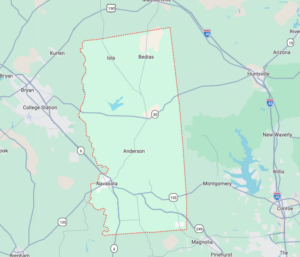

Iola Independent School District (ISD) and Anderson-Shiro Consolidated Independent School District (CISD) both voted to pass a partial tax abatement deal for SpaceX’s “Terafab” project in Grimes County.

Each phase of the four-phase Jobs, Energy, Technology, and Innovation (JETI) application was approved by a vote of 5 to 2 in both Iola ISD and Anderson-Shiro CISD on Tuesday.

SpaceX is a space exploration company founded by tech magnate Elon Musk, who serves as its CEO and chairman. The company is collaborating with computer company Intel and electric vehicle company Tesla, of which Musk is also the CEO, on the Terafab project.

Terafab is a proposed semiconductor megafacility that intends to produce chips for AI computing both on earth and in space. SpaceX calls the project “the most epic chip-building effort ever,” and aims to produce up to one terawatt — one million megawatts — of AI compute capacity annually. The project is projected to cover 100 million square feet of the Brazos Valley, with a projected investment of $119 billion.

The project will supposedly create thousands of temporary and permanent jobs in the area.

Grimes County, an agricultural county within the Brazos Valley, has a population of about 30,000. The proposed Terafab project’s reinvestment zone — the area of land proposed by SpaceX to qualify for tax abatement — would cover areas under the jurisdiction of Iola ISD and Anderson-Shiro CISD.

Last month, the Grimes County Commissioners Court agreed to a 35-year tax abatement over the proposed build, which will provide the county with $20 million per year for its 35-year duration. The abatement will be accomplished through a payment in lieu of taxes or “PILOT” program.

A multi-phased project, SpaceX’s phase one investment in Iola ISD would amount to over $6 billion, and for Anderson-Shiro ISD, phase one would bring in over $10 billion to the district.

While I’m philosophically opposed to special tax breaks for large corporations, this is a far cry from some of the old “we pay nothing forever for the privilege of placing our factory in your Podunk town” deals of the past. When you’re talking billions, that’s a considerable amount of cheddar for a rural school district. And a cutting-edge semiconductor fab is the sort of thing that’s going to be generating jobs and taxes for a long, long time, and nobody is ever going to close the fab and move those jobs to China.

Through Texas’ JETI program — created by the 88th Legislature in 2023 — Terafab is able to apply for a tax abatement deal with school districts; the company, relevant school districts, and the governor’s office enter into a 10-year agreement. If the company meets investment and job creation requirements, the agreement serves to limit the taxable value of the project for school district maintenance and operations taxes.

“The point of the JETI is the tax revenue, bringing in the investment to the local community,” stated Alec Pointer, president of Iola ISD’s school board, during a public hearing last week.

Pointer added that SpaceX will pay 92 percent of the bond debt in Iola ISD.

While there are some additional regulatory clearances, I have to assume at this point that the fab is all but a done deal.

A class action lawsuit has been filed against memory giants Samsung, SK Hynix, and Micron alleging the nefarious, cartel like action of…making the products with the highest profit margins.

The world’s biggest memory chip makers are once again facing accusations of manipulating prices.

A class-action lawsuit filed on Thursday, June 25, in a California federal court alleges that Samsung Electronics (SSNLF), SK Hynix (SKHY), and Micron Technology (MU) coordinated to restrict DRAM supply and push prices sharply higher during the AI boom.

The complaint, filed in the US District Court for the Northern District of California under case number 3:26-cv-06345, claims the companies reduced production of traditional DDR3 and DDR4 memory while shifting capacity toward high-margin AI memory products such as HBM chips used in data centers.

Not to mention DDR5.

However, the companies have not been found liable for now, and no trial date is set.

According to the lawsuit, DRAM prices have surged nearly 500%-700% over the past four years, reported Time of India. Plaintiffs argued that in a competitive market, rising prices should attract more supply, but production cuts continued instead.

