Margaret Thatcher said “The problem with socialism is that you eventually run out of other people’s money,” but Cuba appears to have gone them one better: Bad policies means that they’re now running out of their own money.

‘There is no money in the banks’: Cubans stand in line since dawn to cash their paychecks.

“There is no money in the banks to pay people, everyone is upset and they haven’t even given us an explanation,” said Leydis Tabares, a Cuban who resides in Camagüey, to Martí Noticias this Friday.

The problem is nationwide, said Cubans consulted from different provinces by our editorial team. The lack of cash in ATMs has caused state workers to be unable to withdraw the salary deposited onto their magnetic cards.

“In Sancti Spíritus, queues start forming since dawn because by nine or ten in the morning there is no cash left. Some employees have had to wait up to 45 days to be able to withdraw,” reported independent journalist Adriano Castañeda.

According to the journalist, the process of banking and the limitation of cash withdrawals is the cause of this crisis. “That system is a disaster,” he opined.

“A general reform is needed in Cuba, of all kinds, social, political, and economic,” commented independent journalist Guillermo del Sol. According to him, many owners of private businesses in the country have stopped depositing cash due to the same restrictions imposed by the regime.

“The money that Micro, Small, and Medium-sized Enterprises (MSMEs) deposited in the bank they couldn’t retrieve, so they stopped depositing money in banks. And since they are the ones carrying the weight of what little works within Cuba, the banks ran out of money. That’s what’s happening right now,” he explained.

So even in communist Cuba, small and medium size business are what keeps the economy running, and the commies are destroying them by withholding their access to their own money. That’s some mighty fine management, Lou.

In Guantánamo, the shortage of money for worker payment affects all sectors and is creating another type of business in the streets.

“Some charge for making the long queues in the early mornings for employees. There are also people who have cash and charge a 10% fee to deliver the amount of money they have on the card,” commented independent journalist Anderlay Guerra Blanco.

“When there’s an ATM with money, the queues are endless,” said opposition member José Rolando Cásares, who resides in Pinar del Río.

Independent journalist Vladimir Turró explained that in the capital, there are even people who line up pointlessly because at dawn, the bank doesn’t supply cash to the ATM.

“We’re talking about people who gather at banks, some even go to sleep at the ATMs, trying to get some cash, and so they spend days trying to withdraw money,” he said.

When Cuba in early August announced it was taking a major step towards electronic banking and a “cashless” society, the offices of fledgling small businesses across the communist-run country were left scrambling to figure out how to respond.

Most alarming to many budding entrepreneurs was a new 5,000 peso ($20) daily cap on cash withdrawals for businesses, one of several measures the government said were aimed at forcing Cubans to do their transactions electronically, via transfer, online payment and bank cards.

So commies limit bank access to a business’s own cash, and they’re shocked that businesses stop depositing it in banks.

Cubans are preparing for a new wave of inflation after the government last week rolled out details of an austerity plan that economists say will touch nearly every facet of the communist-run island’s already flailing economy.

I guess the austerity plan means the usually tactic of just printing more money is off the table.

The measures – which include price and tax increases and cuts in subsidies – will slow a soaring budget deficit forecast to exceed 18% of gross domestic product and set the stage for growth, according to Prime Minister Manuel Marrero.

Authorities have already announced gas at the pump will jump nearly five-fold on Feb. 1. But some economists say less visible government price increases such as on wholesale fuel and moving freight, as well as sales and import taxes, are sure to ignite substantial hikes on most products and services at the retail level.

“In economics, such prices are not increased in one area without affecting others,” Cuban economist Omar Everleny said in an interview in Havana. “And in general they are passed on to consumers. I think they will increase 400% to 500%.”

Reuters spoke with several Cubans in Havana who said prices were already rising following the announcements and in anticipation of the price hikes – and were set to soar further in the coming weeks.

Snip.

Inflation was 30% last year, cooling slightly from 38% in 2022, according to the government. Many economists say those rates fall short of reality as the government does not adequately monitor a booming informal market pegged to an informal exchange rate much higher than the official one.

In Holidays in Hell, P. J. O’Rourke talks about exchanging $480 for a gymbag full of cordobas in Sandinista Nicaragua. “You probably have to take economics over and over again two or three times at Moscow U before you can make cash worth this little.”

Government officials have announced wholesale fuel prices will double next month, freight transportation will jump between 40% and 60% in March and for the private sector import duties will increase five-fold. Private companies will also be charged a new 10% sales tax on wholesale transactions.

So prices are soaring, but people can’t get their own money out of the bank to make ends meet. So Cuba’s communist government has accomplished the rare feat of a liquidity crunch and soaring inflation at the same time.

A full scale ground war may or may not be developing in Gaza, the Biden recession claims bank branches, California declares itself a “child molesters across from schools” friendly zone, and lots of criminals making very poor decisions. It’s the Friday LinkSwarm!

There was also a screening today for reporters of footage of the atrocities carried out by the organization so many college lefties are cheering for.

I joined about 20 other journalists in a 14th-floor Manhattan conference room to watch the horrific video, which includes footage and images from a range of sources — such as cameras that Hamas attackers wore, dash cams, traffic cameras, and the phones of terrorists, their victims, and first responders — providing evidence of the crimes that Hamas carried out in Israel this month. The footage shows gagged and bound civilians burnt to an unidentifiable crisp; the casual and summary execution of people, including children, cowering under desks in the dark as they hide from terrorists wearing headlamps; the grisly decapitation of a Thai worker already bleeding from the stomach by a terrorist using a garden hoe; and other horrors.

In Gaza, by contrast, there are no visible military facilities, while Hamas fighters can shed their fashionable black outfits and dress like civilians. This will not, however, frustrate the Israeli offensive, which still has fixed, immovable targets. These are the deep tunnels — too deep for aerial bombing — that Hamas has been excavating and lining in concrete for more than 10 years, using construction equipment and vast quantities of cement donated by different governments and international organisations “to house refugees”. As a result, Gaza’s refugee “camps” do not contain a single tent. Instead, they are home to a forest of high-rise apartments, which is undoubtedly a good thing, except for the fact that both machines and cement were also diverted for tunnelling on the largest scale.

These tunnels house relatively sophisticated rocket-assembly lines, motor-assembly works, sheet metal and explosives’ stores, and warhead-fabrication workshops. More tunnels house Hamas command posts and its ordnance stores of small arms, mortars and rockets. Even deeper tunnels house its leaders’ lodgings and headquarters. Finally, there are the exfiltration tunnels, though there is no sign that they were used in the October 7 attacks, perhaps because their exits had been detected and blocked long before.

When Israel’s forces enter Gaza, they will engage any enemies who resist them, but they will not go looking for them. Their task is to escort combat engineers to their job sites — the camouflaged places from which tunnels can be accessed. How do they know where these entry points are? While Israel’s aerostats with cameras, satellite photography and the pictures generated by radar returns cannot reveal tunnels, they have been used to monitor where cement-mixer trucks have stopped over the years. They cannot pinpoint tunnel entrances by doing so, but they can at least identify places worth exploring with low-frequency, earth-penetrating radars or simple probes.

The obvious danger here is that, even before the escorting troops and combat engineers descend underground to fight off Hamas’s guards and place their demolition charges, they will keep losing casualties to snipers and mortar bombs on their way to the sites.

To minimise the danger, however, the Israeli army can rely on the most heavily protected armoured vehicle ever developed: the Namer infantry combat vehicle. As well as having significantly more armour than any other combat vehicle anywhere in the world, it uses an active defence weapon to intercept incoming anti-tank missiles and rockets, and also has machine guns to fight off infantry attackers. In urban combat, tank crews firing machine guns from the top of their turrets are desperately vulnerable, but the Namer’s crew remains “buttoned up” inside the vehicle, relying on TV screens to see the outside world and operate their weapons remotely. In 2014, the last time Israeli troops fought in Gaza, most were riding thinly armoured M.113s, which were easily penetrated by RPG anti-tank rockets, with some 60 soldiers killed and hundreds wounded. Not this time.

