This is a very different post than the one I set out to write.

When I talked about the current memory shortage, I didn’t really cover Chinese memory fabs, as I lumped them in with “older fabs” churning out older types of memory that weren’t relevant to the current memory crunch. However, after I posted, I came across news for ChangXin Memory Technologies (CXMT). According to this list of semiconductor fabs (which I’ve used as a starting point for many semiconductor posts), their Fab 1 in Hefei, China started running DRAM on a 19nm process node in 2019. That’s unsuitable to fab the high bandwidth memory (HBM) demanded by the AI buildout that’s currently making money for Samsung, SK Hynix and Micron hand-over-fist. But it is already churning out DDR4 (and low-power DDR4 for the mobile market), and just last year started fabbing DDR5. Naturally, being a Chinese company, they probably stole their technology from Samsung and SK Hynix.

CXMT just had a public offering on the Shanghai stock exchange that went very well.

ChangXin Memory Technologies (CXMT), mainland China’s only mass producer of DRAM—

Technically untrue. SK Hynix’s C2F fab in Wuxi, China turns out DRAM, but I included it in SK Hynix’s global output.

—officially launched its initial public offering on the STAR Market, raising approximately CNY 57.9 billion (roughly $8.4 billion) at CNY 8.66 per share, setting a new record for the board. Fueled by surging AI server demand, the company turned profitable for the first time in 2025, with net profit for the first half of 2026 estimated between CNY 50 billion and CNY 57 billion. Supply chain sources indicate that major PC manufacturers including Dell, HP, and Lenovo have already locked in CXMT’s DRAM production capacity through the end of 2027.

I haven’t been able to verify this tech name dropping, but I haven’t tried very hard, because I was chasing down more fundamental questions.

Meanwhile, although Apple is evaluating the integration of CXMT’s LPDDR5X chips, a Bank of America report points to three major constraints—geopolitical risks, technical specifications, and patent issues—making large-scale, substantial procurement unlikely in the near term. CXMT’s listing also provides a glimpse into China’s memory industry landscape, where breakthroughs are being made across DRAM, NAND Flash, and NOR Flash, though a significant gap remains compared to the world’s top three manufacturers.

I’ve seen the “Apple testing CXMT chips” in more reputable sources, so let’s assume it’s true for now.

$8.4 billion is a big chunk of change, but in the semiconductor world that will buy you…one 14nm fab, with a bit of change left over.

But according to some breathless analysis in the sort of farflung web outlets that don’t make up part of your regular feed:

A new report claims that CXMT will come exceptionally close to Micron’s DRAM wafer production capacity by the end of this year. In the coming years, China could become the world’s second-largest producer of DRAM globally, fundamentally altering the global DRAM market.

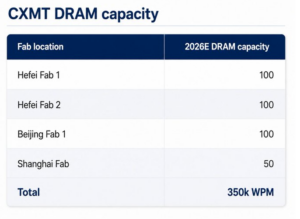

It has been estimated that CXMT will end 2026 with 350,000 wafer starts per month (WSPM). That’s a mere 25,000 fewer wafers than Micron. China has reportedly forced CXMT to share its DRAM technology with other Chinese semiconductor companies, including JHIC, Swaysure, and XMC (a YMTC subsidiary).

Obviously, you’re not getting 350,000 wafer starts per month from one fab. That piece tells us that CXMT has three fabs, two in Hefei and one in Beijing, with another in Shanghai due to come online later this year.

However, the source they cite is…a random guy on Twitter with 754 followers. I’d like a more solid source than that.

Could CXMT actually pay for two more modern-but-not-cutting edge fabs? Maybe. The city of Hefei (and possibly other government and CCP-connected entities) has been subsidizing them.

The fact that the additional fabs aren’t on the Wikipedia list isn’t dispositive. The Source of All Vaguely Accurate Knowledge relies on volunteer labor, and overwhelmingly English-speaking labor at that.

So let’s go to Google maps and take a look at the aerial view of them.

And here’s where the real trouble starts.

“ChangXin Memory Technologies Beijing” brings up nothing.

