” that it had bought in January 2022. So, all in, there was a net loss of over a billion dollars in the fourth quarter of 2022.

“Bank capital requirements are ‘risk-based’ and need to be kept above 4% to be ‘adequately capitalized’ and above 5% to be considered ‘well capitalized.’ Different types of assets have different risk weights, and this is done to keep deposits safe.”

“A bank that makes a lot of mortgage and business loans might have a capital requirement of around 8%, and assets like bitcoin have a 100% capital requirement, meaning that a bank would need to have $100 of capital for every $100 of bitcoin on its books.”

“In September Silvergate was fine, as despite the Bitcoin loans, most of their money was in high quality bonds that had zero risk weights. But when their deposits went out the door and they had to sell assets and realize a billion-dollar net loss, they were left in a situation where an additional $19 million-dollar loss would but their capital below 5% and they would no longer be considered well capitalized.”

“Last week Silvergate announced that they had sold additional debt securities in January and February to repay the company’s outstanding advances from the Federal Home Loan Bank of San Francisco and that they ‘expect to record further losses related to the other-than-temporary impairment on the securities portfolio.’ These additional losses they said would ‘negatively impact the regulatory capital ratios of the company and could result in the bank being less than well-capitalized.” And that’s when Brunhilda strode on stage to give her farewell.

“This announcement caused the stock price to half that day and according to Bloomberg caused Coinbase, Galaxy, Paxos and other crypto firms to announce that they would stop accepting or initiating payments through Silvergate. These customers leaving were the final nail in the coffin, as they reduced deposits even further.”

“A bank run, on a real bank, caused by crypto related losses and crypto volatility.”

“Matt Levine at Bloomberg argues that one way to think about the rise and fall of Silvergate is that the crypto boom was at its heart a low-interest-rate phenomenon. People started speculating in crypto because interest rates were below the rate of inflation, and so Silvergate was hugely exposed to interest-rate risk simply because of its exposure to its crypto customers.”

“Rising interest rates caused the deposits to evaporate at the same time as the assets backing those deposits fell in value. Levine argues that (with hindsight), Silvergate’s risk management – a year ago – should have been laser-focused on the risk of rising interest rates crushing both its assets and its customers, and it should have hedged that risk one way or another.”

I know all this is long and a bit detailed and technical, but I wanted to point it out as an example of how a cascading chain of events (much like the Piper Alpha disaster) caused a failure, mainly how massive fraud on the basis of one crypto space player and rising interest rates ended up bankrupting a real bank in the real world.

I hope all BattleSwarm readers are safe from the Joe Biden Armageddon thus far. Today’s LinkSwarm features Democrats disdaining the rules followed by the little people, the UN is delusional enough to think they can run the world and defy the laws of economics, and petting dogs is good for you.

UNCTAD, the UN agency dealing with global trade, demanding *all* central banks stop rate hikes and instead switch to price controls. They argue, “policymakers appear to be hoping that a short sharp monetary shock – along the lines, if not of the same magnitude, as that pursued… under Paul Volker – will be sufficient to anchor inflationary expectations without triggering recession. Sifting through the economic entrails of a bygone era is unlikely, however, to provide the forward guidance needed for a softer landing given the deep structural and behavioural changes that have taken place in many economies, particularly those related to financialization, market concentration and labour’s bargaining power.”

I am not playing tennis with them either, but note the radicalism. Indeed, their latest report also argues, “supply-chain disruptions and labour shortages require appropriate industrial policies to increase the supply of key items in the medium term; this must be accompanied by sustained global policy coordination and (liquidity) support to help countries fund and manage these changes.” So, industrial policy. And Fed swap-lines. Expect both ahead.

They also ask why we haven’t regulated shadow-banking, and why we allow speculators in global commodity markets who have nothing to do with underlying trade. On the latter they note, “Market surveillance authorities could be mandated to intervene directly in exchange trading on an occasional basis by buying or selling derivatives contracts with a view to averting price collapses or deflating price bubbles.” I expect nothing but that ahead – and geopolitically driven to boot.

This boils down to: “Hey, we need to institute economic policies proven to fail, because otherwise lots of rich people will lose money!” Wage and price controls were tried in the 1970s and they failed miserably. The longer governments try to defy the market, the more terrible the snapback when those efforts fail.

On Tuesday, the New York Times framed a story circulating on the right over a software company’s connection with the Chinese Communist Party as a “right-wing conspiracy theory.”

“At an invitation-only conference in August at a secret location southeast of Phoenix, a group of election deniers unspooled a new conspiracy theory about the 2020 presidential outcome,” was the Times’ original lede (via the Daily Caller).

In it, the Times wrote that “right-wing” election deniers in Arizona had fabricated a conspiracy theory that election software company Konnech had secret ties to the CCP, and was passing them information on around two million US poll workers.

