It’s hard to know just what the state of the Chinese economy is, given the CCP’s constant lies, but this Joe Blogs video suggests that Chinese manufacturers are in a world of hurt, with four straight years of deflation and falling profit margins.

“Chinese businesses are continuing to suffer from margin erosion. And this is an absolute disaster from China’s perspective, because Chinese businesses have very thin margins in the first place. And if these margins are now being cut, then many businesses in China have now actually fallen into a loss-making situation.”

“More than 50% of the companies in China are now estimated to be banking losses.”

“If you’re posting losses, you don’t pay any taxes, and that will drag down GDP growth in China. The Chinese authorities have said that they’re going to hit 5% again in 2026, but I think there is a major question mark over whether or not that is realistically achievable.” My working assumption is they just lied about hitting that target last year as well. And probably meany years before that.

“If we have a look at this table, it shows what’s been happening with producer prices over the past 12 months. And the scale on the right hand side here starts at zero and goes down to minus 4%. And as you can see, in every single one of the past 12 months, Chinese producers have been cutting their prices. This chart is also referred to as the factory gate prices. So this is the price of products when they’re leaving Chinese factories. And the latest data for January 2026 shows that year on year prices were down by 1.4%.”

“If you put that into the context of your economy, if prices were going down by 1.4%, then you’d be very happy as a consumer, because that means that you’re paying less at the tills.”

“But as a company, this is an absolute disaster. Because the reason why we want some form of inflation in the economy is because it allows companies to pass on their cost increases.”

“But if your end price is going down by 1.4%, then clearly you can’t pass on those cost increases. You have to absorb them. And this is why Chinese businesses are seeing their profit margins being wiped out.”

“And if we widen the scale of this chart to show the last five years, you can start to see the scale of the problem in China, because producer prices, factory gate prices have now been falling since May 2022.”

“What we’ve got here is a compounding of year-on-year falls in factory gate prices.”

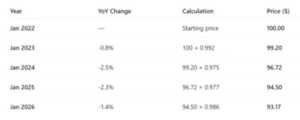

“We have a look at this table I’ve put together. It shows what the impact of this has been on the sales price for a product. So if we assume that January 2022, which was the last time that we saw a price increase year-on-year in China, if we assume that a product that Chinese company was selling for $100 at that time, this shows what the impact has been on that product. So in the year to January 2023, prices fell by 8% producer prices. So that means that that $100 product would have then been selling for $99.20. In January 2024, the year-on-year fall was 2.5%. So that $100 product would then be have sold would have been been selling for $96.72. In 2025 there was a 2.3% fall in producer prices. So that product by then would have been down to $94.50. And the 1.4% that we’ve just seen posted means that that $100 product that was being sold in 2022 would now be selling for $93.17.”

Is this deflation mirrored in Chinese consumer inflation prices? No. “It has been a bit of a mixed story. The scale on the right hand side here goes from 1% positive at the top to 1% negative at the bottom. And as you can see, in six out of the past 12 months, prices did actually fall, but they’ve been increasing over the past four months. And you can see that the latest data that we have for January 2026 shows that year on year prices are up by .2%. So that doesn’t explain the 1.4% fall in producer prices in January 2026.”

“And we widen the scale of this chart to show the past five years. You can see that whilst there has been a few months where we’ve seen deflation, it’s predominantly been inflation in China. It’s a relatively low level compared to other countries, we’re talking between 1% and 2%. So a lot less than we’ve seen in the West over the past five years. But we’ve still seen prices going up.”

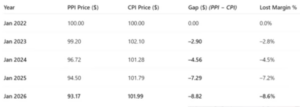

“And if we have a look at this table, it shows what’s happened to prices over the same period. So if we assume the same $100 product in January 2022 that we just looked at for producer prices, in 2023 prices actually went up by 2.1%. So that product would have been selling for $102.10 at that time. We saw deflation in January 2024, which would have brought the price back down to $101.28. In 2025, we saw a year-on-year increase of .5%. So it would have pushed that that price to $101.79. And the most recent data for January 26 of 2% increase tells us that that product would now be selling for $101.99. So an increase in the price.”