Snip.

According to Jefferies, memory prices could rise another 40%-50% next quarter and 30%-40% more in the following quarter, reported analysts like Bull Theory on X, with normalization unlikely before 2028. The rising memory costs are already filtering into consumer electronics prices worldwide.

Does this situation suck if you’re trying to buy or build a new PC with lots of RAM? Absolutely. But there’s no nefarious market coordination at work among those big three, just the confluence of a variety of market trends. So let’s break it down:

Manufacturers switching production from a less profitable product to a more profitable product isn’t some nefarious conspiracy, it’s how the market works. If they’re getting premium pricing for HBM memory that sells out instantly for the AI bubble, that’s what they’re going to produce. A whole lot of tech companies depended on the spot market for RAM because it gave them more flexibility and costs savings, but now it’s biting them in the ass. Their lack of foresight does not indicate a conspiracy or market failure.

Why are there only three big RAM manufacturers? Because a whole lot of other companies dropped out of the market because the game became too expensive to play. RAM makes money hand-over-fist during boom times (like now), but barely breaks even during busts. A whole lot of different companies used to produce memory, Intel and Texas Instruments among them. Remember when Japan Inc. was going to take over the world and the Japanese semiconductor giants (NEC, Toshibu, Fujitsu, Hitachi, etc.) were accused (with some justification) of dumping RAM below cost to capture market share with the backing of state agency MITI? None of those Japanese giants are in RAM any more because, in the wake of the Japanese asset bubble busting in 1991, building new state-of-the-art fabs that doubled in price every four years became a game too expensive for them to play.

Rising prices should attract more supply, but it takes about three years and costs about $25 billion to build a state-of-the-art fab. Because standard memory technology still has a capacitance limit, you don’t necessarily need an under-10nm fab, so maybe you can spend a bit less, but you’re still spending over $10 billion on a fab, and you probably still need an ASML EUV stepper, though not the very latest one.

And indeed, Samsung, SK Hynix, and Micron all have two new fabs each in the pipeline scheduled to come online this year through 2028. The Micron and SK Hynix fabs will both be dedicated to producing memory. As for Samsung (which has a lot of fingers in a lot of semiconductor pies), I would guess their newest South Korean fab will be dedicated to memory, while their 4-5nm Taylor, Texas fab will not. Building new fabs are not the actions of monopolists who want to artificially constrain supply.

Indeed, the “they’re artificially constraining supply” nonsense suggests that they’re producing fewer memory chip than they could otherwise, and that’s just not how the industry works. Fab production lines run 24/7/365 (indeed, they pay technicians triple to work Christmas), because every hour a modern fab is down they’re losing millions in lost profit.

Building new fabs is still a risky bet, because the industry is extremely cyclical. No matter how furious the boom now, the next bust is always around the corner. Back when I was working at Applied Materials, the cycle was described as trains linked together with slinkys. First software takes off, then hardware gets yanked along, then the chip manufacturers get yanked, and then, finally, semiconductor equipment manufacturers get yanked into motion, and shortly after that happens, the bust hits the front of the train, and the trailing cars all crash into each other. (The standing joke at Applied Materials was that you could tell the bust was on the very moment the company broke ground on a new manufacturing facility.) Build a new $25 billion fab at the wrong part of the cycle and it could take a company much longer to amortize it than they expected. That’s why so many companies switched to the foundry model.

Speaking of foundries, could they be a solution to the memory crunch? Potentially, but there you’re running into the same AI boom-induced wafer start constraints that plague the memory sector. TSMC is fabbing AI chips for Nvidia (and most of its competitors) as fast as it possibly can. Maybe they can profitably book runs on slightly older (but not “mature”) TSMC fabs, but they’re still competing with every other fabless company supporting the AI build-out for the same wafer starts. A whole lot of different silicon goes into a data center.

Could an existing semiconductor manufacturer jump into the existing space? Yes, and in fact Intel has announced plans to do just that, though evidently with their own proprietary, next gen “Z-Angle Memory (ZAM),” which isn’t going to do squat to relieve this year’s DDR3/4/5 shortage. Still, they have enough slightly trailing edge fabs to do it, though Intel has had trouble executing at speed in the past.