“In the two years since former President Donald J. Trump lost his re-election bid, conspiracy theorists have subjected election officials and private companies that play a major role in elections to a barrage of outlandish voter fraud claims,” reads the article. “But the attacks on Konnech demonstrate how far-right election deniers are also giving more attention to new and more secondary companies and groups. Their claims often find a receptive online audience, which then uses the assertions to raise doubts about the integrity of American elections.”

The next morning, Konnech executive Eugene Yu was arrested for the alleged theft of poll workers’ personal information.

New Orleans Mayor LaToya Cantrell is facing the threat of a recall election and it’s not just the city’s rising crime that has petition signers enraged.

The two people behind the petition are both Democrats demanding the Democrat mayor leave office for her “failure to put New Orleans first and execute the responsibilities of the position,” according to Fox News.

In 2021, more than 150 officers left the New Orleans Police Department, despite a surge in murders and carjackings. Carjackings so far this year stand at 217, an increase of over 200 percent since 2019, according to the Metropolitan Crime Commission weekly bulletin.

But it’s the mayor’s exorbitant travel spending that has people up in arms.

She traveled to sister cities Ascona, Switzerland, and Juan Antibes-les-Pins on the French Riviera this summer, costing the City of New Orleans close to $45,000, including first-class international airfare with lie-flat seating.

The city’s travel policy requires employees to pay the difference in cost for work-related airfare upgrades, stating “employees are required to purchase the lowest airfare available … employees who choose an upgrade from coach, economy, or business class flights are solely responsible for the difference in cost,” Fox News reported.

But Cantrell hasn’t paid the near $30,000 bill from her first-class international flight upgrades over the summer.

She has claimed the visits are an investment in the city and necessary for her safety.

“My travel accommodations are a matter of safety, not of luxury,” The Times-Picayune/The New Orleans Advocate reported. “As all women know, our health and safety are often disregarded and we are left to navigate alone. As the mother of a young child whom I live for, I am going to protect myself by any reasonable means in order to ensure I am there to see her grow into the strong woman I am raising her to be. Anyone who wants to question how I protect myself just doesn’t understand the world Black women walk in.”

Yes, I’m sure the men and women who walk the streets of New Orleans at night have never know unthinkable fear of having to fly coach to Switzerland.

“Federal Law Does Not Exempt LGBT Employees From Bathroom, Dress Code, Policies, Judge Rules…A U.S. Equal Employment Opportunity Commission (EEOC) policy document from June 2021 overreached in its interpretation of the Supreme Court’s ruling forbidding employment discrimination based on sexual preference and gender identity, Judge Matthew Kacsmaryk of the U.S. District Court for the Northern District of Texas found. Texas sued over the guidance.”

Well, fellas, if you don’t want OPEC+ to be in a position where it can influence U.S. gasoline prices a month before the election, you need policies that minimize the U.S. market’s dependence upon the global oil market. This means maximizing U.S. oil production and expanding U.S. refinery capacity.

It would be a mild exaggeration to declare that the Biden administration hascompletely stopped issuing leases for oil and gas drilling on federal lands and in federal waters, but only a mild one. As the Wall Street Journal reported last month, “President Biden’s Interior Department leased 126,228 acres for drilling through Aug. 20, his first 19 months in office, the analysis found. No other president since Richard Nixon in 1969-70 leased out fewer than 4.4 million acres at this stage in his first term.” It’s not a complete halt, but it’s very close to one. This means that the U.S. is almost entirely dependent upon oil production from private lands.

The good news is that there’s still a lot of oil beneath private lands. As of July, the U.S. was producing 11.8 million barrels per day, an increase from the 11.1 million barrels per day produced in January 2021, the month President Biden took office. But before the pandemic hit in early 2020, the U.S. was producing 12.8 million barrels per day, and it even hit 13 million barrels per day in November 2019. We have the proven ability to produce about 1.2 million more barrels per day than we are, if we want to do so and our public policies encourage it. But right now, they do not.

The Biden administration keeps insisting that it’s doing everything it can to bring gas prices down, including releasing oil from the Strategic Petroleum Reserve — which is now at its lowest level in 40 years. But what’s in the SPR is oil, not gasoline, and oil must still be refined. You can’t just pump the stuff out of the ground and put it in your car.

U.S. refineries are running at full capacity, or just short of full capacity. This is why oil from the Strategic Petroleum Reserve releases got sent to Europe and Asia, because they had the room and equipment to turn it into actual usable fuel. The U.S. currently has no more spare ability to turn the oil from the reserve into stuff that will actually make your car move; yelling at the oil companies isn’t going to change what is fundamentally an engineering problem.

And Democrats absolutely refuse to let anyone build new oil refineries.