“And if we have a look at the comparison between those two tables, then you can see here the producer prices between January 22 and 26, the $100 product has gone from $100 to $93.17. That’s what the companies are receiving for that same product. At the same time, inflation has gone up by 1.99% over that period. That pushed up the price to 101.99. So the gap between those two metrics, what’s been happening with inflation? If producer prices had just been moving at the same rate as inflation, the difference between the two is $8.82 over the past five years. That represents lost profit margin for Chinese businesses over the past five years of 8.6%. So that’s how much profit has been taken out by the fall in producer prices compared to what should have been happening if they were matching inflation.”

“Now why is this happening?”

“Why are Chinese businesses constantly cutting their prices when prices in the domestic market are going up? Well, there’s a number of reasons for it, but one of the main reasons is down to overcapacity.”

“Chinese industry has been gearing up heavily over the past 20 years. So in areas where China believes that it’s strong, it’s put a lot of investment and the government has subsidized a lot of these companies in many situations to enable them to grow rapidly to take a dominant global market position. So we have got some huge businesses in sectors where China has tried to become dominant.”

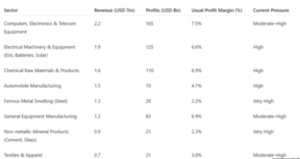

“If we have a look at this table, it shows the different industries in China that are the biggest in terms of revenue and what that should mean in terms of profitability for those businesses.”

“So the biggest sector in terms of manufacturing is computers, electronics, and telecom equipment. So I’m sure you’ve seen lots of different equipment that’s been made in China over the past 20 years. It’s estimated that that sector has revenue of around about $2.2 trillion US, and that should be equating to around about $165 billion of profits. The usual profit margin is around 7.5% for Chinese businesses in those sectors. But those sectors are currently under a lot of pressure.”

“Firstly, we’ve seen its biggest single market, the USA, applying tariffs against Chinese imports. So, that’s causing problems because it’s pushing up the price. And in order to counteract those tariff increases, some Chinese businesses have actually been cutting their cost to absorb some of those tariffs. But also, we’re seeing competition from the rest of the world.”

“So Chinese businesses are constantly slashing their prices to be the cheapest on the shelf because, realistically, that’s why a lot of consumers choose the Chinese option.”

“So that sector is under pressure at the moment. So that’s one of the reasons why those companies are cutting back on their prices.”

“Now another area which is absolutely huge for Chinese businesses is electric vehicles, batteries and solar. So this is an area that China has really specialized in. It’s cornered the market in batteries and solar panels. Most of them are made in China these days. But also electric vehicles. It decided to take a big slice of the global market and those electric vehicles are being sold at very low prices compared to local competition. So if you compare a Chinese electric vehicle the actual list price of that versus things like BMW, Volkswagen, Ford, they are a lot cheaper.”

“That’s one of the reasons why a lot of countries have been applying tariffs on the electric vehicles. So this is aside from Donald Trump’s tariffs. We’re talking about the whole industry globally is saying that it’s not fair that EVs are being subsidized. In terms of revenue, it’s around about $1.9 trillion for China and the usual profit margins around about 7% on that. But they’re under a lot of pressure because of the tariffs. Now a lot of countries are saying that China is trying to put the rest of the world out of business so that it can become completely monopolistic in these areas. So they’re under high pressure, and that’s another reason why Chinese companies are cutting their prices.”

“Jump down to some of the things that are related to property. Look at ferrous metals, which are basically steel. China has some of the biggest steel smelting plants in the world. It’s a big producer of steel. The revenue is about $1.3 trillion. Now the profit margin on steel is wafer thin. 2.2%. And the problem that China has is twofold at the moment.”