After they reach the suspected tunnel sites, the Namers will line up to form a perimeter — an improvised fortress — to protect the combat engineers as they go about their task. It is very likely that there will still be skirmishing before, during and after each de-tunnelling operation, with Hamas mortar teams in action, as well as snipers hidden in ruins. Fortunately, the Israelis will have their 70-ton Namers, as well as their post-2014 street-fighting training, to protect them.

And they will need that protection, as dismantling Hamas’s tunnel network will take time: the one certainty in all this is that the planting of demolition charges cannot be done quickly without suffering many fatalities. This means there will be at least two weeks of war in the Gaza strip — and even this optimistically assumes that the entire tunnel system in the evacuated northern part can be cleared in a week, allowing the Israelis to do the same in the southern sector, after evacuating the southerners and sending home the northerners. The Government’s vow to persist until the destruction of Hamas will be tested every day.

During the first week of October alone, U.S. banks closed a whopping 54 local branches…

Major US banks are continuing to close branches across the US, leaving an increasing number of Americans without access to basic financial services.

Bank of America axed 21 branches in the first week of October, according to a bulletin published by the Office of the Comptroller of the Currency (OCC) on Friday.

Wells Fargo shuttered 15, while US Bank and Chase reported closing nine and three respectively.

In total, some 54 locations had either closed or were scheduled to close between October 1 and October 7.

That is just one week!

Of course bank branches have been closing at a frightening pace for quite some time now.

Last year, U.S. banks shut down about 2,000 more branches than they opened.

I do wonder how many of those closed-branches are in crime-happy Soros-backed-DA zones…

Scenes from the decline of law and order in California: “Dude is a sex offender with a loophole that allows him to be near a school and he can set up the ‘free fentanyl’ sign because he doesn’t actually have the drugs on him.” Social Justice Warriors seem to love pedophiles almost as much as radical Muslim terrorists…

“NewsGuard, a company which claims to rate media outlets’ level of ‘trustworthiness’ and therefore has a meaningful influence over ad revenue, has been sued along with the Biden administration by Consortium News, which also named the Pentagon’s Cyber Command for “contracting with NewsGuard to identify, report and abridge the speech of American media organizations that dissent from U.S. official positions on foreign policy.”

Sometimes you start working on a story, only to find out there are too many unknowns to fairly approach it from a blogging angle, or because you run the risk of looking like a complete jackass. Such is the case with this story of APD Chief Data Officer Jonathan Kringen being charged with domestic violence. Kringen is married to Anne Kringen, who seems to have been brought into APD to wage social justice against it in the wake of the “rimagining Austin police” lunacy. “I think it’s fundamentally important to involve the community voice into policing in all spheres, including the academy, and I’ll work to foster a culture of inclusivity that reflects the needs of a city as diverse and exciting as Austin.” “Provide insight into institutionalized racism and explores the underlying causes of inequality as well as tools to address these causes.” No one should be the victim of domestic abuse, but it appears that neither Kringen should be employed by APD.

Trump’s gag order is so extreme that even the ACLU agrees his free speech rights are being infringed.

The truth about Postcolonialism: “We started with Frantz Fanon calling for violent revolution, and ended with Gayatari Spivak trying to use postmodern philosophy to attack western ideas of knowledge…Decolonization for Fanon was replacing all the colonizers with colonized people, using violence (or threats of violence) in order to free colonized people from the shackles of western influence…Decolonization is the systematic destruction of any and all western influence anywhere and everywhere by any means necessary.”

“On Thursday, 32-year-old veteran NYPD Officer Grace Rose Baez was arrested along with 42-year-old Casar Martinez and charged with conspiracy to distribute narcotics and the distribution of narcotics after they allegedly tried to sell large quantities of drugs to a federal informant between Oct. 9 and 29.” Even NYPD frowns on such shenanigans as setting up your own fentanyl distribution network while on duty…

And they say retail workers aren’t ambitious these days: “California Home Depot Employee Arrested For Allegedly Embezzling $1.2 Million.” “She was basically just manipulating the books on how much she was depositing” and would walk away with spare cash. I know theft in California is bad, but I’m pretty sure Home Depot has all those sales computerized, and is going to catch on when you keep coming up short…

Robber: “Stop! Hammertime!” Gun store owner: “Nope!” BLAM!

Now that Ken Paxton has been acquitted of all charges, Paxton can talk about the forces that conspired to push his bogus impeachment, which he does in this interview with Texas Scorecard’s M.Q. Sullivan.

MQS: “We had a secret investigation take place in the Texas House, with unsworn witnesses offering uh what John Smithy described as triple hearsay as evidence [and] no public hearings.”

MQS: “It’s been said that the Republicans were told this is a loyalty vote to the speaker of the House [Dade Phelan], and if it’s taking out Ken Paxton is what it takes to show loyalty, you have to do it.”

KP: “Democrats have figured out they can block vote. There’s 65 of them. Right now they block vote. They go to the Republicans and they say ‘We’ll get you elected as as speaker if you do what we say. We want to negotiate this deal.’ And so then that speaker who’s really controlled by the Democrats only needs 10 Republicans votes and then the Democrats effectively control [the House].”

KP: “I don’t think it’s any accident that the Biden Administration’s Department of Justice had two lawyers involved with the House investigating committee.”

KP: “I think the Biden Administration was tired of being sued. We’d sued him 48 times in two and a half years, and have been relatively successful with those cases, and I think that was a directive to the Democrats.”

KP: “[Phelan] was directed by the Democrats.” House Republicans need to be as united as Democrats.

KP: “They never had any evidence, and they obviously didn’t when they got to the Senate floor. But I think the message was ‘Do what we tell you to do or else.'”

MQS: “It seemed apparent to a lot of observers that the old Bush machine was ratcheted up against you. Johnny Sutton, Karl Rove, folks like that, who had not had much to say about Texas politics, their fingerprints were all over this from from very early on.” Sutton held several roles at the state and national level under George W. Bush, and was eventually appointed U.S. Attorney for the Western District of Texas.

KP: “This whole Coincidence of George P., after, what, 10 years of not having his license, on October 1st he asked the State Bar to get his license back. That just so happened to be that later that day that the these employees of mine told me that they’d turn me into the FBI. So somehow on that same day, before I knew about it, George P. is applying for his license.”

KP: “I think that that was the first sign that the Bush people were involved in this. And I think you can see from Johnny Sutton representing every one of these employees, that he was he’s doing this for free for the last three years, without ever sending a bill or even having a fee arrangement, that doesn’t make any sense either.”

KP: “Karl Rove wrote the editorial and he was directed, and I think given, that editorial by Texans for Lawsuit Reform. So you have all of these Bush connections that sought to get rid of me.”

MQS: TLR “is a group that has been kind of the de facto business lobby for more than two decades.”

KR: “They have definitely changed. They become a lobby group. They’re beholden to large, either corporate interests or individual interests, that don’t necessarily reflect the views of the Republican party.”

Sullivan suggests Paxtons problems may have started when he started targeting big tech and big pharma.

KP: “There’s a reason that we we’re looking at Big Tech, because they control the marketplace and they’re trying to control speech and control entire market activity on on advertising. There are issues related to them being deceptive in how they advertise, and also in what they tell consumers about what they’re doing with their information.”

KP: “Big Pharma obviously involved in this vaccine mandate, and potentially getting away with not actually testing their their vaccine, and telling us it does one thing when it does another.”

Paxton also brings up the role of banking as an industry that may not have been happy with him.

In another interview with Tucker Carlson, Paxton said he considers Texas Senator John Cornyn “a puppet of the Bush family” and will consider running against him in 2026.

A Soros-backed DA is stepping down, a Harvard prof lying about playing footsie with commies sentenced, and another Democratic fundraiser convicted of fraud. It’s the Friday LinkSwarm!

Good news, everyone! Soros-backed St. Louis Democrat DA Kim Gardner has resigned.

On Thursday, a progressive prosecutor who was notoriously funded by far-left billionaire George Soros announced her resignation, after months of bipartisan pressure to do so.