OK, let’s ask Google AI: “Where is ChangXin Memory Technologies semiconductor fab in Beijing?” Google’s answer:

ChangXin Memory Technologies (CXMT) operates its Beijing semiconductor fabrication plant (known as Fab C1/C2) within the Beijing Economic-Technological Development Area (BDA), also commonly referred to as the Yizhuang Development Zone in the southern suburbs of Beijing. Production at this specific memory/DRAM site began in 2022.

Hmmm. Let’s see if we can narrow that down: “What is the street address of ChangXin Memory Technologies semiconductor fab in Beijing?” Google’s answer:

The primary location for this facility is: Building 52, No. 2 Jingyuan North Street

Beijing Economic-Technological Development Zone

Beijing, China

Great! Let’s pop that into Google Maps.

And here we run into multiple problems:

Problem 1: That’s an empty square in a parking lot outside “BDA International Business Park,” which includes multiple shops and restaurants within, so that’s obviously not a fab. Problem 2: It appears that Google’s “float over” street grid in Beijing is offset about a quarter mile east from the actual location. Problem 3: Adjusting that marker a quarter-mile west puts it in a cluster of much smaller buildings amidst trees, all of which are obviously too small to be fabs.

Worse still, asking the question differently brings up a completely different address. “Where is ChangXin Memory Technologies located in the Beijing Economic-Technological Development Zone Beijing, China.” Answer:

The specific facility and office address is: No. 51 Jinghai 3rd Road, Courtyard 1, Building 1 (Floors 1-5)Beijing Economic-Technological Development Zone, Beijing, China

Here it can find the road…and nothing else.

Expanding further and further out using aerial views of Beijing in the general vicinity, I find a building complex that might, might qualify, as it has the extensive air-handling equipment that you might find on a fab:

But there’s no guarantee that’s it and not another big factory. (It might also be SMIC’s Beijing fab in the same general area, which Google seems to have trouble finding with any precision as well.)

Likewise, doing a Google image search on “CXMT beijing fab” brings up mostly greenfield artist renderings and pictures of other CXMT buildings, not an actual fab in a Beijing industrial zone. (By the way, the picture of the big building with the curved purple building in the bottom of the pic is an actual fab, but it’s Yangtze Memory Technologies’s NAND flash fab in Wuhan.)

Maybe Google sucks at bringing up information on Chinese locations. In a move I rarely make, let’s ask ChatGPT “What is the exact location of ChangXin Memory Technologies Beijing fab.” Answer:

There is no publicly confirmed street address for the CXMT (ChangXin Memory Technologies) fabrication plant in Beijing….

As of today, CXMT has not publicly disclosed the precise street address or GPS coordinates of the Beijing fab. Unlike many semiconductor companies that publish corporate campus addresses, this facility appears to be intentionally identified only at the industrial park level in public documentation.

As the kids say today, “Super sus, bro.”

What does CXMT’s own website say about their Beijing fab?

“2020.06 CXMT Fab C Project kicked off”

“2022.01 Operation began on Fab C1 (Beijing) trial production line”

OK, now I’m really suspicious. You don’t go from starting work on a fab to pilot production in 18 months, not even in China. Even without waiting for an ASML EUV stepper that they can’t get, the lead time for all the fab equipment alone is likely to be longer that.

To be fair, I couldn’t use Google maps to find their Hefei fab(s) either, but that one does come up in Apple Maps if you search for “Changxin Cunchu Technology Co., Ltd.” And scrolling around Google Maps does bring up some large buildings in that precise location, so I am willing to believe CXMT has one or more fabs there. But searching on “Changxin Cunchu Technology Co. Beijing China” brings up nothing on Apple Maps, and Google automatically changes the name to something else that isn’t a semiconductor company.

Remember, previous Chinese semiconductor companies have proven to be smoke and mirrors and shell games all the way down. Right now, I question whether CXMT even has a fab in Beijing. That doesn’t mean they don’t. The map is not the territory, and Google is obviously having problems with both their mapping and AI technology when it comes to China. (And this is also a lesson, once again, that AI can’t distinguish between truth and falsehood, as “garbage in, garbage out” still applies, and the Internet-based datasets the AI hyperscalers have been using to feed their baby Frankenstein monsters are full of garbage.) But CXMT would not be the first Chinese company to lie about their business to con the gullible. Or even the thousandth.

Anyway, if you have an actual reliable source (not a news article based on a tweet based on press releases) that CXMT has an actual fab in Beijing, feel free to share it in the comments below.