“Firstly, a lot of that steel was being sold into the Chinese market for the property market, because the property market over the past 25 years was booming the first 20 years of the 20th century. It was absolutely on fire. Lots of massive property developers like Evergrande were building whole cities all across China and they were using a huge amount of steel to do that. They building these huge tower blocks and you have to put a lot of steel in there.”

“The properties sector has absolutely crashed in China over the past few years, since the government changed the rules and made it more difficult for property developers to borrow money. There hasn’t been anywhere near as much production. So that’s caused a huge drop off in demand in China for steel itself.”

“So that’s meant that Chinese steel businesses have had to look to the export markets. But similar to what’s been happening in the electric vehicle market, a lot of countries, including the USA, have pushed back on Chinese steel imports because they are so cheap that they are killing local steel production. And in the UK, the British government had to recently take over the last virgin steel producer in the UK to make sure that it could actually produce steel that was needed for things like the defense sector. So we’ve seen a major attack globally on the whole steel industry, and lots of countries have pushed back on that.”

“So the steel industry in China is now under a lot of pressure. It’s struggling with regards to demand and those profit margins have been wiped out.”

“But we’ve got a lot of different sectors here that are under intense pressure at the moment from competition. And that’s one of the factors why Chinese businesses are cutting their prices.”

“In addition to that, Chinese businesses are also seeing weak demand at home. Chinese consumers are not buying as much stuff as they used to. So Chinese companies are cutting their prices to try to encourage consumers to keep buying.”

“And as that demand falls at home, what that means is that Chinese businesses are having to depend on the export markets more. So, Chinese companies are struggling with regards to its biggest single market, because the USA has hit all Chinese imports with additional tariffs. So, that’s led to a further cutting of prices and Chinese businesses basically across the board are geared up for high volume, low margin. And when demand starts to fall, then the only thing that you can do is cut your price.”

“Because if you’ve got a huge fixed cost business, if you’ve spent billions building up your business, maybe it’s lots of machinery, you’ve got lots of people, you’ve got huge factories, you need to hit those volume numbers just to keep the wafer thin profit margins going.”

“If demand starts falling, you can’t cut back on your costs because these are very high fixed cost businesses. So what Chinese businesses are doing instead is slashing their prices to maintain their volume of sales. But that is wiping out their profit margins. And that’s why many Chinese businesses, over 50%, are now banking losses.”

“And of course, this is an absolute disaster from the Chinese economy point of view, because it needs those companies to keep contributing to make profits to pay taxes to contribute to GDP in order to hit that 5% GDP total.”

“What we’re seeing from the data that’s just been published is that producer prices are continuing to fall.”

“Inflation is still very, very low in China. Consumer demand is very weak. So China remains dependent on the export markets. Many export markets are pushing back against Chinese imports.”

“Chinese businesses are having to cut their prices, which is further reducing their profit margins. Many have moved into losses, and this is a complete nightmare, vicious circle from many of these companies’ perspective. And I can’t see how they’re going to get out of this situation.”

China’s economy has long been smoke and mirrors all the way down. To be sure, China has made real gains, joining (and gaming) the world economic system just in time to see explosive growth thanks to global trade deals, the container ship era, rampant IP theft, and western capitalists eager to exploit cheap labor. But the rest of the world slowly caught on to China’s tricks, especially since China thought they could get away with belligerent, militarist, expansionist rule-breaking aggression against at the same time it was striving to become the world’s manufacturing hub.

Now that the world’s caught on, people are starting to realize that much of China’s “economic miracle” was an illusion. The opaque banking rules, the government subsidies, the insane “ghost cities” property boom and the regime’s strict currency controls all helped to hide the manipulations, making China’s economy look healthier than it actually is. But now the entire house of cards is tumbling down, and China has no one to blame but itself.

Interesting article. However, first of all I don’t believe any statistics that the Chinese put out. As far as I can see, they are all made up. Second of all, if I had a dollar for every article/YouTube video I’ve seen about the sure doom of China, I could afford a Business Class ticket to Beijing to see for myself. People like Joe Blogs, Peter Zeihan, and Gordon Chang have made careers out of preaching doom and gloom for China, but they still seem to be here.