Fox News reports that Kim Gardner, the Circuit Attorney for St. Louis, announced that her resignation will be effective June 1st. Gardner was one of the first prosecutors in the country to be bankrolled by Soros, who has since expanded his efforts to other major cities across the country. She was first elected in 2016 and re-elected in 2020, largely due to Soros’ financial backing. Prior to her resignation announcement, she had declared her intention to run for a third term in 2024.

After years of criticism for being soft on crime and siding with criminals over victims, Gardner faced a whole new wave of criticism from both parties over an incident in February: Teenage volleyball player Janae Edmonson, who was visiting St. Louis from Tennessee for a tournament, was hit by an out-of-control car while crossing the road; although Edmonson survived, she had to have both of her legs amputated.

The driver of the car was Daniel Riley, a man who was out on bond while awaiting trial for an armed robbery case. It was later revealed that Riley had violated the terms of bond dozens of times, but was never arrested. When the blame turned to Gardner for failing to keep him off the streets, she falsely claimed that her office had attempted to have Riley jailed once again, only to be denied by a judge; there are no records of her office filing any such motion or otherwise seeking the revocation of Riley’s bond.

Following the Edmonson incident, Missouri Attorney General Andrew Bailey (R-Mo.) filed a petition quo warranto, the process by which the state attorney general can fire a prosecutor who has been determined to be neglectful of her duties. Bailey claimed that as many as 12,000 criminal cases have been dismissed due to Gardner’s failures, with another 9,000 having been thrown out right before they were set to go to trial, due to Garnder’s office refusing to provide evidence and speedy trials for defendants.

After Gardner’s announcement, Bailey released a statement demanding that she vacate her office immediately, rather than wait for another month.

Wagner Group chief Yevgeny Prigozhin said he will pull his mercenaries out of the meat grinder that is the Ukrainian city of Bakhmut on May 10, one day after Russia’s Victory Day Celebrations, which Russian president Vladimir Putin is expected to use to shore up support for the Russian invasion.

The Wagner Group, a well-known mercenary unit known to be one of Russia’s most competent fighting divisions, is leading the charge on Bakhmut, a city that that has gained outsized symbolic importance.

“I am withdrawing the Wagner PMC units from Bakhmut, because in the absence of ammunition they are doomed to senseless death,” Prigozhin said in full military fatigues and carrying an automatic weapon. The video he released showed him surrounded by masked Wagner fighters. Prigozhin also released a statement to the same effect.

His forces had no choice but to withdraw to rear bases to “lick the wounds,” said Prigozhin, as translated by the Washington Post. If Wagner goes through with the withdrawal, it would be viewed as catastrophic in terms of morale. The Russian invasion has ground to a standstill after large-scale Russian and Ukrainian offensives last year. Kyiv, which has been amassing ammunitions including tanks and fighter jets, is expected to launch a fresh counterattack in the very near future.

Prigozhin also launched a remarkable video tirade overnight on Telegram in which he displayed bodies of dozens of Wagner soldiers killed in Bakhmut. He angrily laid into the Russian Defense minister Sergei Shoigu and Valery Gerasimov, chief of the general staff of the Russian armed forces, for supplying Wagner with only 30 percent of the ammunition that’s needed.

The statement released today claimed that number was even lower, standing at 10 percent.

One caveat is that we’ve heard complaints from Prigozhin about his ammo supply before.

Russian soldiers dig trenches in horse graveyard in occupied Ukraine. Now they have anthrax.

“Biden CIA chief met with Epstein several times after financier convicted of child sex crime. Central Intelligence Agency Director William Burns had three meetings with Jeffrey Epstein in 2014, when the top spy official was deputy secretary of state and after Epstein was convicted of child sex exploitation.” (Hat tip: Stephen Green at Instapundit.)

“Harvard chemistry professor sentenced for lying about ties to CCP…Former Harvard University Chemistry Department Chair Charles M. Lieber was sentenced Wednesday to time served and over $80,000 in fines for committing fraud and for failing to disclose his connections to the Chinese Communist Party.” (Hat tip: Instapundit.)

New Jersey Democratic campaign strategist James Devine was charged with election fraud for allegedly submitting more than 1,900 fake petitions to help secure a 2021 Democratic gubernatorial primary ballot spot for candidate Lisa McCormick, New Jersey Attorney General Matthew Platkin announced Tuesday.

Devine was McCormick’s campaign manager and sent the fake voter certifications to the New Jersey Secretary of State’s Division of Elections via email in April 2021, but the New Jersey Democratic State Committee challenged his attempt days later, arguing that all the forms featured same the style of signature and at least one of the named voters was deceased, Platkin said.

A judge subsequently took McCormick off the primary ballot, and Devine is now charged with third-degree offenses concerning nomination certificates or petitions, tampering with public records or information and fourth-degree falsifying or tampering with records.

LoRA updates are very cheap to produce (~$100) for the most popular model sizes. This means that almost anyone with an idea can generate one and distribute it. Training times under a day are the norm. At that pace, it doesn’t take long before the cumulative effect of all of these fine-tunings overcomes starting off at a size disadvantage. Indeed, in terms of engineer-hours, the pace of improvement from these models vastly outstrips what we can do with our largest variants, and the best are already largely indistinguishable from ChatGPT. Focusing on maintaining some of the largest models on the planet actually puts us at a disadvantage.

How severe? How about $105 billion drop in loans in just two weeks.

“This credit crunch greatly increases the chances that America is going to have a deflationary recession or depression at some point in 2023. And, in fact, we could already be in it.” Ya think?

“We’re going to see the unemployment rate start to spike in America in the second half of 2023, In fact, we’re already seeing a big increase in unemployment claims data from the Federal Reserve shows that continued unemployment claims has surged since September.”

“We’re seeing a big surge in mortgage defaults right now across America, particularly on what’s called FHA mortgages. FHA mortgages are these first-time home buyer loans that the US government sponsors and allows people to only put three to five percent down. Well, these loans now have a 12% default rate in the most recent month of February 2023.”

Debt-to-income ration is now higher than it was at the pre-subprime meltdown peak in 2008.

“The Biden Administration has been very aggressive in wanting to expand mortgage access to low-income borrowers who can’t afford these mortgages. And they do this under the guise of expanding the benefits of home ownership to everyone, but really what they’re doing is they’re saddling at-risk economic households with a lot of debt near the peak of a housing bubble.”

“When banks tighten the belt and businesses can no longer get loans, businesses have to shut down, or what businesses have to do is, they have to start liquidating their holdings and taking whatever cash they have and use it to pay expenses. This is actually a concern of mine.”

“This bank credit crunch which is occurring right now could cause even more bank runs in the future” as people pull money out of the bank to cover expenses.

Quantitative tightening is back on.

“Mortgage application demand is on par with what we saw basically in the worst of the last housing crash in 2008, 2009, 2010, and so, no, there is no recovery.”

“The regular home buyer is still out of the housing market and is not returning.”

“The money supply in America is contracting…every other time in history it contracted, which was four times, we had a depression, a panic and a banking crisis.”

Cheerful enough. But if you’re a car dealer, things are even worse:

Banks are cutting off backing loans and providing credit to dealerships.

Not just used car dealers, but even national brand, nameplate dealerships.

This all started back in 2020, when banks started lending way too much money on cars that simply aren’t worth it, to consumers that simply couldn’t afford these payments, and shouldn’t have got the car in the first place…Let’s fast forward to 2023. We’re seeing record high repossession rates, and we’re seeing record high portfolio sell-offs, where people are just liquidating their paper because they don’t want to take on the risk of all these really bad auto loans, because they owe too much money. People are not making payments and they see the value of cars going down.

The fewer banks dealers can pit each other against for loan terms, the higher the interest rate consumers have to pay.

Dealers (not the banks) are also the ones who get screwed if a customer misses their first through third car payment.

Texas car dealer: “He was floored because he sells a lot of trucks between $45- and $65,000 trucks. Four of his banks told him that they’re no longer lending over twenty five thousand dollars.” (Previously.)

“I promise you this: it’s only gonna get worse.”

But wait! It gets worse!

“Capital One is going to start pulling their floor plans from dealers.”

“Floor plans” are the lines of credit dealers use to purchase cars to populate their lots, even the big nameplate dealers.

