The Senate’s bad border deal goes down badly, Big Brother is (still) watching you, Netanyahu tells everyone calling for a Gaza ceasefire to stick it in their murder tunnels, more Democrats arrested for (or convicted of) fraud, and a tiny bit of Disney news. It’s the Friday LinkSwarm!

Republicans took one look at the abomination of a “bipartisan” border deal and declared it dead on arrival.

In a key vote on Wednesday, Senate Republicans moved to block the long-anticipated bipartisan border deal, which ties border-security provisions to aid for both Israel and Ukraine.

The bill was blocked in a 49 to 50 procedural vote, with only four Republicans joining Democrats in backing the legislation. The bill needed 60 votes to advance.

This setback comes after months of negotiations between Senate Republicans and Democrats on a measure President Joe Biden strongly requested. While the GOP wants more resources allocated toward the southern border, House Republicans and former president Donald Trump have made it clear they don’t want the legislation tied to foreign aid.

Hours after the bill’s details were revealed Sunday night, House GOP leaders rejected the package and declared it “DEAD on arrival in the House.”

Trump, who has made the border crisis a central issue of his 2024 presidential campaign, also weighed in on the border deal earlier this week. “Don’t be STUPID!!! We need a separate Border and Immigration Bill. It should not be tied to foreign aid in any way, shape, or form!” Trump posted on Truth Social.

Before the Senate voted on the matter, Biden blamed Trump for Republicans’ fierce opposition to the bill.

“Now, all indications are this bill won’t even move forward to the Senate floor,” Biden said Tuesday. “Why? A simple reason: Donald Trump.”

Hey Biden, I’m already going to vote for Trump. You don’t need to keep giving me new reasons.

The $118 billion Senate proposal includes about $60 billion in Ukraine funding, $14 billion in Israel aid, and $20 billion in border-security improvements, among various other items listed in the legislative package.

Senators James Lankford of Oklahoma, Lisa Murkowski of Alaska, Susan Collins of Maine, and Mitt Romney of Utah were the only Republicans to vote in favor of the bill on Wednesday.

Lankford should be ashamed to be in such company.

Texas isn’t taking the Biden Administrations abrogation of the rule of law lying down. “Texas Attorney General’s Legal Challenge to Biden Administration’s ‘Asylum Rule’ Will Proceed. A federal judge ruled Texas raised a plausible claim that the federal government is violating the Appointments Clause of the U.S. Constitution.”

The Texas Office of the Attorney General (OAG) announced a procedural victory in one of its many ongoing lawsuits against the federal government this week, after a federal district judge ruled against a motion by the Department of Homeland Security (DHS) to dismiss a legal challenge to its “asylum rule,” saying Texas had a plausible constitutional challenge.

According to the OAG, the federal government violated the Appointments Clause in the U.S. Constitution when the DHS granted power to review asylum cases to immigration officers — a power uniquely held under federal statute by immigration judges.

“This case offers a rare opportunity to litigate the application of the Appointments Clause of the Constitution, which states that Congress may only vest the power to appoint “inferior Officers… in the President alone, the Courts of Law, or the Heads of Departments,” the OAG wrote in a press statement regarding the case.

The office explained that by using asylum officers to perform jobs Congress assigned to judges when said officers were not appointed in the same manner, DHS violated the Constitution.

The OAG also argues that asylum officers are granting more noncitizens asylum than otherwise would be entitled to it. This is causing surges at the border and population increases that are in turn increasing the state’s costs relating to the increases, the state says.

“It is tremendously important for Texas and for our Constitutional order that this case is allowed to move forward,” Attorney General Ken Paxton said regarding the case. “The Biden Administration must not be permitted to ignore Congress and violate the Constitution. We take every opportunity to hold Biden accountable for his unlawful overreach.”

Rank-and-file Border Patrol agents have slammed the Senate’s $118B Senate funding bill that would guarantee 1.5 million illegal migrants entry to the United States, while sending the majority of funds to Ukraine ($60B+) and Israel ($14.1B).

Snip.

“Now that I’ve seen more of it, they can respectfully go fuck themselves. The more I’m seeing the more it just puts what they’ve been doing in writing. You want to shut this down, it’s real easy. Team up [the Department of Defense] with DHS and let us enforce like we were supposed to,” one agent told the Caller, adding “I feel like we are the only nation in the world that is this dumb about the border. Maybe it’s because we haven’t.”