But thanks for the article anyway.

I’m amazed that the Chinese think that they can put every other manufacturing out of business and corner the market with no pushback. To be sure, they’ve bought the political classes in most countries but eventually even there the working folks have to push back.

This analysis completely fails to take into account massive swings in USD/CNY and the very advantageous energy prices the Chinese have secured from the Russians.

The Chinese economy is not roaring, but neither is it a basket case.

The Chinese Communists and especially Xi Jinping really are that arrogant. They seriously believe they are entitled to pursue a mercantilist, Machiavellian trade policy with no pushback whatsoever. For that matter, they seriously believe they are entitled to seize other countries’ territory with no pushback whatsoever, which is why pretty much everyone in East Asia (except for North Korea and Cambodia) hates the Chinese Communists.

While it is true that all too many commentators have been predicting China’s demise for all too long, one factor is already baked into the cake: inevitable population collapse due to the persistence of the one-child culture–even after the policy behind it was not only revoked, but reversed. Killing off millions of baby girls back then didn’t help either.

“If you’re posting losses, you don’t pay any taxes, and that will drag down GDP growth in China.“

I don’t like (or understand) this mindset that what matters economically is tax revenue. If these businesses are losing money, doesn’t that drag down GDP regardless of how much is being skimmed off by the government?

“This analysis completely fails to take into account massive swings in USD/CNY and the very advantageous energy prices the Chinese have secured from the Russians.”

To the contrary, a large part of the analysis concerns falling commodity prices and the cost of production inputs.

“If these businesses are losing money, doesn’t that drag down GDP regardless of how much is being skimmed off by the government?”

GDP = C + I + G + NX, where C is consumption, I is investment, G is government spending, and NX is net exports (exports minus imports).

If tax revenue is reduced, “G” spending will be forced to contract. Admittedly, spending can continue through deficit spending, but this will amount to getting a loan through bond sales or simply running the printing press to cover the difference between taxes and spending.

The resultant inflation would boost commodity prices, which would increase production costs, aggravating the “overcapacity” problem.

From the article:“More than 50% of the companies in China are now estimated to be banking losses…..Chinese industry has been gearing up heavily over the past 20 years. So in areas where China believes that it’s strong, it’s put a lot of investment and the GOVERNMENT HAS SUBSIDIZED A LOT OF THESE COMPANIES in many situations to enable them to grow rapidly to take a dominant global market position.”

The subsidized companies subsequently expanded to generate “overcapacity”, which is to say beyond the economy’s ability to adequately utilize. This is most fully realized in the housing market but will be evident in industry, as well.

If the output of these subsidized industries is intended for the export market and the importers must apply a tariff charge to the product, the additional cost must be recognized as a production cost. So even if domestic input costs are falling, a high tariff will more than offset this advantage.

So tariffs make the export industries less profitable, necessitating either additional subsidies or contraction in those same industries will follow

China Inc.then, is exposed as a financial fraud and investors will inevitably head for the exits.Taxes will have to be raised if the charade is to continue but raising taxes during a financial contraction may very well trigger a full-blown depression.

Will this chain of events lead to revolution or war? Stay tuned…

“To the contrary, a large part of the analysis concerns falling commodity prices and the cost of production inputs.”

Steel is the only item mentioned here which even you could consider a commodity. It is not a commodity, rather it is made from commodities dug out of the ground like iron ore, manganese, lime, and coal. Steel is bespoke, manufactured to specifications which vary from country-to-country and industry-to-industry. You will not find any steel grade, nor any other item mentioned here, traded as a commodity on a recognized commodity exchange.

Commodity prices are lower than their pandemic peaks (when producers were strangled by government constrictions), but they are – across the board – higher than any other period in history and still rising. Not falling.

This is not a commodity market. It is a unbased financial derivative (hedge). You cannot take possession of steel through this CME mechanism. Eventual possession is the definition and purpose of a commodity market. Real commodity markets have warehouses which disperse commodities to bidders on demand, such as the LME Warehouse system for nonferrous metals.