Could another company jump into the semiconductor fab race as an integrated device manufacturer for memory? Risky but possible. Someone like Apple could decide that memory shortages are an existential threat to its business model and spend the tens of billions to get into the game. And indeed, Apple is already spending some $500 billion to reshore its supply chain back into the US, so that would fit right in. Apple could potentially contract with TSMC (or even Micron) to build and run a memory fab. (Samsung is a trickier proposition, since the two are fierce competitors as the biggest smartphone manufacturers in the world, but there’s still a lot of “cooperatition” between the two, so it’s not beyond the realm of possibility.) But the three year lead time still applies.

Entire tech boom and bust cycles have come and gone in an era in which RAM is cheap and plentiful, a situation people have come to think of as “normal.” Just as with higher credit rates, a whole lot of business models that were viable in an era of cheap memory are suddenly going to stop being so in an era of scarcity. Some companies will be able to raise prices and remain profitable, and others won’t. Not everyone will be hit, as a lot of embedded devices use older types of memory that hasn’t gone through the roof. There are all sorts of older fabs churning out older types of memory that aren’t relevant to this discussion.

The idea that Samsung and SK Hynix are colluding is particularly laughable, as the two Korean chaebol backing SK Hynix (Hyundai and LG (AKA Lucky Goldstar)) both hate rival Samsung with a passion.

The current shortage, as painful as it is to so many, isn’t the result of a nefarious cartel, it’s just the free market working like it always does at the interface between supply and demand. It’s just that cutting-edge semiconductor supply has a whole lot more lead-time constraints that most other economic sectors.

The AI Bubble seems considerably worse than the Dotcom Bubble (which was only partially about the Internet; updating hardware and software to avoid the Y2K bug also drove a lot of spending in the same timeframe), and its inevitable bursting (or just deflating) is going to relieve pressure on everyone else that needs 10nm or smaller wafer starts.

When last we checked, Terafab, the cutting-edge megafab being built to produce AI chips for Elon Musk’s Telsa/SpaceX/xAI consortium, was going to be built and run by Intel, but the location was up in the air. Now, according to regulatory filings, it looks like the location may well be Grimes County, Texas.

Elon Musk’s SpaceX has proposed an initial investment of $55 billion to build a semiconductor manufacturing facility, called Terafab, in Texas, according to a filing made public on Wednesday.

The facility, a joint project with Tesla, comes as Musk seeks to secure in-house access to advanced chips, though analysts say the scale of capacity he has outlined would likely require far greater investment.

SpaceX is also targeting a June IPO that could value the company at around $1.75 trillion.

Musk has been tightening integration of AI efforts across his companies, with SpaceX acquiring his startup xAI earlier this year in a deal focused on building space-based data centers for artificial intelligence processing. The combined entity was valued at $1.25 trillion.

The Terafab project would involve a multi-phase chip fabrication and advanced computing complex aimed at boosting domestic semiconductor production in the United States. SpaceX estimates total investment could rise to $119 billion if additional phases are completed.

The facility is planned in Grimes County within a newly designated reinvestment zone, where local officials are expected to consider a property tax abatement agreement at a June meeting.

The proposed facility could help reduce reliance on external suppliers such as Samsung and Taiwan Semiconductor Manufacturing Co., SpaceX flagged plans to “manufacture our own GPUs” as part of “substantial capital expenditures” outlined in its S-1 registration, according to excerpts reviewed by Reuters.

The filing also highlighted risks around supply, noting the company lacks long-term contracts with many direct chip suppliers and will continue to rely significantly on third parties. SpaceX added there is no assurance it will meet its Terafab objectives within expected timelines, or at all.

That last bit is just the usual publicly-traded stock disclaimer blather.

Grimes County is quite rural, but it’s also on the edge of the Houston exurbs (which I would say end at Magnolia), right in a triangle between Huntsville, Conroe and College Station.