Oh, and “Aliens from noncontiguous countries shall not be included in the sum of aliens encountered.” Did America’s enemies write this thing?

Cruz went on to say he knew [the Biden border bill] “had zero chance of passage” and that the entire purpose of the bill was to give “political camouflage to Democrats running in November.”

“Joe Biden can secure the border any day he wants,” Cruz said. “He doesn’t want to.”

The Secure the Border Act, which passed in the lower chamber as as House Resolution (H.R.) 2, was introduced to the Senate by Cruz in September of 2023, a fact he highlighted Wednesday, saying to “give me Ukraine aid and H.R. 2 and I’ll vote for that.”

H.R. 2 would have continued construction of the border wall, reinstated the “remain in Mexico” policy, and added border patrol agents and technology for both the southern and northern borders.

“Democrats do not want to secure the border; they want this invasion,” Cruz continued. “The Americans who are dying as a result, they’re [Democrats] willing to look the other way.”

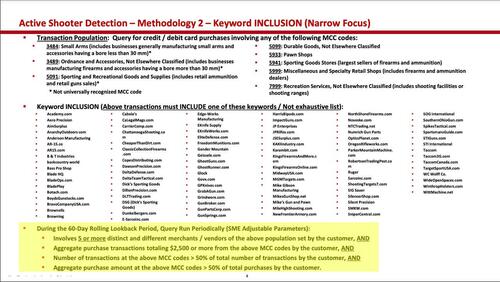

A few weeks ago, Ohio congressman and Judiciary Committee chairman Jim Jordan’s office released a letter to Noah Bishoff, the former director of the Financial Crimes Enforcement Network, or FinCEN, an arm of the Treasury Department. Jordan’s team was asking Bishoff for answers about why FinCEN had “distributed slides, prepared by a financial institution,” detailing how other private companies might use MCC transaction codes to “detect customers whose transactions may reflect ‘potential active shooters.’”

The slide suggested the “financial company” was sorting for terms like “Trump” and “MAGA,” and watching for purchases of small arms and sporting goods, or purchases in places like pawn shops or Cabela’s, to identify financial threats.

Jordan’s letter to Bishoff went on:

According to this analysis, FinCEN warned financial institutions of “extremism” indicators that include “transportation charges, such as bus tickets, rental cars, or plane tickets, for travel to areas with no apparent purpose,” or “the purchase of books (including religious texts) and subscriptions to other media containing extremist views.”

During the Twitter Files, we searched for snapshots of the company’s denylist algorithms, i.e. whatever rules the platform was using to deamplify or remove users. We knew they had them, because they were alluded to often in documents (a report on the denylist is_Russian, which included Jill Stein and Julian Assange, was one example).

However, we never found anything like the snapshot Jordan’s team just published:

The highlighted portion shows how algorithmic analysis works in financial surveillance.

First compile a list of naughty behaviors, in the form of MCC codes for guns, sporting goods, and pawn shops.

Then, create rules: $2,500 worth of transactions in the forbidden codes, or a number showing that more than 50% of the customer’s transactions are the wrong kind, might trigger a response.

The Committee wasn’t able to specify what the responses were in this instance, but from previous experience covering anti-money-laundering (AML) techniques at banks like HSBC, a good guess would be generation of something like Suspcious Activity Reports, which can lead to a customer being debanked.

If Facebook, Twitter, and Google have already shown a tendency toward wide-scale monitoring of speech and the use of subtle levers to apply pressure on attitudes, financial companies can use records of transactions to penetrate individual behaviors far more deeply. Especially if enhanced by AI, a financial history can give almost any institution an immediate, unpleasantly accurate outline of anyone’s life, habits, and secrets. Worse, they can couple that picture with a powerful disciplinary lever, in the form of the threat of closed accounts or reduced access to payment services or credit. Jordan’s slide is a picture of the birth of the political credit score.

Tiabbi says worse revelations are to come…

“Netanyahu Rejects Hamas Cease-Fire Demands, Vows to Fight until ‘Absolute Victory.'”