“Dealers are overexposed right now. They have paid way too much for their inventory and now they are having a hard time selling it.”

“It is so much harder now than it has been in the last two years to get people approved for loans to be able to sell these vehicles.”

“[Banks] do not want to get stuck holding the bag on these cars.”

“Dealers have been stupid. They have overpaid and they have too much inventory right now.”

“Some of these dealers, if they’re having cars 60, 90 days and maybe they’re getting a little bit behind on their payments [the] floor plan company will actually go to these dealers lots and they will take these cars that have been sitting too long, they’ll take them to the auction.”

“If they didn’t have the cash, the liquidity, to begin with, then they have to start liquidating cars, and they have to liquidate them fast to be able to pay their flooring lines…if they lose these flooring lines, they might as well not be in business, they don’t have the cash to be able to buy more inventory to be able to sell it to make more money.”

Banks pulling their floor lines could potentially crash the whole car market.

Things are going to get worse for car dealers before it gets better, and six months from now might be a great time to buy a car, assuming you’re not too busy shooting starving looters trying to steal your canned goods…

More on the collapse of Silicon Valley Bank, Syria gets spicy again, woke companies like Disney are having massive layoffs, and Sig Saur gets into the Killbot business. It’s the Friday LinkSwarm!

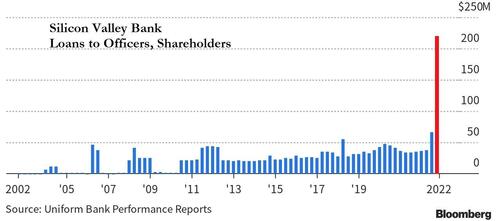

Courtesy of Bloomberg’s reporting, it appears that not only were insiders dumping their shares faster than syphilitic hooker, there were loading up on loans from the bank at a scale that makes a mockery of any regulatory oversight…

”

Yes, that’s real.

Loans to officers, directors and principal shareholders, and their related interests, more than tripled from the third quarter last year to $219 million in the final three months of 2022 – a record dollar amount of loans going back over 20 years.

Many questions come to mind – what were the terms, who were the recipients, what was the collateral?

But, sadly, we will likely never know.

However, we do note that the banking execs may be facing a serious shortfall (like their bank): if the loans were collateralized by SVB shares for example, those shares are now worthless, leaving the loan-heavy C-suite left to come up with the cash to repay the loans (and no, these loans don’t disappear with the bank’s liquidation).

Between that and the insider share dumping, people need to go to jail.

After the implosion of the FTX crypto exchange run by Sam Bankman Fried, questions of due diligence and competency immediately arose, suggesting that perhaps the company mishandled assets “accidentally” and that Fried was naive and “in over his head.” Numerous central bank officials and globalist organizations jumped into the debate almost immediately, arguing that FTX was a perfect example of why centralized regulation of crypto and digital currencies was necessary. They claimed that without oversight by banking elites, disaster was inevitable.

Of course, what they did not mention was that FTX and Sam Fried already had extensive connections with globalist groups including the World Economic Forum. In fact, the very basis of Fried’s business model was the WEF’s “Stakeholder Capitalism” theory, which he often referred to as “Effective Altruism.”

Stakeholder Capitalism is essentially the opposite of free markets – It is a socialist/globalist framework which uses corporations as a kind of economic enforcement tool. Corporations are already highly socialistic in their operations, and their existence is completely dependent on their special relationship with government. Corporations are created through government charter, enjoy special protections under “corporate personhood” laws and avoid direct consequences for criminal activities through limited liability.

Many corporations are not even allowed to fail because governments backstop their operations. That’s socialism, not free markets. However, “stakeholder capitalism” expands on this dynamic a hundred-fold.

Where free markets assert that businesses must make profit their primary objective for the overall economy to function, the WEF asserts that companies including banking institutions have a social obligation that goes beyond making money. To the typical leftist this probably sounds like a Utopian vision filled with promise, but to anyone that actually understands economics it sounds like a recipe for the collapse of civilization.

The WEF paints stakeholder capitalism an effort to reign in the power of the corporate system in favor of social causes. In reality, it’s a way to give corporations ultimate power over everything, including ultimate influence over public behavior.

We have seen extensive evidence of this through widespread corporate ESG investment programs implemented in the past several years. It is no coincidence that the invasion of woke ideology into the mainstream happened at the exact same time that ESG-based lending accelerated.

The institutions lending to various companies were able to set social rules for access to credit, and these rules required businesses to adopt far-left politics in their marketing and policies as a result. Stakeholder capitalism is about homogenizing all business into a single ideological entity – Instead of competing with each other for market share through innovation, companies have been abandoning merit based competition and are colluding to saturate the mainstream with social justice cultism, climate change propaganda and globalist rhetoric.

By making corporate elites “responsible” for society, we give them the power to engineer society.

However, the WEF’s model of false altruism is turning out to be a disaster for corporate survival. I have to wonder now if this was the intent all along – To create a kind of ESG fueled woke financial bubble that was always intended to come crashing down, leaving the western world in ruins.

Snip.

Looking into SVB’s operational history, the company was a woke nightmare.

Take a gander at their 66 page ESG report compiled in 2021 to get a sense of how far to the extreme political left the bank was. SVB is the pinnacle example of why “Get Woke, Go Broke” is more than a mantra, it’s a rule.

Digging even deeper we then find that SVB’s leadership was highly involved in the WEF and their Stakeholder Capitalism Metrics (SCM), along with corporate governance. SVB was not only implementing every single policy the WEF outlines in its agenda, they were reporting back to the WEF on their progress.

SVB’s capital exposure was heavily tied up in securities, but also venture capital for woke tech startups, climate change related projects and leftist activist groups which qualified for ESG loans; everything from BLM to Buzzfeed. In other words, they were investing aggressively into money-pit projects that devoured cash and gave nothing back. The real question is, how many US banks are involved in ESG and WEF operations at the same level as SVB? Dozens? Hundreds?

“U.S. Carries Out Airstrikes in Syria after Iranian Drone Kills U.S. Contractor, Wounds Five Service Members.” As I’ve mentioned before the withdrawal of most U.S. troops from Iraq and Syria doesn’t mean all. And the same goes for Africa.

“56% of liberal white women age 18-29 have been diagnosed with a mental health condition.” Well, you already said “liberal”…

Louisiana state Rep. Francis Thompson switched from the Democratic to the Republican Party, given Republicans a super-majority in both houses and thus the ability to override any veto by Democratic Governor John Bel Edwards. ““The push the past several years by Democratic leadership on both the national and state level to support certain issues does not align with those values and principles that are a part of my Christian life,” said Thompson.

World Athletics, the governing body for international track and field competition, has banned men from international competition. “I’ll take ‘Headlines no one in the 20th century would understand’ for $600, Alex.”

“Dallas Bar Cancels All-ages Drag Event.” Funny how the threat of having your TABC license yanked concentrates the mind…

Get Woke, Go Broke Part 1: After a string of expensive bombs and streaming losses, Disney to lay off 7,000 employees.

Get Woke, Go Broke 1.5: “Woke Marvel Producer Victoria Alonso Gone From MCU.” She was one of the central figures pushing Disney to adopt a pro-groomer position in Florida. The ostensible reason for her firing was breach of contract for producing a non-Marvel movie, but a lot of industry insiders think her outspoken wokeness was a key reason for her getting the axe.

Get Woke, Go Broke Part 2: “Twitch Streaming Service To Sack 36% Of Employees.”

SIG Sauer announced late last week it has acquired General Robotics, one of the world’s premier manufacturers of lightweight remote weapon stations and tactical robotics for manned and unmanned platforms as well as anti-drone applications. The companies have been working in concert for some time, a fact made obvious at January’s SHOT Show when they debuted a Polaris ATV equipped with a General Robotics PitBull remote weapons station that aimed and fired the vehicle-mounted SIG MG 338 belt-fed machine gun remotely.

“This acquisition will greatly enhance SIG Sauer’s growing portfolio of advanced weapon systems,” said Ron Cohen, president and CEO of SIG Sauer. The team at General Robotics is leading the way in the development of intuitive, lightweight remote weapon stations with their battle-proven solution.”