According to this tweet, the site is going to be near the Gibbons Creek Reservoir, which is between College Station and Huntsville.

SPACEX / TERAFAB: The County of Grimes, Texas, will be home to SpaceX's Multiphase, next gen, vertically integrated semiconductor manufacturing and advanced computing fabrication facility.

Building it in such a rural area probably means less regulatory hurdles, but building it within commuting distance of Texas A&M in College Station (and, to a lesser extent, Sam Houston State in Huntsville) is going to provide access to a technologically savvy labor pool of engineers, technicians, etc.

California’s heavy-handed Flu Manchu lockdown was the straw that finally convinced Musk to pick up stakes and move to Texas. It looks like that decision will result in Texas becoming the home for companies with market capitalizations of several trillion dollars.

After the initial report on Elon Musk’s planned Terafab project, there were a whole lot of questions about how Musk was going to get his ambitious semiconductor fab project up and running. Now a very, very big piece of the puzzle (like, 85%) has been solved: Intel is going to build it for him.

In an unexpected turn of events, Intel on Tuesday said that it had joined Elon Musk’s TeraFab project. The announcement mentions Intel’s ability to develop, produce, and package advanced processors in high volumes, which could help Tesla, SpaceX, and xAI to get enough compute performance for next-generation AI and robotics applications. However, the announcement made in an X post you can expand below does not reveal how exactly Intel will help TeraFab.

“Intel is proud to join the Terafab project with SpaceX, xAI, and Tesla to help refactor silicon fab technology,” a statement by Intel reads. “Our ability to design, fabricate, and package ultra-high-performance chips at scale will help accelerate Terafab’s aim to produce 1 TW/year of compute to power future advances in AI and robotics. It was fun hosting Elon Musk at Intel this past weekend!”

The announcement is not accompanied by any press releases or SEC filings, which raises questions about the framework of the collaboration between Intel and TeraFab, as well as any possible legal bindings. In fact, the post in X is deliberately written in a way that barely reveals any concrete details about the structure of the partnership.

Officially, TeraFab is positioned as the “most epic chip-building effort ever” that is to combine “logic, memory and advanced packaging under one roof,” which implies localized production in a massive facility. Furthermore, the company is hiring managers to build a greenfield semiconductor fabrication plant in Texas. By contrast, Intel’s wording rather implies a virtual semiconductor production ecosystem, or even a consortium that involves chip design, manufacturing, and packaging at Intel and demand from Tesla, SpaceX, and xAI. How such a consortium would differ from a typical wafer supply agreement that large companies tend to have with their suppliers is something that is unclear at this point.

It makes perfect sense for one of only three global semiconductor manufacturers (and the only American company of the three) to help Musk realize his vision. Though nobody has spelled it out, my guess is it’s going to be very similar to the way Apple funds its manufacturer ecosystem through partner build-outs: Musk is going to pay Intel to build and run the fab, and Musk’s Telsa/SpaceX/xAI consortium is going to buy the dedicated output at a given price for x number of years, after which Intel can use the fab for other projects.

This makes a great deal of sense for both parties, especially if Intel has its 18A process dialed in. This is not a given, as Intel’s process screwups at previous nodes let TSMC and Samsung lap them in the sub-10nm race. But Intel yields at that node are reportedly rising.

And having Intel do all the heavy lifting means Musk’s new company doesn’t have to negotiate with Applied Materials, ASML, LAM, etc. Intel already has standing purchase agreements with all of them, and likely already knows what it wants and what the lead times will be to equip the new fab. Not to mention already knowing which contractors they’ll get to bid to build it.

If that’s actually what’s happening, that clears up a whole lot of questions about the project. Now, it doesn’t make Musk’s crazy “2027 volume production of 1 million wafer starts a months” any more feasible, but a fully functional Intel fab up and running at full-tilt by 2029 pumping out chips for xAI/SpaceX/Telsa is entirely feasible.

When last we checked, Microsoft CEO Satya Nadella was busy trying to shove Copilot, their AI tool, into every crevice of every Microsoft product. Finally, enough users seem to have complained loudly enough to get them to rethink the strategy.