Israeli prime minister Benjamin Netanyahu rejected Hamas cease-fire demands on Wednesday, vowing to fight on until “absolute victory.”

Netanyahu made the comments shortly after meeting with Secretary of State Antony Blinken, who arrived in the region Tuesday night after meeting with leaders of Qatar and Egypt in the most serious diplomatic push of the war to secure a cease-fire agreement. Through these diplomatic channels, Hamas presented Israel with a proposal for a three-stage cease-fire that would last for 135 days and culminate in the end of the war.

“Surrendering to Hamas’s delusional demands that we heard now not only won’t lead to freeing the captives, it will just invite another massacre.”

Indeed.

The Special Counsel’s report on Biden’s mishandling paints a picture of Biden’s mental decline we all know is true but which the media refuses to report.

President Biden couldn’t even remember when he was vice president or when his son Beau had died, leading special counsel Robert Hur to conclude that he could not bring charges for mishandling of classified documents, because a jury would see the president “as a sympathetic, well-meaning, elderly man with a poor memory.”

In a report, Robert Hur concluded that Biden “willfully retained and disclosed classified materials after his vice presidency when he was a private citizen.” But he declined to issue any charges, in part because Biden’s poor recollection would make him hard to convict.

If you want to see Fani Willis taken down only the way Ace of Spades can, then I direct your attention to “CashApp Cougar Fani Willis: Okay, Fine, So I Used Taxpayer Money to Hire a Human Meat-Mallet to Pound My Snizz Into Thin Tender Strips Like Veal Scallopini.” (Hat tip: Reader Tig if Brue.)

Members of the Austin American-Statesman took one look at the vast wave of layoffs hitting newsrooms across the country and decided “Now is the perfect time to go on strike!” (Note: Elon Musk should buy the name, fire everyone, and build a national quality newspaper from scratch.)

Dell demands all workers (no matter how far away) return to the office. Those who don’t will be “placed on a ‘career limiting’ fully remote contract. In my experience, working for Dell is itself career limiting…

Budget drag race community comes together to help fan with terminal brain tumor who’s also the happiest guy they know. “Don’t feel bad for me. Everyone’s terminal.”

Louis Rossmann has ample reason rant today, namely news of a failed software update that bricks your car.

Note: This happened on the Ford Mach-E Mustang, the ugly crossover SUV that shouldn’t be called a Mustang.

“Unfortunately a recent software update was not successful your vehicle cannot be driven. Please call customer support.”

“I’m confident that when you call that number, you’re going to be dealing with is somebody who helps talk you through how to restore your car’s operating system from backup memory. Because of course, if you’re dealing with mission critical firmware or something, surely you would have a copy of the original that came with it?”

“Or perhaps a copy of the last known good update that was actually working over there that you could go back to if the update was not successful?”

“Of course not! You paid $63,000 for a device that is literally more buggy than Windows 10.”

“This car is over $60,000 and they don’t have even the most basic, fundamental redundancy built in, so that if your update fails it will flash back to a known good [version] on the backup memory. Apparently that’s not a thing.”

Says that this problem isn’t because the Mach E is an EV vehicle.

“I do not believe there is a circumstance where the vehicle is so screwed up because the version of software that it had from February of 2023 was so behind that that vehicle is now fundamentally unfit to be on a road, even in limp mode. That’s ridiculous.”

“The ability to roll back a version of software to an older version if the update that you put on is an update that screwed it up this is something that has been more than perfected in the modern day.”

“To not implement it into a vehicle that costs over $60,000 to the point where the entire 4,000 lb hunk of metal needs to be towed, and you no longer have a method of transportation because of that? There’s no excuse for it.”

“One of the things that bothers me a lot is that every time you move to a new technology paradigm, we accept less freedom. We accept that things are going to suck more in ways that they don’t have to suck.”

“You see this subscription bullshit, this less reliability bullshit, this everything made to break bullshit, this everything made to be replaced in a year or two, this every…this is not something that is simply inherent to electric vehicles this is something that is pervasive. This is something that is happening everywhere.”

“This is something that we need to push back against every single time we see this happen.”