I meant to mention something about the Credit Suisse situation in Friday’s LinkSwarm but ran out of time. I’m not an expert on European banking in general or Swiss banking in specific. (As opposed to being a squinty, one-eyed, myopic man in the land of the blind sort of expert on American banking, which is not very.) But it’s a big story, so I suppose I should post something about Credit Suisse.

So here’s something.

First, as of this writing, it appears that fellow Swiss bank UBS is about to take over Credit Suisse, probably with the financial backing of the Swiss National Bank (SNB)

Late on Thursday, just hours after the SNB had launched the first (of many) bailout attempts of Swiss banking giant Credit Suisse, Bloomberg blasted the following headline:

*UBS, CREDIT SUISSE SAID TO OPPOSE IDEA OF A FORCED COMBINATION

This lack of enthusiasm by UBS to acquire its struggling rival of course forced the Swiss National Bank to front CS a CHF50 billion credit line to hold it over for the next four days amid a furious bank run, one which we said would be woefully insufficient to restore confidence in the collapsing lender, and which we probably used up in just a few hours.

Then, late on Friday, both banks “unexpectedly” changed their minds and we got the following 180 degree U-Turn report from the FT:

*UBS IN TALKS TO ACQUIRE ALL OR PART OF CREDIT SUISSE: FT

So a deal is inevitable after all… but as always, there is a footnote one which we predicted yesterday when we said that a deal would only happen if the acquiring bank – in this case UBS – got a full central bank backstop.

That now appears to be the case with Bloomberg, Reuters and the WSJ all reporting that UBS is asking the Swiss government for a backstop to cover future risks if it were to buy Credit Suisse Group AG, after the Swiss National Bank and regulator Finma have told international counterparts that they regard a deal with UBS as the only option to arrest a collapse in confidence in Credit Suisse. The FT reported that deposit outflows from the bank topped CHF10bn ($10.8bn) a day late last week as fears for its health mounted.

Here’s Patrick Boyle on how Credit Suisse brought itself low:

One big take-away: It wasn’t bad investments per se that wrecked confidence in the bank, it was involvement in a series of scandals, as they have “a strong, liquid balance sheet.” “Credit Suisse has instead been plagued by repeated scandals. From spying on a former employee, a criminal conviction for allowing drug dealers to launder money, a massive leak of client data to the media, Archegos, Greensill, Mozambique ‘tuna bonds,’ the list is too long.”

UK courts are at the heart of a spate of litigation arising out of the Mozambique “Tuna bond” or “hidden debt” scandal. The scandal involved $2 billion of bank loans and bond issues from Swiss bank Credit Suisse and Russian bank VTB. The bank loans were taken out in secret by Mozambican state-owned companies, without the legally required approval of the Mozambique Parliament and backed with hidden government guarantees.

The loans were intended to finance contracts between the state companies and a Lebanese-UAE based ship builder, Privinvest, between 2013-2016 for three maritime projects. These projects were intended to boost maritime security and develop the country’s fishing industry. However, a 2017 audit by Kroll found that $500 million of loans could not be accounted for and that Privinvest may have over-inflated prices by $713 million. The audit also found that $200 million of the loans were spent on bank fees and commissions.

So it turns out that Mozambique’s political and business elites are at least as corrupt as our own political and business elites.

Good to know.

Ironically, according to Boyle, the reason European banks may be in better shape than our own is because they had to deal with the fallout of the Euro crisis. “This is not because European banks are very good — it is precisely because they have historically been quite bad.”

Practically every banking regulation in existence commemorates a time when things went badly wrong, and Europe spent a decade toughening up banking regulation because it went through a rolling multiyear euro crisis. The European regulators have a detailed set of standards for testing interest rate risk, with the idea that they will be applied to every significant bank in Europe. Unrealized losses are not ignored under this regime and the global Basel standards on stable funding are applied across the entire banking sector. This is quite different to the regulations applied to community banks in the United States who lobbied the government for regulatory exemptions over the years.

“The economist Matthew Klein argued in a blog post that banks today can be seen as speculative investment funds grafted on top of critical infrastructure, and that this structure is designed to extract subsidies from the rest of society by threatening civilians with crises if the banks’ bets are ever allowed to fail.”

Was Credit Suisse infected with the radical transexual social justice warrior madness as the rest of our elites? Of course they were:

Fear not! The banks that are failing are not woke! OK, they’re woke, but they’re not broke! OK, they’re broke, but they are not without allies who realize that they must support this house of cards freak show. OK, the contagion will take the little people down, but so what? https://t.co/D76Y8svHTL

The more I hear about the Silicon Valley Bank collapse mentioned in Friday’s LinkSwarm, the worse it sounds.

I saw a snippet of Gary Tan, CEO of startup fund Y Combinator, talking about how bad it is. I can’t find a video of the full interview online, but evidently it was excerpted on Bannon’s War Room podcast and there’s a transcript.

[Interviewer]: How many of these startups that have been through Y Combinator, for example, have their cash tied up at Silicon Valley Bank? And over this weekend, I’m gonna try to figure out how they’re gonna make payroll next week. Do they have to go to investors and say, can you front me some cash so that we can stay alive?

[Tan]: We have funded about 3,000 active startups right now. I would guess that this affects more than 1,000 startups. And about a third of those startups will not be able to make payroll in the next 30 days in the current configuration. As of this morning, RIPLING, which many startups use to manage payroll and benefits, transfers were not being processed by SVB for payroll.

And so that’s a really existential threat for companies broadly. These are founders who are texting me and calling me saying, do I need to furlough my workers next week? Because I do not have other bank accounts, you know, a Google or a Facebook or even companies farther along with a Treasury Department. They’re going to be able to weather this, but if SVB is your only bank, it’s actually an existential risk. You’re going to go out of business if you can’t pay payroll. And that starts Monday.

That transcript also has this sobering figure: “97% of the deposits at Silicon Valley Bank. 97% are not insured by FDIC because they’re in accounts over $250,000. These company accounts that would be $169 billion.”

So what was Silicon Valley Bank doing rather than properly managing their risk profile? Banks have Chief Risk Officers whose job is to make sure their risk exposure ratios don’t get out of whack. Well, guess what? SVB didn’t have one for some nine months. “SVB’s former head of risk, Laura Izurieta, who formerly performed a similar role for Capital One, left the bank in April 2022. She wasn’t replaced until January 2023 when the bank hired Kim Olson, formerly of Japanese bank Sumitomo Mitsui.”

But don’t worry: SVB had CRO for the bank in Europe, Africa and the Middle East who was entirely focused…on Social Justice and ESG.

Jay Ersapah, who acts as CRO for the bank in Europe, Africa and the Middle East and who describes herself as a ‘queer person of color from a working-class background’ – organized a host of LGBTQ initiatives including a month-long Pride campaign and implemented ‘safe space’ catch-ups for staff.

In a corporate video published just nine months ago, she said she ‘could not be prouder’ to work for SVB serving ‘underrepresented entrepreneurs.’

Professional network Outstanding listed Ersapah as a top 100 LGTBQ Future Leader.

‘Jay is a leading figure for the bank’s awareness activities including being a panelist at the SVB’s Global Pride townhall to share her experiences as a lesbian of color, moderating SVB’s EMEA Pride townhall and was instrumental in initiating the organization’s first ever global “safe space catch-up”, supporting employees in sharing their experiences of coming out,’ her bio on the Outstanding website states.

It adds that she is ‘allies’ with gay rights charity Stonewall and had authored numerous articles to promote LGBTQ awareness.

These included ‘Lesbian Visibility Day and Trans Awareness week.’

Separately she was also praised in a Facebook post by the group ‘Diversity Role Models,’ a charity which campaigns against homophobic, biphobic and transphobic bullying in UK schools.

Being in Silicon Valley, I’m betting that the entire company was whole hog backing DEI, ESG, Transwhatever and the entire rainbow of victimhood identity politics acronyms.