Microsoft is vowing to focus on quality with future Windows 11 releases, which includes better performance and reeling in the company’s Copilot footprint over the OS.

“Quality” and “performance” go together with Windows like vanilla ice cream and used motor oil.

On Friday, Microsoft President for Windows and Devices, Pavan Davuluri, announced the “commitment to quality” in both a blog post and an email to users.

The plan calls for bolstering the “performance, reliability and well-crafted experiences” over the OS for this year.

That sort of suggests that “performance, reliability and well-crafted experiences” were not priorities for Windows in previous years, doesn’t it?

“These areas have meaningful impact on how you experience Windows: how fast it starts and responds, how stable it is under real workloads, and how consistent and thoughtful the experience feels,” Davuluri wrote.

PC users will be happy to know that one goal is reducing Windows 11’s resource usage to free up more capacity.

This would be great news if anyone trusted them to do that. Countless times in the past, Microsoft has pledged to reduce resource usage in Windows, but the bloat always returns.

Another priority is “less noise, less distraction and more control across the OS.”

Surprisingly, the blog post makes little mention of AI. Instead, Davuluri merely says the company wants “to be thoughtful about how and where we bring AI into Windows.”

“You will see us be more intentional about how and where Copilot integrates across Windows, focusing on experiences that are genuinely useful and well‑crafted. As part of this, we are reducing unnecessary Copilot entry points, starting with apps like Snipping Tool, Photos, Widgets and Notepad,” he said. Users can expect the change to roll out this month and in the next for Windows 11 preview releases.

Finally, the backslash against MicroSlop has gotten so loud that it’s even penetrated Redmond’s C-Ring. This is indeed progress, given that earlier this month Microsoft was literally banning users from its Discord for using the term. So give them credit for at least realizing that they have a problem.

Davuluri made the announcement months after he faced backlash for tweeting that “Windows is evolving into an agentic OS,” which caused some users to retort the company was obsessing about AI over basic Windows 11 performance. A January Windows 11 release that prevented PCs from booting up or going to sleep sparked more complaints about the OS’s stability.

There’s that vaunted Microsoft quality again.

Last month, Davuluri indicated he was taking the criticism seriously. Microsoft is also facing increased competition from Apple, which released its most affordable MacBook so far, the Neo, which has been a hit among consumers and reviewers.

Yeah, let’s talk about the state of Windows-based PCs and the competition. This was supposed to be a big year for PCs, but then reality hit.

There was supposed to be a massive tailwind for the PC market this year. Windows 10 reached end-of-life in late 2025, meaning that somewhere around 1 billion PCs worldwide stopped receiving security updates. This is less of an issue in the consumer PC market, but it’s a big deal in the business PC market.

PC OEMs like HP were set up for success in 2026, but the AI boom has complicated the situation. Enormous demand for DRAM and NAND chips from the AI infrastructure build-out, coupled with memory chip manufacturers shifting production to server products, has left the PC market with scraps. Memory chip prices have surged, pushing up the bill of materials and forcing price increases.

Gartner expects PC prices to surge by 17% this year, prompting consumers and businesses to hold onto their current PCs for longer. Budget PCs as a category could essentially disappear, leaving a large swath of consumers in a bind. Gartner expects PC shipments to tumble by 10.4% in 2026.

In one of life’s little ironies, the same AI bubble that Microsoft was trying to shove down user’s throats is what’s making buying a new PC less affordable and crushing sales. But it’s not stopping Apple.

HP is an obvious loser in this scenario, but there’s a surprising winner as well: Apple….

Apple is also exposed to rising memory chip prices across its entire device business. However, the company is seizing an opportunity to bring Windows PC users into its ecosystem.

Apple announced the MacBook Neo last week. The 13-inch entry-level MacBook starts at $599, a price that PC OEMs like HP will have trouble hitting as memory prices spiral higher. The Neo is powered by the A18 Pro chip, the same SoC used in the iPhone 16 Pro family. Higher-end MacBooks use Apple’s M-series chips, but the underlying technology is essentially the same.