Right-to-repair advocate, former New Yorker and current Texan Louis Rossmann did a video (and then a follow up) on a man whose Amazon smart home devices were all locked out of functioning after an Amazon delivery driver falsely accused him of having a “racist doorbell.” (The followup video covers his access being restored.) Rossmann noted that this was a good reason to never have “smart” devices in your home that third parties (like Amazon) can turn off at will.

Well, guess what? Amazon just disabled Rossmann’s 7+ year affiliate account over bogus reasons.

This is a crappy and petty move, Amazon, and only underscores why no one should entrust you with control over their “smart” devices.

Our 2-year investigation has concluded that Block has systematically taken advantage of the demographics it claims to be helping. The “magic” behind Block’s business has not been disruptive innovation, but rather the company’s willingness to facilitate fraud against consumers and the government, avoid regulation, dress up predatory loans and fees as revolutionary technology, and mislead investors with inflated metrics.

There’s also a negative side.

Even the summary is pretty breathtaking in the rang of allegations:

Most analysts are excited about the post-pandemic surge of Block’s Cash App platform, with expectations that its 51 million monthly transacting active users and low customer acquisition costs will drive high margin growth and serve as a future platform to offer new products.

Our research indicates, however, that Block has wildly overstated its genuine user counts and has understated its customer acquisition costs. Former employees estimated that 40%-75% of accounts they reviewed were fake, involved in fraud, or were additional accounts tied to a single individual.

Core to the issue is that Block has embraced one traditionally very “underbanked” segment of the population: criminals. The company’s “Wild West” approach to compliance made it easy for bad actors to mass-create accounts for identity fraud and other scams, then extract stolen funds quickly.

Even when users were caught engaging in fraud or other prohibited activity, Block blacklisted the account without banning the user. A former customer service rep shared screenshots showing how blacklisted accounts were regularly associated with dozens or hundreds of other active accounts suspected of fraud. This phenomenon of allowing blacklisted users was so common that rappers bragged about it in hip hop songs.

Block obfuscates how many individuals are on the Cash App platform by reporting misleading “transacting active” metrics filled with fake and duplicate accounts. Block can and should clarify to investors an estimate on how many unique people actually use Cash App.

CEO Jack Dorsey has publicly touted how Cash App is mentioned in hundreds of hip hop songs as evidence of its mainstream appeal. A review of those songs show that the artists are not generally rapping about Cash App’s smooth user interface—many describe using it to scam, traffic drugs or even pay for murder…

“I paid them hitters through Cash App”— Block paid to promote a video for a song called “Cash App” which described paying contract killers through the app. The song’s artist was later arrested for attempted murder.

Cash App was also cited “by far” as the top app used in reported U.S. sex trafficking, according to a leading non-profit organization. Multiple Department of Justice complaints outline how Cash App has been used to facilitate sex trafficking, including sex trafficking of minors.

There is even a gang named after Cash App: In 2021, Baltimore authorities charged members of the “Cash App” gang with distribution of fentanyl in a West Baltimore neighborhood, according to news reports and criminal records.

Beyond facilitating payments for criminal activity, the platform has been overrun with scam accounts and fake users, according to numerous interviews with former employees.

Examples of obvious distortions abound: “Jack Dorsey” has multiple fake accounts, including some that appear aimed at scamming Cash App users. “Elon Musk” and “Donald Trump” have dozens.

To test this, we turned our accounts into “Donald Trump” and “Elon Musk” and were easily able to send and receive money. We ordered a Cash Card under our obviously fake Donald Trump account, checking to see if Cash App’s compliance would take issue—the card promptly arrived in the mail.

Former employees described how Cash App suppressed internal concerns and ignored user pleas for help as criminal activity and fraud ran rampant on its platform. This appeared to be an effort to grow Cash App’s user base by strategically disregarding Anti Money Laundering (AML) rules.

The COVID-19 pandemic and nationwide lockdowns posed an existential threat to Block’s key driver of gross profit at the time, merchant services.

In this environment, amid Cash App’s anti-compliance free-for-all, the app facilitated a massive wave of government COVID-relief payments. CEO Jack Dorsey Tweeted that users could get government payments through Cash App “immediately” with “no bank account needed” due to its frictionless technology.

Within weeks of Cash App accounts receiving their first government payments, states were seeking to claw back suspected fraudulent payments—Washington State wanted more than $200 million back from payment processors while Arizona sought to recover $500 million, former employees told us.