In a strong economy, you can get away with a bit of shareholder-value-destroying, virtue-signaling luxury goods as long as your core business is strong. But with rising interest rates, Biden Inflation, the Biden Recession and the gale winds of deglobalization, taking your eye off the ball to focus on anti-reality SJW garbage is a recipe for disaster.

And all the startups that relied on SVB for their banking are well and truly screwed.

Update: Uncle Sugar is evidently going to make all depositors whole at both SVB and newly insolvent Signature Bank. This relatively early intervention may indeed be the best move to prevent bank runs at other institutions, and may reflect a change in philosophy since 2008. (It’s a thorny subject.) But it does make me think that a lot of well-connected depositors were screaming in the ears of Washington to be made whole at the taxpayer’s expense. What do you think the odds are that the same consideration wouldn’t be given to, say, a Texas bank that specialized in underwriting oil and gas ventures?

Here’s hedge fudge manager/university professor Patrick Boyle goes into detail of just how it went down.

“Silvergate’s importance in the recent crypto boom is possibly best described by a now-deleted testimonial from the bank’s website: ‘Life as a crypto firm can be divided up into before Silvergate and after Silvergate.It’s hard to overstate how much it revolutionized banking for blockchain companies.’ The testimonial was written by a millennial who still lives in his parents’ basement playing video games and has had some recent run-ins with the law. His name is Sam Bankman Fried.”

“If we go back ten years, Silvergate was a small San Diego based real estate lender that transformed itself into the go-to bank for the crypto industry.”

“Silvergate invited in crypto entrepreneurs and asked them what problems they were trying to solve and how the bank could be helpful. After this, the bank transformed itself and grew rapidly. It went public in late 2019 at a share price of $13, and a year later the stock price had risen by 1,580% as it became a key interchange point between dollars and cryptocurrencies.”

“Major Silverlake clients included Paxos, bitFlyer, Kraken and also innovators in atonal rock music – Mars Junction…” [This is an inside joke. Mars Junction is the band of Cameron & Tyler Winklevoss, AKA the WInklevoss Twins of Facebook investing controversy] “…who also had some involvement in the Crypto industry. FTX and Alameda were also big customers.”

“The bank’s growth mirrored the growth of the crypto industry, and it declined alongside that industry too, announcing in a regulatory disclosure earlier this week that it plans to wind down operations in the face of ‘turmoil in digital currency markets.'”

Last week Silvergate had announced that they would be unable to file an annual report with the SEC on time due to a weakening in their capital position. They announced that they might be forced to close at that time, blaming growing problems, in part on pending investigations into their operations. The filing confirmed that Silvergate is being investigated by the US Department of Justice.”

“Customers rushed over the last few months to pull money out of Silvergate. In January they reported that customers had withdrawn more than $8 billion, forcing them to sell held-to-maturity assets to fund the run, accruing losses on the sale of those securities of $718 million dollars.”

Why was Silvergate so important in the world of crypto? Well, people who trade cryptocurrencies often want to use dollars to buy crypto, or they want to sell crypto and receive dollars and the dollar side of those transactions is where things get bogged down. If you are transferring large sums of money to buy crypto, you need to deal with the US banking system, who might ask you a lot of questions relating to anti money laundering regulations. Crypto people hate questions like this. Similarly, if you just sold some crypto and want to deposit the dollars you received, most banks will have a long list of questions about the source of your funds, and there is a really good chance that they will simply refuse to do the transaction. It is going to be a struggle for a US regulated financial institution to show their regulator that they have done enough due diligence to be sure that your funds are not the proceeds of crime. And the last thing a bank needs is to be accused of money laundering; they would rather just simply not deal with suspicious transactions.

“For this reason, stablecoins like Tether and Terra exist – or existed.” If you weren’t paying attention, the value of theoretically stable Terra crashed hard last year.

“If you can convert your dollars into crypto once, you can then buy stablecoins that are supposed to always be worth a dollar, and then instead of buying and selling crypto, with actual dollars you buy and sell crypto with dollar-denominated stablecoins, your money can stay ‘on chain.’ The problem with that, is that you have to trust the stablecoin issuers, and they, for some reason, don’t always seem trustworthy. They won’t really tell you where the money is.”

“They’ll sometimes announce that they are going to be audited by a top 12 auditor (I’m not really sure what a top 12 auditor is – but when you hear that – you know you are getting number 12 on the list), and you start to wonder if Friehling & Horowitz made that list.” Friehling & Horowitz were Bernie Madoff’s auditors.

“If you have deposited your dollars with a crypto exchange or a stablecoin provider, they still need to deposit them somewhere. They need a bank too. Now (of course), another way of dealing with this banking issue, might be to lie to your bank about what your account is being used for (SBF and the team at FTX did that), but the technical term for ‘lying to your bank’ is Bank Fraud (as Sam Bankman-Fried just found out) – and you can get in trouble for that.”

“There was significant demand for a “crypto friendly bank” and Silvergate was willing to fill that role, when no other bank was willing to take that risk. Silvergate weren’t just crypto friendly either, they built their own payments network called the Silvergate Exchange Network to (according to their marketing documents) enable the efficient movement of U.S. dollars between participants 24 hours a day, 7 days a week, 365 days a year.”

“As you might imagine, Silvergate (being the only bank that would deal with them) attracted a lot of big crypto customers, as these customers were able to open up accounts without lying too much.”

“Silvergate dealt with most of the big players in the industry and they were an actual US regulated bank with excruciatingly detailed audited financial statements and capital regulation. This meant that your money was safe at Silvergate, unlike at the other venues we just went over.”

“The beauty of dealing with these crypto customers, crypto exchanges, [was] that because you don’t have any real competition in this space, you don’t really have to pay them any interest on their deposits. You could take the billions of dollars they deposit with you, put it all in treasuries, and you get to keep all of the interest. You’ll probably have to spend some of the profits on lawyers to keep the regulators at bay, but overall you might have a profitable business. But that’s boring right? And no one gets involved in crypto for a boring life…”

“They had a product called SEN Leverage direct lending, where they would lend people money collateralized with bitcoin. Exchanges could also borrow dollars collateralized with bitcoin for corporate treasury and other business purposes. In January, they announced that total SEN Leverage commitments were $1.1 billion dollars and that all of their SEN Leverage loans ‘continued to perform as expected, with no losses or forced liquidations.’ So, as crazy as that business might sound, it was not really the source of their problems.”

“As of September, 2022 their balance sheet showed about $11.4 billion of ‘securities,’ meaning bonds: Treasury securities, mortgage-backed securities, agency bonds and so on and $1.4 billion of ‘loans,’ meaning the Bitcoin loans and some other real-estate lending. They had $13.2 billion worth of deposits at the end of September, most of them being from crypto companies – so non-interest paying deposits, the best kind.”

“The problem for Silvergate was that when FTX was exposed as being insolvent, crypto investors were considerably less willing to leave their cash on exchanges.”

“They asked for their money back from the exchanges, meaning that the crypto companies had to ask for their money back from Silvergate, so Silvergate was faced with a good old fashioned bank run – driven not by a loss of faith in Silvergate, but by a loss of faith in crypto exchanges. By the end of December, noninterest bearing deposits at Silvergate fell from $13.2 billion dollars to just $3.9 billion dollars.” Yowzers! It’s hard to expect any bank to survive an outflow of 2/3rds of their deposits in such a short period of time.”

“There is a good chance that if you had an account at a crypto exchange, that exchange banked with Silvergate, and if you closed your account and cashed out, the cash came from a deposit at Silvergate.”

“There were other FTX related problems too. When prosecutors started looking into the collapse of FTX, their attention was drawn to their banker – Silvergate, for hosting accounts connected to Sam Bankman-Fried. Now, a big problem for Silvergate, was that – with their money all tied up in bonds or lent out, Silvergate had to come up with around 9 billion dollars to pay out these withdrawals.”

“Their accounts show that by the end of December they had sold half of their bonds and had controversially borrowed $4.3 billion from the Federal Home Loan Bank of San Francisco, a government institution that is in place to give short-term secured loans to banks that have a short-term liquidity problem.” That, and the FTX connection, attracted the attention of Washington D.C.