Financial settlements at term on this mechanism are unrelated to underlying steel prices, rather they are based on terminal bids. This hedge is Polymarket gambling.

“Eventual possession is the definition and purpose of a commodity market.”

No, the vast majority of futures contracts traded on the CBOT are used to hedge against price risk and are traded against a “strike” price before the underlying commodity is taken for delivery..

“No, the vast majority of futures contracts traded on the CBOT are used to hedge against price risk and are traded against a “strike” price before the underlying commodity is taken for delivery..”

Once again, the purpose of a commodity market is to distribute commodities from producers to consumers.

Commodity producers ship commodities to points of trade, usually warehouses. Commodity consumers take possession at those trade points.

Commodity producers sell contracts which transfer ownership of a certain quantity of a specified grade of commodity. Commodity consumers purchase contracts which obtain ownership of a certain quantity of a specified grade of commodity. A contract purchaser can demand delivery of the specified commodity from the point of trade at any time after the purchase clears.

The delivery and taking of possession at the instant of trade is the essence of a commodity market and provides price discipline. When that point of trade runs out of a commodity (rare, but it happens), the commodity market locks up.

Traders can opt to sell their purchase contracts back to the commodity exchange, but this is just them using the market to hedge. This kind of hedging is permissible in most modern commodity markets because it can be used to establish futures prices, but it is not a fundamental characteristic of a commodities market.

Your CME derivative is a gambling mechanism, not a commodity market. There is no point of trade. A “contract” (actually nothing more than a bidding unit) does not permit the purchaser to take delivery of steel from anyone or anywhere, at any time. There is no price discipline.

“No, it is priced against hot-rolled coil steel, which is an industrial commodity widely used in hydraulic stamping operations.”

“No, it is a risk management tool, used as insurance against unfavorable price changes of the underlying commodity.”

Roger Smith of GM broke the steel industry price list in 1982, along with many of its terms. Since April 1982, there has not been any recognized industry price for hot rolled steel. Indeed, it is common for HR prices to be simultaneously rising and falling for different mills and consumers.

“hydraulic stamping operations” is not a proper description of anything done in industry. Some really large plan area stampings are pressed on open frame hydraulic presses, but these operations are extremely uncommon. Mechanical stamping presses are the norm due to their energy efficiency and speed. Hydraulic presses are normally reserved for long draw forging operations, such as artillery shell extrusioning, or forging difficult to form alloys such as titanium (where low strain rates are required to prevent cracking).

Steel price risk management is performed exclusively with multi year contracts. Three year contracts between mills and consumers are now the norm, and 5 year contracts are popular with the Japanese. In the auto industry, small parts stampers are invariably covered in their customers’ steel contracts. This provides them with “risk management”.

“Since April 1982, there has not been any recognized industry price for hot rolled steel. Indeed, it is common for HR prices to be simultaneously rising and falling for different mills and consumers.”

This is why there is a futures contract for this commodity: it brings predictability to the price discovery process.

Interesting article. However, first of all I don’t believe any statistics that the Chinese put out. As far as I can see, they are all made up. Second of all, if I had a dollar for every article/YouTube video I’ve seen about the sure doom of China, I could afford a Business Class ticket to Beijing to see for myself. People like Joe Blogs, Peter Zeihan, and Gordon Chang have made careers out of preaching doom and gloom for China, but they still seem to be here.

But thanks for the article anyway.

I’m amazed that the Chinese think that they can put every other manufacturing out of business and corner the market with no pushback. To be sure, they’ve bought the political classes in most countries but eventually even there the working folks have to push back.

This analysis completely fails to take into account massive swings in USD/CNY and the very advantageous energy prices the Chinese have secured from the Russians.

The Chinese economy is not roaring, but neither is it a basket case.