Once again, the signs were hard to miss. Rapper “Nuke Bizzle”, made a popular music video about committing COVID fraud. Several weeks later, he was arrested and eventually convicted for committing COVID fraud. The only payment provider mentioned in the indictment was Cash App, which was used to facilitate the fraudulent payments.

We filed public records requests to learn more about Block’s role in facilitating pandemic relief fraud and received answers from several states.

Massachusetts sought to claw back over 69,000 unemployment payments from Cash App accounts just four months into the pandemic. Suspect transactions at Cash App’s partner bank were disproportionate, exceeding major banks like JP Morgan and Wells Fargo, despite the latter banks having 4x-5x as many deposit accounts.

In Ohio, Cash App’s partner bank had 8x the suspect pandemic-related unemployment payments as the bank that processed the most unemployment claims in the state, even though the latter bank processed 2x the claims as Cash App’s, according to data we obtained via a public records request.

The data shows that compared to its Ohio competitor, Cash App’s partner bank had nearly 10x the number of applicants who applied for benefits through a bank account used by another claimant – a clear red flag of fraud.

Block had obvious compliance lapses that made fraud easy, such as permitting single accounts to receive unemployment payments on behalf of multiple individuals from various states and ineffective address verification.

In an apparent effort to preserve its growth engine, Cash App ignored internal employee concerns, along with warnings from the Secret Service, the U.S. Department of Labor OIG, FinCEN, and State Regulators which all specifically flagged the issue of multiple COVID relief payments going to the same account as an obvious sign of fraud.

Block reported a pandemic surge in user counts and revenue, ignoring the contribution of widespread fraudulent accounts and payments. The new business provided a sharp one-time increase to Block’s stock, which rose 639% in 18 months during the pandemic.

As Block’s stock soared on the back of its facilitation of fraud, co-founders Jack Dorsey and James McKelvey collectively sold over $1 billion of stock during the pandemic. Other executives, including CFO Amrita Ahuja and the lead manager for Cash App Brian Grassadonia, also dumped millions of dollars in stock.

With its influx of pandemic Cash App users, our research shows Block has quietly fueled its profitability by avoiding a key banking regulation meant to protect merchants. “Interchange fees” are fees charged to merchants for accepting use of various payment cards.

Congress passed a law that legally caps “interchange fees” charged by large banks that have over $10 billion in assets. Despite having $31 billion in assets, Block avoids these regulations by routing payments through a small bank and gouging merchants with elevated fees.

Block includes only a single vague reference in its filings acknowledging it earns revenue from “interchange fees”. It has never revealed the full economics of this category, yet roughly one-third of Cash App’s revenue came from this opaque source, according to a 2022 Credit Suisse research report.

Competitor PayPal has disclosed it is under investigation by both the SEC and the CFPB over its similar use of a small bank to avoid “interchange fee” caps. A Freedom of Information Act (FOIA) request we filed with the SEC indicates that Block may be part of a similar investigation.

Block’s $29 billion deal to acquire ‘buy now pay later’ (BNPL) service Afterpay closed in January 2022. Afterpay has been celebrated by Block as a major financial innovation, allowing users to buy things like a pair of shoes or a t-shirt and pay over time, only incurring massive fees if subsequent payments are late.

Afterpay was designed in a way that avoided responsible lending rules in its native Australia, extending a form of credit to users without income verification or credit checks. The service doesn’t technically charge “interest”, but late fees can reach APR equivalents as high as 289%.

The acquisition is flopping. In 2022, the year Afterpay was acquired, it lost $357 million, accelerating from 2021 losses of $184 million.

Fitch Ratings reported that Afterpay delinquencies through March 2022 had more than doubled to 4.1%, from 1.7% in June 2021 (just prior to the announced acquisition). Total processing volume declined -4.8% from the previous year.

Block regularly hypes other mundane or predatory sources of revenue as technological breakthroughs. Roughly 31% of Cash App’s revenue comes from “instant deposit” which Block says it pioneered and works as if by “magic”. Every other major competitor we checked provides a similar service at comparable or better rates.