In September Silvergate had shown 3.1 billion dollars’ worth of bonds as being “held to maturity” and 8.3 billion dollars’ worth of bonds as being available for sale. The difference between these two classifications (from an accounting perspective) is that the available for sale bonds have to be marked to market – or held on the books at their fair market value, while the “held to maturity” bonds could be marked at their cost price. By the end of December there were no “held to maturity” bonds left on the balance sheet, meaning that they had either been sold, or reclassified as available for sale. One way or another, interest rates had gone up a lot in 2022, and these bonds were worth a lot less than they were being carried on the balance sheet at.

So they might have skated by if rising interest rates hadn’t wrecked their mark-to market.

The sale resulted in a loss of $751.4 million during the fourth quarter of 2022 and in addition, the company recorded a $134.5 million dollar impairment charge related to an estimated $1.7 billion dollars of securities it “expects to sell in the first quarter of 2023 to reduce borrowings.” This is because reclassifying some of the bonds to “available for sale” meant that they now had to be marked to market and that the loss had to be recognized under GAAP accounting rules. Silvergate also had to write down a $196 million dollar investment in “certain developed technology assets related to running a block-chain-based payment network” that it had bought in January 2022. So, all in, there was a net loss of over a billion dollars in the fourth quarter of 2022.

“Bank capital requirements are ‘risk-based’ and need to be kept above 4% to be ‘adequately capitalized’ and above 5% to be considered ‘well capitalized.’ Different types of assets have different risk weights, and this is done to keep deposits safe.”

“A bank that makes a lot of mortgage and business loans might have a capital requirement of around 8%, and assets like bitcoin have a 100% capital requirement, meaning that a bank would need to have $100 of capital for every $100 of bitcoin on its books.”

“In September Silvergate was fine, as despite the Bitcoin loans, most of their money was in high quality bonds that had zero risk weights. But when their deposits went out the door and they had to sell assets and realize a billion-dollar net loss, they were left in a situation where an additional $19 million-dollar loss would but their capital below 5% and they would no longer be considered well capitalized.”

“Last week Silvergate announced that they had sold additional debt securities in January and February to repay the company’s outstanding advances from the Federal Home Loan Bank of San Francisco and that they ‘expect to record further losses related to the other-than-temporary impairment on the securities portfolio.’ These additional losses they said would ‘negatively impact the regulatory capital ratios of the company and could result in the bank being less than well-capitalized.” And that’s when Brunhilda strode on stage to give her farewell.

“This announcement caused the stock price to half that day and according to Bloomberg caused Coinbase, Galaxy, Paxos and other crypto firms to announce that they would stop accepting or initiating payments through Silvergate. These customers leaving were the final nail in the coffin, as they reduced deposits even further.”

“A bank run, on a real bank, caused by crypto related losses and crypto volatility.”

“Matt Levine at Bloomberg argues that one way to think about the rise and fall of Silvergate is that the crypto boom was at its heart a low-interest-rate phenomenon. People started speculating in crypto because interest rates were below the rate of inflation, and so Silvergate was hugely exposed to interest-rate risk simply because of its exposure to its crypto customers.”

“Rising interest rates caused the deposits to evaporate at the same time as the assets backing those deposits fell in value. Levine argues that (with hindsight), Silvergate’s risk management – a year ago – should have been laser-focused on the risk of rising interest rates crushing both its assets and its customers, and it should have hedged that risk one way or another.”

I know all this is long and a bit detailed and technical, but I wanted to point it out as an example of how a cascading chain of events (much like the Piper Alpha disaster) caused a failure, mainly how massive fraud on the basis of one crypto space player and rising interest rates ended up bankrupting a real bank in the real world.

Mutiny! Bank runs! Twitter files! It’s a ginormous LinkSwarm full of interesting (and alarming) links!

And I finally get a chance to talk more about the FTX scandal.

The Twitter files revelations continue to roll out. And Democrats aren’t happy that the workings of their thought police apparatus are being unmasked.

As one might expect, the Judiciary hearing on the “weaponization” of federal agencies, featuring Matt Taibbi and Michael Shellenberger as witnesses was full of fireworks, facts, and ad hominem friction.

Out of the gate, Ranking Member Democratic Del. Stacey E. Plaskett labeled the two “so-called journalists” as dangerous and a “threat” to former Twitter employees.

She claimed that Republicans brought “two of Elon Musk’s ‘public scribes'” in “to release cherry-picked out-of-context emails and screenshots designed to promote his chosen narrative – Elon Musk’s chosen narrative – that is now being parroted by the Republicans” for political gain.

“I’m not exaggerating when I say you have called two witnesses who pose a direct threat to people who oppose them,” Plaskett said after the video.

Chairman of the House Judiciary Committee, Republican Rep. Jim Jordan of Ohio, had a simple response to her accusations:

“It’s crazy what you were just saying.”

“You don’t want people to see what happened,” Jordan continued.

“The full video, transparency. You don’t want that, and you don’t want two journalists who have been named personally by the Biden administration, the FTC in a letter. They say they’re here to help and tell their story, and frankly, I think they’re brave individuals for being willing to come after being named in a letter from the Biden FTC.”

Taibbi was having none of it.

Matt Taibbi epic comeback:

"Ranking Member Plaskett, I'm not a 'so-called journalist'. I've won the National Magazine Award, the I.F. Stone Award for Independent Journalism, and I've written 10 books including 4 NYT Best Sellers." pic.twitter.com/crXlWjScEr

— Citizen Free Press (@CitizenFreePres) March 9, 2023

As Glenn Greenwald chimed in from Twitter: “To Democrats, “journalist” means: one who mindlessly and loyally endorses DNC talking points. ”

Unshaken, Matt Taibbi continued, when he was allowed to respond, laid out what he and Shellenberger had found in their research of The Twitter Files:

“The original promise of the Internet was that it might democratize the exchange of information globally. A free internet would overwhelm all attempts to control information flow, its very existence a threat to anti-democratic forms of government everywhere,” Taibbi said.

“What we found in the Files was a sweeping effort to reverse that promise, and use machine learning and other tools to turn the internet into an instrument of censorship and social control. Unfortunately, our own government appears to be playing a lead role.”

Taibbi pointedly added that “effectively, news media became an arm of a state-sponsored thought-policing system.”

“It’s not possible to instantly arrive at truth. It is however becoming technologically possible to instantly define and enforce a political consensus online, which I believe is what we’re looking at.”

Democrats only response to Taibbi and Shellenberger’s facts was to get personal…

Snip.

As we detailed earlier, journalists Matt Taibbi and Michael Shellenberger are testifying before the House Judiciary Committee’s Select Subcommittee on the Weaponization of the Federal Government today. Both journalists were involved in the ‘Twitter Files’ disclosures, in which we learned that the government was directly involved in censoring disfavorable speech.

“Our findings are shocking,” writes Shellenberger at his blog. “A highly-organized network of U.S. government agencies and government contractors has been creating blacklists and pressuring social media companies to censor Americans, often without them knowing it.”

Ahead of the appearance, Taibbi released his prepared remarks. He also dropped a new and related Twitter Files mega-thread on ‘THE CENSORSHIP-INDUSTRIAL COMPLEX’ which will be submitted to the Congressional record which, according to Taibbi, ‘contains some surprises.’

But Twitter was more like a partner to government. With other tech firms it held a regular “industry meeting” with FBI and DHS, and developed a formal system for receiving thousands of content reports from every corner of government: HHS, Treasury, NSA, even local police…

But equally concerning was how those driving The Narrative used NGOs that agreed with them as Arbiters of Truth.

We came to think of this grouping – state agencies like DHS, FBI, or the Global Engagement Center (GEC), along with “NGOs that aren’t academic” and an unexpectedly aggressive partner, commercial news media – as the Censorship-Industrial Complex.

Who’s in the Censorship-Industrial Complex? Twitter in 2020 helpfully compiled a list for a working group set up in 2020. The National Endowment for Democracy, the Atlantic Council’s DFRLab, and Hamilton 68’s creator, the Alliance for Securing Democracy, are key…

Twitter execs weren’t sure about Clemson’s Media Forensics Lab (“too chummy with HPSCI”), and weren’t keen on the Rand Corporation (“too close to USDOD”), but others were deemed just right.