Apple has equipped the Neo with 8GB of unified RAM, shared between the CPU and GPU, as well as a 256GB solid-state drive. These are really the bare minimums for a usable PC, but it’s enough for a solid entry-level experience. Early reviews have been positive, although full third-party reviews haven’t yet arrived ahead of launch.

Apple is playing the long game here. If there was ever a time to launch a budget MacBook, it’s right now. With memory prices driving up the cost of Windows PCs, a $599 MacBook should be appealing to budget-conscious consumers. Apple also offers the Neo to the education market for a discounted price of $499.

If Apple can grow its Mac install base and steal away market share from Windows-based PCs, the company will be setting up its Mac business for stronger growth down the road. Once the memory situation normalizes and the macroeconomic environment improves, Apple will have a larger base of Mac users eager to upgrade when the time comes.

This is probably correct. $599 is getting down around the price range for what used to be called netbooks, though that market segment seems to have largely died, at least among Windows users. (There still seems to be a market there for Linux users.)

Remember: Apple is the company that saw other companies dumping dump-trucks full of cash into AI build-outs and went “Nah, bro, I’m good.”

Google will spend approximately $90 billion on AI infrastructure this year. Meta has committed $65 billion. Microsoft, Amazon, and Alphabet are collectively spending over $300 billion. Apple, meanwhile, is spending just $12.7 billion on capital expenditure for the entire fiscal year.

As a hardware manufacturer, Apple can just wait for the AI wars to shake out and partner with the winner (if any).

And here’s a mildly amusing video on the whole situation.

I’m pretty sure Microsoft users wouldn’t object to Copilot if it was something optional you could turn off, and if the granularity of control allowed users to keep it entirely out of products they don’t want it in. But no, letting users decide isn’t the Microsoft Way, and they had to try shoving it into everything to justify the huge sums of money they were throwing into AI.

A bunch of AI-related news has popped up this week, so let’s do a roundup.

Some AI companies are complaining that TSMC is killing the AI boom by not expanding rapidly enough:

Asianometry notes that TSMC’s caution at expanding is amply justified by the boom-and-bust nature of the semiconductor industry:

“I’m hearing many similar views in the Silicon Valley Borg that TSMC is the break or limiter on the AI boom, as if they’re the reason why we don’t have AGI yet. Because they didn’t and still don’t believe.”

“If we can ever say that a company that spent $41 billion on capital expenditure in 2025, with another $53 to $56 billion in 2026 planned, is sitting on its hands, doing nothing.”

“TSMC having 90% share of the AI chip market looks pretty unhealthy. That should go down and it will. Samsung seems to be doing well so far.”

“The cold, hard reality is that shortages are a fact of life in semiconductors, as are horrific gluts.”

“What we are flippantly labeling as TSMC we really mean is the AI supply chain. And that supply chain is as complicated as you can possibly imagine. Like an iceberg, it looks big enough on the surface of the water, but goes way far deeper underneath. TSMC has thousands of suppliers in two categories: Equipment like the famed ASML lithography tools and materials like photoresist, silicon wafers, acid etch gases and so on. These are not generalized tools and materials. They are not fungeible like AWS compute units.”

“And then there are the memory guys. You cannot ship an AI system without memory. DRAM and NAND. Nvidia’s AI chips use a special form of DRAM called high bandwidth memory, and they use quite a lot of it. The memory industry is just as consolidated as the logic industry, with the major players being Samsung, SK Hynix and Micron.”

“The chip guys are last to know when the party is getting started, but first they get batoned in the face when the police shut things down.”

He points out that semiconductor manufacturers have log supply chains. He uses a different metaphor (the beer distribution game, or a bullwhip), but back when I was working at Applied Materials, it was described as trains linked together with slinkys. First software takes off, then hardware gets yanked along, then the chip manufacturers get yanked, and then, finally, semiconductor equipment manufacturers get yanked into motion, and shortly after that happens, the bust hits the front of the train, and the trailing cars all crash into each other. It’s a regular boom/bust cycle.