On a purely fundamental basis, even before factoring in the findings of our investigation, we see downside of between 65% to 75% in Block shares. Block reported a 1% year over year revenue decline and a GAAP loss of $540.7 million in 2022. Analysts have future expectations of GAAP unprofitability and the company has warned it may not be profitable.

Despite this, Block is valued like a profitable growth company at (i) an EV/EBITDA multiple of 60x; (ii) a forward 2023 “adjusted” earnings multiple of 41x; and (iii) a price to tangible book ratio of 13.1x, all wildly out of line with fintech peers.

Despite its current rich multiples, Block is also facing threats from key competitors like Zelle, Venmo/Paypal and fast-growing payment solutions from smartphone powerhouses like Apple and Google. Apple has grown Apple Pay activations from 20% in 2017 to over 70% in 2022 and now leads in digital wallet market share.

In sum, we think Block has misled investors on key metrics, and embraced predatory offerings and compliance worst-practices in order to fuel growth and profit from facilitation of fraud against consumers and the government.

We also believe Jack Dorsey has built an empire—and amassed a $5 billion personal fortune—professing to care deeply about the demographics he is taking advantage of. With Dorsey and top executives already having sold over $1 billion in equity on Block’s meteoric pandemic run higher, they have ensured they will be fine, regardless of the outcome for everyone else.

That’s just the high level summary. There’s a whole lot more detail in the report.

I have never once used Cash App. I have an ancient Square Reader floating around in a bag somewhere, but I never actually ran any transactions on it. I do have PayPal, because I pretty much have to in order to buy or sell on eBay (though I’ve gotten to the point I do almost no selling there). I don’t even use Apple Pay, despite having a MacBook Pro and iPhone.

Speaking of fees, here Louis Rossmann rants about how Square refuses to return fees for refunds:

Anyway, if you’re using Square or CashApp, maybe it’s a good time to look into alternatives…

Blackstone (NYSE:BX) has defaulted on part of a €531M bond backed by a commercial portfolio owned by Finnish property investment firm Sponda, which it acquired in 2017.

The private equity firm has repaid almost half of that figure, closer to €300M, according to a person familiar with the matter.

Currently €297.1M of the loan remains outstanding, according to ratings agency Fitch. The loan is secured against 45 properties in Finland, most of which are offices and the rest are stores.

Blackstone (BX) earlier sought an extension from holders of the securitized notes so that it could sell the assets and repay the debt, Bloomberg reported citing people aware of the matter. The commercial mortgage-backed security has since matured, without being repaid.

A Blackstone (BX) spokesperson told Seeking Alpha that “this debt relates to a small portion of the Sponda portfolio. We are disappointed that the servicer has not advanced our proposal, which we believe would deliver the best outcome for noteholders.”

Translation: “Shut up and let us force our losses on you rather than taking them ourselves.”

Though off in Finland, this story should probably receive more notice due to the “mortgage-backed” angle.

Remember the 2008 Subprime Meltdown, fueled by easy taxpayer-backed Fannie Mae money and bundled subprime mortgage securities? And how all sorts of banking fatcats got bailed out and never paid a price for their shenanigans?

Well, mortgage backed assets never went away, they just moved into commercial real estate. There’s untold trillions of dollars in Commercial Mortgage-Backed Securities (CMBS) across the world, and almost no one is keeping track of them. The average retail investor probably knows less about CMBS now than they did about subprime mortgages in 2008.

And you know one of the hardest-hit sectors following the Flu Manchu lockdowns? Commercial real estate. A whole lot of companies figured out that a whole lot of their work force can work from home, freeing them from having to pay expensive rent on office space.

Add to that the fact that the way CMBS are structured has immediate negative consequences on several cities. Because the rules of many CMBS state that the value of a property doesn’t need to be reevaluated as long as the asking price per square foot doesn’t change, commercial real estate spaces stay vacant for years rather than lowering their prices, screwing would-be renters and shrinking tax bases. (Louis Rossmann has been ranting about this for years.)

Blackstone Inc’s (BX.N) fourth-quarter distributable earnings fell 41% year-on-year as the world’s largest manager of alternative assets said on Thursday it cashed out fewer investments across key portfolios.

Blackstone has been dealing with rising redemptions at its flagship real estate income trust (BREIT), prompting the private equity firm to exercise its right to block investor withdrawals at 5% of the quarterly net asset value of the fund.