PBAR,

The Chinese Communists and especially Xi Jinping really are that arrogant. They seriously believe they are entitled to pursue a mercantilist, Machiavellian trade policy with no pushback whatsoever. For that matter, they seriously believe they are entitled to seize other countries’ territory with no pushback whatsoever, which is why pretty much everyone in East Asia (except for North Korea and Cambodia) hates the Chinese Communists.

While it is true that all too many commentators have been predicting China’s demise for all too long, one factor is already baked into the cake: inevitable population collapse due to the persistence of the one-child culture–even after the policy behind it was not only revoked, but reversed. Killing off millions of baby girls back then didn’t help either.

“If you’re posting losses, you don’t pay any taxes, and that will drag down GDP growth in China.“

I don’t like (or understand) this mindset that what matters economically is tax revenue. If these businesses are losing money, doesn’t that drag down GDP regardless of how much is being skimmed off by the government?

I do not understand. Eight percent of $100 is $8.00, not $0.80. What am I missing?

“This analysis completely fails to take into account massive swings in USD/CNY and the very advantageous energy prices the Chinese have secured from the Russians.”

To the contrary, a large part of the analysis concerns falling commodity prices and the cost of production inputs.

“If these businesses are losing money, doesn’t that drag down GDP regardless of how much is being skimmed off by the government?”

GDP = C + I + G + NX, where C is consumption, I is investment, G is government spending, and NX is net exports (exports minus imports).

If tax revenue is reduced, “G” spending will be forced to contract. Admittedly, spending can continue through deficit spending, but this will amount to getting a loan through bond sales or simply running the printing press to cover the difference between taxes and spending.

The resultant inflation would boost commodity prices, which would increase production costs, aggravating the “overcapacity” problem.

China is in a bad place right now.

From the article:“More than 50% of the companies in China are now estimated to be banking losses…..Chinese industry has been gearing up heavily over the past 20 years. So in areas where China believes that it’s strong, it’s put a lot of investment and the GOVERNMENT HAS SUBSIDIZED A LOT OF THESE COMPANIES in many situations to enable them to grow rapidly to take a dominant global market position.”

The subsidized companies subsequently expanded to generate “overcapacity”, which is to say beyond the economy’s ability to adequately utilize. This is most fully realized in the housing market but will be evident in industry, as well.

If the output of these subsidized industries is intended for the export market and the importers must apply a tariff charge to the product, the additional cost must be recognized as a production cost. So even if domestic input costs are falling, a high tariff will more than offset this advantage.

So tariffs make the export industries less profitable, necessitating either additional subsidies or contraction in those same industries will follow

China Inc.then, is exposed as a financial fraud and investors will inevitably head for the exits.Taxes will have to be raised if the charade is to continue but raising taxes during a financial contraction may very well trigger a full-blown depression.

Will this chain of events lead to revolution or war? Stay tuned…

Eight percent is the annualized rate, but the period covered is only one month.

“To the contrary, a large part of the analysis concerns falling commodity prices and the cost of production inputs.”

Steel is the only item mentioned here which even you could consider a commodity. It is not a commodity, rather it is made from commodities dug out of the ground like iron ore, manganese, lime, and coal. Steel is bespoke, manufactured to specifications which vary from country-to-country and industry-to-industry. You will not find any steel grade, nor any other item mentioned here, traded as a commodity on a recognized commodity exchange.

Commodity prices are lower than their pandemic peaks (when producers were strangled by government constrictions), but they are – across the board – higher than any other period in history and still rising. Not falling.

“You will not find any steel grade, nor any other item mentioned here, traded as a commodity on a recognized commodity exchange.

Wrong again. Steel is a commodity that trades in the futures market.

https://www.marketwatch.com/investing/future/hrn00

“[T]hey are – across the board – higher than any other period in history and still rising. Not falling.”

The Chinese Producer Price Index (YOY) as of January 2026 is in negative territory, as it was all year. https://en.macromicro.me/collections/24/cn-price-relative/12049/cn-ppi

The index measures *ahem* commodity prices of the goods coming to the factory gates.