“From 1961 to 2006, electronics consumption in the United States grew positively but with wild volatility swings between 0 to 20%. But for the semiconductor makers, that translates to swings anywhere from 20% to 40%. And for the equipment makers, it is amplified even more, plus or minus 60%. The whip hits particularly hard in the semiconductor industry because of the industry’s long lead times. It takes 4.5 months to fabricate and package a chip. It takes 18 months to 2 years to build a fab. Meaning from shovels down to producing chips, and it takes 12 to 18 months to produce and install something like an EUV machine into the fab. Another 6 months before that machine actually starts patterning wafers.”

“Long lead times mean having to make very long demand forecasts, which leads to extreme volatility swings during up and downturns even if those up or downturns are relatively small.” People forget that in 1998, during the time we now think of as the DotCom Boom, there was a small semiconductor downturn that had Applied Materials forcing employees to take unpaid leave.

“ASML just reported 2025 earnings, and we see the bullwhip in full effect. TSMC raised capital expenditure 35% but ASML announced €13.2 billion of net new bookings. Analysts had expected just €6.32 billion. This is because ASML collected orders not just from TSMC, but also Samsung, Intel and the memory guys. When it rains it pours, right? Again, this is why I fear that another AI foundry would not mean our compute shortage is solved, because ultimately, when those foundries start scaling their capacity, they all go to the same suppliers.”

He goes over how car manufacturers cancelled orders during Flu Manchu, and then scrambled when the economy took off afterwards. “TSMC was trying to discern between double booked orders and real demand, which is not an uncommon experience for them. Customers lie about their own demand all the time, or at least we can say that they are eternally optimistic. TSMC tried to respond in 2022. The Taiwanese giant poured $36 billion into capital expenditure. They went to their suppliers and pushed like no tomorrow.”

“It turned out those customers really were double booking orders and artificially inflating demand. When the macro environment turned in 2022, the automotive, smartphone, and PC chips that were so hot during the COVID era fell out of vogue and customers started cutting orders.”

“Meanwhile, deeper down in the supply chain, TSMC and the rest of the semiconductor industry were getting bullwhipped by COVID hangover. Utilization at TSMC’s multi-billion dollar N7 fabs crashed, Semi analysis wrote in April 2023. Now, Semi analysis data indicates that the 7nm utilization rates were below 70% in Q1. Furthermore, Q2 gets even worse with 7nm utilization rates falling to below 60%. This is primarily due to weakness in both smartphones and PCs, but there is a broader weakness in most segments. A fab’s break even utilization rates are about 60% to 70%. So those N7 Taichung fabs were taking financial losses potentially on the order of hundreds of millions, maybe even billions. The financial burdens of low utilization are another reason why I’m skeptical another AI foundry could have rushed into the AI chip fray to save the day.”

He says that Intel incurred losses during this period due to an unnecessary fab expansion, which is probably true, but that was a secondary factor next to their longer running problem of getting their process wrong.

“ChatGPT was released in November 2022, and that kicked off a massive increase in capex amongst the hyperscalers in particular, but it sure seems like TSMC didn’t buy the hype. That lack of increased investment earlier this decade is why there is a shortage today and is why TSMC has been a de facto break on the AI buildout/bubble.”

“I recall news in mid 2024 of TSMC struggling with CoWoS capacity bottlenecks and yield problems, including one design issue that caused cracks in the Nvidia chips packaging.” CoWoS is Chip on Wafer on Substrate, which involves fabbing an interposer as a substrate for faster connections between your processing chips and memory.

“I also recall news in late 2024 noting how the vendors in charge of making the server racks for Nvidia’s Blackwell servers struggled with overheating, liquid cooling leaks, software bugs, and connectivity issues. Such technical difficulties delayed server deployment until early to mid 2025, creating a weird situation for several months where TSMC was pumping out chips that just went into storage. So that gated things, because you don’t scale until you first fix the technical problems.”

Then there’s the power-scaling issue, which is a whole ‘nuther can of worms.