Multiple sources have confirmed that Nord 2 was full of natural gas; that it was full for at least months; and that said natural gas had never moved.

It. Just. Sat. There. For — allegedly — months.

During normal operations of a pipeline, you run a pig through fairly regularly. A “pig” is a bit of equipment pushed by the gas flow, and as it moves along it shoves water and hydrate slurry down to where it can be removed; and it scrapes compounds off the inside walls (hydrogen sulphide, I’m looking at you) that might be are probably eating your pipe.

Note the part above where the pigs are pushed by the gas. The gas in Nordstream 2 never moved. That means no pig ever went down the line to shove water out, move hydrate slurry, or stop H2S from corroding the steel of the pipeline.

As I said in the previous post — and I will continue to say — none of this rules out intentional Acts of War. There are idiots enough in that region that sabotage can’t be discounted.

“A lot of folks are running the White House. Joe Biden just isn’t one of them.” “Biden is surrounded with longtime D.C. power players, such as Ron Klain, Susan Rice, Anita Dunn, John Podesta, Gene Sperling – a veritable “who’s who” of Beltway knife fights and insider skullduggery. Throughout their long careers, they’ve never sought credit or voter approval. Just power.”

“NYC Mayor Declares State of Emergency over Influx of Illegal Immigrants. [New York City mayor Eric Adams] said at least 17,000 asylum seekers have arrived in the city by bus from other parts of the country since April.” Oh, a million illegal aliens come over the border into Texas and it’s no big deal, but 17,000 show up in your “sanctuary city” and suddenly it’s a problem!

“NYU Fires Chemistry Professor After Students Launch Petition Claiming His Course is Too Hard.” The lesson here seems to be that businesses shouldn’t hire NYU grads…

British blogger eats on £1 for a single day and has a very tough time of of it, even with foraging and scavenged condiments. Despite the dollar-pound exchange rate being so favorable, I don’t think I could do that on $1 a day shopping at HEB, and even if you made it $1.25, it would have to be three meals of ramen. Also, I don’t think I can even buy a single carrot at HEB (if I had wanted to), spaghetti is considerably more than 23¢ for 500 grams. $5 for $5, that I could do, and $30 for 30 days would be grim but very doable (price, pasta, and beans).

If you can remember all the way back to pre-Flu Manchu 2020, housing prices were soaring and there were a raft of articles decrying how commercial investors were snapping up housing as fast as they possibly could, pricing ordinary Americans out of the market.

Now, some two years later, it’s evident that a lot of those commercial investors kept buying right up through the peak of the market, and are now proceeding to lose their shirts on those deals thanks to the Biden Recession.

Take, for example, OpenDoor, the company that sends out those endless “We want to buy your home” letters. They promised investors they were going to use the Internet to revolutionize home-buying by flipping homes at scale and cut out the middle man. How well did they succeed?

Now that they’ve had a while to run their system, the answer is: Not so well.

Takeaways:

One thing I was unaware of: Commercial investors in residential real estate fund their purchases through variable interest rate debt.

OpenDoor’s outstanding debt balance “has ballooned from $271 million to $6.1 billion.”

Every point rise in interest rates costs OpenDoor $40 million more in interest rate payments.

“OpenDoor is truly a modern day house of cards. The company’s revenue grew from $1.8 billion in 2018 to over $8 billion in 2021. To grow they scaled, going from 18 markets to 44 markets in the U.S. In those four years, the company went from flipping 7,000 homes a year back in 2018 to now flipping 21, 000 homes most recently in 2021.”

“Despite OpenDoor’s top-line growth, the company has incurred loss after loss after loss, each bigger than the last, even in a strong rebound year in 2021. Where the company sold a record number of homes, OpenDoor incurred a record loss of over $600 million.”

Some math snipped. “OpenDoor would need to sell roughly sixty thousand homes a year just to break even with how much it costs the company to exist in its current burn rate. Every time the interest rate goes up a single point, OpenDoor needs to sell an additional 2,000 homes in order to offset that additional $40 million.”

The end of the video touches on how Zillow lost $881 million by trusting an algorithm that had them paying above-marker prices. We covered that briefly here some nine months ago. Here’s a video with more details:

But it’s not just OpenDoor and Zillow. Here’s a video that explains why all the large-scale commercial buyers of residential real estate (including those buying to rent it out rather than flip) are screwed by rising interest rates:

Takeaways:

The Fed “is now committing to not only continue increasing interest rates, they’re committing to keeping interest rates elevated for the foreseeable future.”

“These real estate investors are going to be losing money in the housing market on their investments, and that they are going to have to fire sale their portfolio as a result.”

“Over the last year, the investor profit or the cap rate in America is about 4.5%, which was pretty good in 2021, when interest rates were zero, but now that interest rates are projected to go to 3.8%, we can see that investors who buy real estate in America are basically getting very little premium over buying a short-term government bond.”