That’s not exactly a sign of unassailable strength.

I am very far indeed from being an expert on how Blackstone has structured its various holdings. I suspect that its various funds and trusts and CMBS are all well-siloed and isolated from each other, which is the smart way to do things. But The Biden Recession That Dare Not Speak Its Name, falling real estate prices, frozen rental prices and huge shift in the need for commercial real estate all point to some very difficult challenges for Blackstone to navigate.

Given the amount money Blackstone has spread around to the Chuck Schumers of the world, expect that there are going to be a whole lot of swamp creatures ready and willing to make any serious Blackstone financial problem into a big problem for the America taxpayer.

One-Party Democratic California is so desperate for cash they want to tax people for leaving.

Desperate to stem the stampede of cash cows — affluent residents — out of their state, they are trying to pass an exit tax for households with assets of $50 million or more. Current residents would have to keep paying for years after they have decamped to less hostile states.

Heaven forbid that these legislators should instead come to terms with the reasons so many productive residents flee or what they could do to make their state a more attractive destination for people and businesses. They aren’t much concerned with that, merely with stopping the flight of all that revenue. If they cared about the livelihoods of the people leaving, they probably would have governed in a way that didn’t prompt people to head for the exits.

This is probably unconstitutional nine ways to Sunday. Wealth tax, Ex-Post Facto law, taxation without representation, etc. It’s also likely to be counterproductive, as rich people are not only likely to leave the state preemptively to avoid being subject to it, but are exactly the people that can hire top-notch lawyers to get it overturned.

Louis Rossmann, who recently fled New York City to Austin, has additional thoughts:

“They are showing and demonstrating here they have no confidence in their ability to govern better, or in their ability to actually give the customers of that state what they want, because they’re telling you ‘We’re not going to make things better. Rather, if you leave we are going to figure out a way to fine you.'”

“It demonstrates a sick ideology that’s both just authoritarian and disgusting in nature.”

“It’s not like [the tax rates in California and New York] just spiked up insanely over the past one or two years, they’ve been higher than the tax rate in Texas and Florida for as long as I’ve been alive, by a fairly large margin. This is not news. It’s something else in addition to that, and they don’t even appear to be interested in trying to figure out what that is.”

“Florida and Texas…have not had income tax for a very long time.”

“Maybe it would make sense to actually ask people what changed over the past two or three or five years that caused you to decide that you want to move your business and get the fuck out.”

“I could tell you from experience that losing half of your employees, putting all your stuff in a truck, carting it across the country. and spending months putting it all back together is insanely stressful, and not something that I’m going to do so I could save six or eight percent of my income tax.”

“Why are you then going to bake more taxes, and then have a fine for leaving that is then going to discourage anybody else that has the same concern from ever coming to your state thereby ensuring that the population of people that are productive and create value diminishes.”

“The idea of being taxed based on what you are worth at a particular time without actually cashing it out is insane to me.”

Long, correct discussion of why long-term capital gains are taxed at a lower rate snipped. (I doubt many of my readers don’t already understand, or disagree.) Ditto the discussion of how investment creates jobs.

“People deciding to defer their gratification, to decide ‘I will wait for the large payoff 10 to 20 years from now rather than make a decision that results in me getting more money right now,’ and I think that that it should be discussed more often because if it’s not, then we are going to end up with stuff like this.”

He discusses the slippery slope argument: The bill already states the tax will start at billionaires, but then in two years hit people with a net worth of $50 million or more. “Once it gets low enough like once this makes its way off to 10 million or a million, because again this is going to slip.”

And just wait until it hits the net worth not only of individuals, but of businesses.

Here’s a Louis Rossmann rant that hits home for me: How online menu apps for restaurants suck compared to ordinary paper menus.

I hate having to scan QR codes on my phone just to get a menu so badly that I will avoid eating at any restaurant that wants to make me do that. ToastTab is especially infuriating.

And while I’m ranting about things that infuriate me, having you rate your transaction when ordering at the counter, before you’ve even received your food, is so unacceptable that I always give them the lowest rating possible when they make me do that.

Ahem. Back to the topic at hand.

Everyone but a small minority of perpetual covid paranoids have gotten over the stupidities of 2020. It’s time for every restaurant to go back to printed menus as the default.