“Wrong again. Steel is a commodity that trades in the futures market.

https://www.marketwatch.com/investing/future/hrn00”

This is not a commodity market. It is a unbased financial derivative (hedge). You cannot take possession of steel through this CME mechanism. Eventual possession is the definition and purpose of a commodity market. Real commodity markets have warehouses which disperse commodities to bidders on demand, such as the LME Warehouse system for nonferrous metals.

Financial settlements at term on this mechanism are unrelated to underlying steel prices, rather they are based on terminal bids. This hedge is Polymarket gambling.

“The index measures *ahem* commodity prices of the goods coming to the factory gates.”

Producer Price Indices are a measure of the selling prices received by producers for their output. Not commodity prices, which are a producer input,

“Eventual possession is the definition and purpose of a commodity market.”

No, the vast majority of futures contracts traded on the CBOT are used to hedge against price risk and are traded against a “strike” price before the underlying commodity is taken for delivery..

“It is a unbased financial derivative.”

No, it is priced against hot-rolled coil steel, which is an industrial commodity widely used in hydraulic stamping operations.

“This hedge is Polymarket gambling.”

No, it is a risk management tool, used as insurance against unfavorable price changes of the underlying commodity.

“No, the vast majority of futures contracts traded on the CBOT are used to hedge against price risk and are traded against a “strike” price before the underlying commodity is taken for delivery..”

Once again, the purpose of a commodity market is to distribute commodities from producers to consumers.

Commodity producers ship commodities to points of trade, usually warehouses. Commodity consumers take possession at those trade points.

Commodity producers sell contracts which transfer ownership of a certain quantity of a specified grade of commodity. Commodity consumers purchase contracts which obtain ownership of a certain quantity of a specified grade of commodity. A contract purchaser can demand delivery of the specified commodity from the point of trade at any time after the purchase clears.

The delivery and taking of possession at the instant of trade is the essence of a commodity market and provides price discipline. When that point of trade runs out of a commodity (rare, but it happens), the commodity market locks up.

Traders can opt to sell their purchase contracts back to the commodity exchange, but this is just them using the market to hedge. This kind of hedging is permissible in most modern commodity markets because it can be used to establish futures prices, but it is not a fundamental characteristic of a commodities market.

Your CME derivative is a gambling mechanism, not a commodity market. There is no point of trade. A “contract” (actually nothing more than a bidding unit) does not permit the purchaser to take delivery of steel from anyone or anywhere, at any time. There is no price discipline.

“No, it is priced against hot-rolled coil steel, which is an industrial commodity widely used in hydraulic stamping operations.”

“No, it is a risk management tool, used as insurance against unfavorable price changes of the underlying commodity.”

Roger Smith of GM broke the steel industry price list in 1982, along with many of its terms. Since April 1982, there has not been any recognized industry price for hot rolled steel. Indeed, it is common for HR prices to be simultaneously rising and falling for different mills and consumers.

“hydraulic stamping operations” is not a proper description of anything done in industry. Some really large plan area stampings are pressed on open frame hydraulic presses, but these operations are extremely uncommon. Mechanical stamping presses are the norm due to their energy efficiency and speed. Hydraulic presses are normally reserved for long draw forging operations, such as artillery shell extrusioning, or forging difficult to form alloys such as titanium (where low strain rates are required to prevent cracking).

Steel price risk management is performed exclusively with multi year contracts. Three year contracts between mills and consumers are now the norm, and 5 year contracts are popular with the Japanese. In the auto industry, small parts stampers are invariably covered in their customers’ steel contracts. This provides them with “risk management”.

“Since April 1982, there has not been any recognized industry price for hot rolled steel. Indeed, it is common for HR prices to be simultaneously rising and falling for different mills and consumers.”

This is why there is a futures contract for this commodity: it brings predictability to the price discovery process.

“This is why there is a futures contract for this commodity: it brings predictability to the price discovery process.”

There is no “price discovery” process in hot rolled sheet steel. Far too many variables. Why steel is not a commodity.