NGOs ideally serve as a check on corporations and the government. Not long ago, most of these institutions viewed themselves that way. Now, intel officials, “researchers,” and executives at firms like Twitter are effectively one team – or Signal group, as it were:

The Woodstock of the Censorship-Industrial Complex came when the Aspen Institute – which receives millions a year from both the State Department and USAID – held a star-studded confab in Aspen in August 2021 to release its final report on “Information Disorder.”

The report was co-authored by Katie Couric and Chris Krebs, the founder of the DHS’s Cybersecurity and Infrastructure Security Agency (CISA). Yoel Roth of Twitter and Nathaniel Gleicher of Facebook were technical advisors. Prince Harry joined Couric as a Commissioner.

Why the fuck is Prince Harry on a committee deciding how free American citizens should be censored?

Their taxpayer-backed conclusions: the state should have total access to data to make searching speech easier, speech offenders should be put in a “holding area,” and government should probably restrict disinformation, “even if it means losing some freedom.”

Snip.

The same agencies (FBI, DHS/CISA, GEC) invite the same “experts” (Thomas Rid, Alex Stamos), funded by the same foundations (Newmark, Omidyar, Knight) trailed by the same reporters (Margaret Sullivan, Molly McKew, Brandy Zadrozny) seemingly to every conference, every panel.

The #TwitterFiles show the principals of this incestuous self-appointed truth squad moving from law enforcement/intelligence to the private sector and back, claiming a special right to do what they say is bad practice for everyone else: be fact-checked only by themselves. While Twitter sometimes pushed back on technical analyses from NGOs about who is and isn’t a “bot,” on subject matter questions like vaccines or elections they instantly defer to sites like Politifact, funded by the same names that fund the NGOs: Koch, Newmark, Knight.

#TwitterFiles repeatedly show media acting as proxy for NGOs, with Twitter bracing for bad headlines if they don’t nix accounts. Here, the Financial Times gives Twitter until end of day to provide a “steer” on whether RFK, Jr. and other vax offenders will be zapped.

Well, you say, so what? Why shouldn’t civil society organizations and reporters work together to boycott “misinformation”? Isn’t that not just an exercise of free speech, but a particularly enlightened form of it?

The difference is, these campaigns are taxpayer-funded. Though the state is supposed to stay out domestic propaganda, the Aspen Institute, Graphika, the Atlantic Council’s DFRLab, New America, and other “anti-disinformation” labs are receiving huge public awards.

Meant to cover this back in February, but FTX founder Sam Bankman-Fried, in additional to all those federal fraud charges, was charged with “12 new counts, including illegally making over 300 political contributions to the tune of tens of millions of dollars through straw donors and using corporate funds.” The overwhelming majority went to Democrats and left-leaning causes. “Bankman-Fried was the second largest individual donor during the 2022 US midterm elections, contributing $39 million to various Democrat causes.” Also: “FTX’s former CEO wanted to give at least $1 million to a pro-LGBTQ political action group, but couldn’t find anyone bisexual or gay at the company whom he trusted, the document said.”

Speaking of Bankman-Fried: “The previously sealed names of two people who co-signed Sam Bankman-Fried’s $250 million bail package have been publicly released. The guarantors were identified in the unredacted bonds as Andreas Paepcke, a Stanford research scientist, and Larry Kramer, former dean of Stanford law school…How the fuck did these Stanford faculty members get so rich as to guarantee that size of a bail?”

Speaking of crypto, Silvergate, a California bank that was a heavy player in the crypto space, is shutting down and liquidating after huge bank runs in the crypto-winter. Want to guess who was a big booster of Silvergate? Would you believe Sam Bankman-Fried?

When China began to require Western corporations to establish Chinese Communist Party (CCP) cells, businesses brushed off the move as benign. For example, when HSBC HBA 0.0% became the first international financial institution at which workers established a Chinese Communist Party cell in its investment banking venture in China in July, the bank stated that the CCP committee does not influence the direction of the firm and has no formal role in its day-to-day activities. But the CCP may have begun to flex its muscle in other ways. This week, the CCP cell inside the Beijing office of Big Four accounting firm EY demanded that party members wear CCP badges at work in the run-up to China’s annual parliamentary meetings.

Silicon Valley Bank, Santa Clara, California, was closed today by the California Department of Financial Protection and Innovation, which appointed the Federal Deposit Insurance Corporation (FDIC) as receiver. To protect insured depositors, the FDIC created the Deposit Insurance National Bank of Santa Clara (DINB). At the time of closing, the FDIC as receiver immediately transferred to the DINB all insured deposits of Silicon Valley Bank.

All insured depositors will have full access to their insured deposits no later than Monday morning, March 13, 2023. The FDIC will pay uninsured depositors an advance dividend within the next week. Uninsured depositors will receive a receivership certificate for the remaining amount of their uninsured funds. As the FDIC sells the assets of Silicon Valley Bank, future dividend payments may be made to uninsured depositors.

Silicon Valley Bank had 17 branches in California and Massachusetts. The main office and all branches of Silicon Valley Bank will reopen on Monday, March 13, 2023. The DINB will maintain Silicon Valley Bank’s normal business hours. Banking activities will resume no later than Monday, March 13, including on-line banking and other services. Silicon Valley Bank’s official checks will continue to clear. Under the Federal Deposit Insurance Act, the FDIC may create a DINB to ensure that customers have continued access to their insured funds.

As of December 31, 2022, Silicon Valley Bank had approximately $209.0 billion in total assets and about $175.4 billion in total deposits. At the time of closing, the amount of deposits in excess of the insurance limits was undetermined. The amount of uninsured deposits will be determined once the FDIC obtains additional information from the bank and customers.

SVB was a bank that primarily counted venture capital firms and technology startups as clients. It achieved financial stardom during the COVID-19 pandemic because major cash deposits from the booming firms increased its deposits from $60 billion in the first quarter of 2020 to over $200 billion in December 2022, the Wall Street Journal reported. Its securities portfolio rose from roughly $27 billion in 2020’s first quarter to approximately $127 billion at the end of 2021.

The fact that most of SVB’s assets were seemingly secure — they were mainly longer-term government bonds — led many investors to feel the bank was secure. Those feelings would be dashed in just two days. The bank suddenly announced Wednesday that it needed to raise over $2.2 billion, sending its stock plunging by more than 60% in a matter of days.

The government securities bought by SVB pay a fixed rate, so when market interest rates were raised, a gap began to grow between how much the securities were worth on the open market and what they were valued on the bank’s books. The unrealized losses in SVB’s securities portfolio in December had grown to more than $17 billion, a number expected to grow, as the securities could only be sold at a loss.

Crack the whip: unacceptable because of origins in slavery

Waiter or waitress: server should be used instead

Biological gender, biological sex, biological woman, biological female, biological man, or biological male

Illegal immigrant or illegal alien

Cake walk: “originated during slavery” and thus perpetuates “racist motifs”

In reference to illegal migration: onslaught, tidal wave, flood, inundation, surge, invasion, army, march, sneak and stealth

Anchor baby

Chain migration: this is a term used by “immigration hard-liners”

Peanut gallery: “the cheapest seats often occupied by Black people and people with low incomes”

Third-world countries: too “derogatory”

Oh, it does not end there. Politico reporters are also not allowed to say that a transgender person “identifies as” a certain gender, or describe the current situation at the border as a “crisis.” The guide also warned reporters to make sure not to portray migrants as a “negative, harmful influence.”

Want some more? “Pro-choice” is frowned upon in favor of “abortion rights supporter,” and (of course) “pro-life” is outlawed, with “anti-abortion” taking its place. “Late-term abortion” is also a no-no; reporters are told to use “abortion later in pregnancy.”

College student accused of stealing more than half a million dollars via credit card fraud working part-time at a mall jewelry store where most of the items are under $50. She marked up items, then returned them at the original price and somehow pocketed the difference. She made eight fake transactions totally more than $540,000. As though somehow the store wasn’t going to notice something funny going on.