In my previous post on crime statistics, several commenters (here and over on Instapundit) noted that Louis Rossmann had also put up a video covering the final straw that caused him to decide to leave New York: an audit he was subjected to after making a video discussing how incompetent New York taxing authorities were. I had seen it, but it was a bit long and I already had the crime statistics video cued up. Here it is by way of prologue for the next video.

The upshot is that, after having millions in fines and the possible destruction of his business dangling over his head for over a year thanks to New York authorities, the audit found that Rossman’s reporting had a 0.11% error rate.

If you thought that was the end of it, you underestimate the penny-ante fury of petty bureaucrats against those who would dare to criticize them. New York has launched a spite audit of Rossmann on his way out of the state:

Yet another excellent reason for business owners to leave New York as soon as possible…

Some leftists have asserted, despite all evidence, that crime rates in blue states are no higher than in red states. One for this illusion is that Soros-backed DAs game the statistics. Another is that in many deep blue cities, residents simply no longer report crime, because they know police won’t investigate the case or pursue suspects, and that even if suspects are apprehended, those same Soros-backed DAs will simply let them go without bail. Another is that, even if citizens try to make a complaint, the police will simply refuse to take it, believing it to be a waste of their time.

Here New York City-to-Austin transplant Louis Rossmann talks about the decay of the Big Apple from it’s Rudy Giuliani broken windows policing heyday to its current state of disorder, and why you can’t trust the statistics.

Friday’s LinkSwarm mentioned the plight of New York City bodega clerk, who was viciously attacked by the convicted-felon boyfriend of a patron whose credit card had been refused. Defending himself from the attack, Alba stabbed his attacker to death, and was charged with murder.

GoFundMe has deleted the legal defense fund page for the hard-working Manhattan bodega worker holed up at Rikers Island on a whopping $250,000 bond after he fatally stabbed a violent ex-con he was trying to fend off.

Jose Alba, 51, is currently languishing behind bars at the notorious jail despite surveillance video capturing the alleged victim, Austin Simon, 35, storming behind the counter of the bodega to attack him Friday night.

Alba’s family insist he was acting in self-defense when he grabbed a knife to fight off Simon inside the Hamilton Heights Grocery.

Relatives immediately launched a GoFundMe page to help raise funds to cover Alba’s sky-high bail and legal fees after he was hit with a second-degree murder charge — but the page was mysteriously removed Wednesday night.

“Our terms of service prohibit fundraising for the legal defense of a violent crime. At this time, the fundraiser has been removed and all donors have been refunded,” GoFundMe said in a statement Thursday.

The page had already raised $20,000 for Alba when it was suddenly removed, the Daily Mail reported.

Under GoFundMe’s terms of services, the platform can’t be used for the legal defense of “alleged crime associated with hate, violence, harassment, bullying, discrimination, terrorism.”

Controversial Manhattan District Attorney Alvin Bragg has faced backlash over Alba’s case after his office brought the charges — and then pushed for $500,000 bail for the father-of-three at his arraignment Saturday.

This is just the latest example of a Soros-backed Democrat DA filing charges against law-abiding citizens daring to defend themselves from violent attacks by felons. (See also: Kyle Rittenhouse.)

Former New York City resident Louis Rossmann has a nice video rant on the subject.

“If you are a criminal, Alvin Bragg has your back!”

You have felonies that have been, in many cases, decreased to petty misdemeanors. So if you commit a felony, it’ll get decreased to a petty misdemeanor. However if you are one of the people that allow society to function, one of the people that puts in work every day, a law-abiding citizen that simply wants to go home without getting killed by somebody half his age, who has a criminal record, who is beating you up, we throw the book at you this is sickening and tiring and it has to stop!

“They will always simp for the criminal.”

He’s right about everything, but the name “George Soros” never appears anywhere in his rant. Pretty much every-time you see this sort of coddling of criminals and throwing the book at the law-abiding, a George Soros-backed DA is the one making the prosecution decisions.

Soros-backed DAs seem intent on destroying the social fabric of America, and of prosecuting the law-abiding Americans as though the right to self-defense didn’t exist. It goes hand-in-hand with the Democratic Party’s obsession with disarming law-abiding Americans.