“As this investor demand continues to go down, home prices are also going to continue to go down in America, because in many markets investors were quarter of the demand, a third of the demand for homes over the last of couple years, and in some neighborhoods investors were 50—60% of the demand.”

“A lot of people think [commercial buyers pay] cash, but folks, it’s never cash, it’s always a bank in the background giving these hedge funds and private equity funds money to buy single-family homes.”

“They’ll give these hedge funds maybe 70—75% percent of the money to go do it, like a normal loan. The thing is, the loans that these Wall Street investors use to buy homes are often adjustable rate loans, where every time the fed hikes interest rates, the Wall Street investor has to pay more in debt service and interest on their existing portfolio.”

“We’re gonna get to a point soon over the next six months where these Wall Street investors are having to pay more to their bank and their warehouse lender than they’re going to receive in income and rent from their tenant. Like, literally, these Wall Street investors not only are going to see the value of their property going to go down, they’re going to begin losing money in terms of cash flow.”

So not only will investors have to sell, but frequently they won’t have any choice.

Because their lender, their bank, is going to do something called a margin call. At a certain point, they’re gonna say “Hey Wall Street buyer who I’m giving money to, the value of the homes has gone down and now you can barely afford to pay interest. You’re gonna have to now just pay us off, or pay us down,” and when the bank does that margin call, these investors are then going to be forced to sell off their portfolio, because they’re going to need the cash, causing a massive, widespread dump of inventory onto the U.S. housing market.

He doesn’t mention Austin by name in this video, but he does in another pegging it as the #5 market most likely to see price drops. “This is a market in absolute freefall.” “In the span of just five months, the number of homes for sale in Austin has increased from 1460 and February to nearly 8 000 in July.” He thinks home prices could go down by 40%. Naturally, as an Austin-area home-owner, I think that’s way too much, but I do expect significant retreats from the highs reached early this year.

He also thinks inflation is going to get worse (which is probably a good bet).

(In another video covering some of the same ground, he mentions BlackRock, one of the biggest boogeymen in public perceptions of buying residential real estate. Guess what? “BlackRock is not a big player in terms of owning, managing and buying real estate in the U.S.”)

Like the fear of Japan buying everything in the late 1980s, fear that institutional investors will make owning a home impossible for ordinary Americans turned out to suffer from the same recency bias, assuming that what is going on right this minute will continue for the foreseeable future.

Like assuming that the giant ants are unstoppable, or that Hispanics will always vote for Democrats, assuming that housing prices will always go up and that credit will always be cheap are categorical mistakes that the market will eventually punish you for making, and the companies that made it are now bleeding red ink.

People who sold during the bubble made out like bandits, and people who bought during it got screwed, but what can’t go up forever won’t. Bubbles pop. Absent government distortions of the market*, supply and demand have a way of adjusting.

Anyway, if you need to buy a house, nine months from now is probably going to be a great buyer’s market…

*And yes, lots of cities and states try their damnedest to prevent new housing from being built. I’m looking at you, California.

In The Before-Time, The Long Long Ago, prior to The Great Dot Com Bubble Bust, newspapers (remember those?) were filled with reports of day-traders, ordinary people who quit their day jobs to trade stocks. And what do you know! A whole bunch of them made money doing that! They must have been geniuses!

Few paused to test an alternative theory: They just happened to be riding the tail end of one of the greatest stock bubbles in history. It’s easy to pick stock market winners when there are lots of winners around.

Then the bust hit, and a whole lot of geniuses turned out to not be so smart after all, especially those who had backed such companies as Flooz and WorldCom.

Thanks in large measure to the SUPERgenius economic management of the Biden Administration, the world is now exiting an era of historically cheap money and entering a period of rising interest rates. A whole lot of business models that seemed to make sense during an era of cheap credit are going to look as retroactively foolish as Pets.com.

Vice will be mounting a new round of cost-cutting to try to stretch out its solvency while it searches for some sucker to buy it.

Vice does not make money. It will never make money. It just wants a series of Sugar Daddies willing to pump money into it forever to keep its overpaid, underperforming staff paid.

Snip.

The article says that they can only estimate what Vice is worth. They guess it’s worth, maybe, “at least one billion.” (And they owe $1.1 billion in debt?)

It was valued at $5.7 billion just a few years ago.

Ace of Spades also posted this Ryan Long video that I’m absolutely stealing:

As for the next media outlets to close, well, I’ve got to think any Bulwarkesque outlets whose entire raison d’être is subsidized Trump-hating is going to look like a luxury good during the Biden Recession.

High debt, high inflation and high interest rates are all recipes for disaster. And as those pools of liquidity dry up as cheap capital recedes, all the stranded starfish that so briefly thrived will find that they have no place to hide in the Biden Recession.