There’s a lot of talk about a SaaSpocalypse going on thanks to a new AI tool. (SaaS is “Software as a Service.” Instead of hosting your own payroll or sales-tracking or whatever servers, you hire a company that already has cloud software setup to do it and you just tie into that, which can considerably reduce startup costs. A whole lot of successful new tech companies over the last decade plus have been SaaS companies.)

The software sector was jolted overnight with what analysts are calling a “SaaSpocalypse” — a sudden and severe selloff triggered by new artificial intelligence tools unveiled by US AI startup Anthropic. The episode has sharpened investor fears that AI is no longer merely helping software companies but may now begin replacing them.

Anthropic has expanded its enterprise AI platform, Claude Cowork, by launching 11 new plugins aimed at automating a wide range of professional tasks. Claude Cowork is an agentic, no-code AI assistant built for corporate users, allowing companies to automate workflows without writing software. The new plugins are designed to handle tasks across legal, sales, marketing and data analysis functions. The most recent addition is Anthropic’s Claude Legal agent, which can perform routine legal work such as document and contract review, and compliance checks.

Anthropic has said that the tool does not provide legal advice and that all AI-generated outputs must be reviewed by licensed attorneys. Even so, the breadth of automation signals a step change in how much white-collar work AI systems can now perform.

Productivity — Manage tasks, calendars, daily workflows, and personal context

Enterprise search — Find information across your company’s tools and docs

Plugin Create/Customize — Create and customize new plugins from scratch

Sales — Research prospects, prep deals, and follow your sales process

Finance — Analyze financials, build models, and track key metrics

Data — Query, visualize, and interpret datasets

Legal — Review documents, flag risks, and track compliance

Marketing — Draft content, plan campaigns, and manage launches

Customer support — Triage issues, draft responses, and surface solutions

Product management — Write specs, prioritize roadmaps, and track progress

Biology research — Search literature, analyze results, and plan experiments

A lot of those are already automated elsewhere, but I suspect a lot accountants and paralegals just felt a goose strut across their grave. On the other hand, who is really going to turn over, say, Accounts Payable to an AI? One glitch, and your entire bank account is drained…

If it works (a big if, give so many AIs are prone to hallucinations), this is potentially good news for Anthropic and the companies using their tools, and bad for SaaS companies and the employees currently doing those jobs.

I note there’s no plugin for technical writing…yet.

And Google Cloud ended 2025 at an annual run rate of over $70 billion, representing a wide breadth of customers, driven by demand for AI products.

We’re seeing our AI investments and infrastructure drive revenue and growth across the board. To meet customer demand and capitalize on the growing opportunities we have ahead of us, our 2026 CapEx investments are anticipated to be in the range of $175 to $185 billion.”

Remember how Nvidia was going to invest $100 billion in OpenAI? Yeah, not so much.

In September 2025, Nvidia and OpenAI announced a letter of intent for Nvidia to invest up to $100 billion in OpenAI’s AI infrastructure. At the time, the companies said they expected to finalize details “in the coming weeks.” Five months later, no deal has closed, Nvidia’s CEO now says the $100 billion figure was “never a commitment,” and Reuters reports that OpenAI has been quietly seeking alternatives to Nvidia chips since last year.

Reuters also wrote that OpenAI is unsatisfied with the speed of some Nvidia chips for inference tasks, citing eight sources familiar with the matter. Inference is the process by which a trained AI model generates responses to user queries. According to the report, the issue became apparent in OpenAI’s Codex, an AI code-generation tool. OpenAI staff reportedly attributed some of Codex’s performance limitations to Nvidia’s GPU-based hardware.

After the Reuters story published and Nvidia’s stock price took a dive, Nvidia and OpenAI have tried to smooth things over publicly. OpenAI CEO Sam Altman posted on X: “We love working with NVIDIA and they make the best AI chips in the world. We hope to be a gigantic customer for a very long time. I don’t get where all this insanity is coming from.”

Microsoft’s Copilot chatbot has become central to its artificial-intelligence strategy as the company’s close partnership with OpenAI diminishes. But the effort to build it up as a ChatGPT alternative has been tough going.

Confusing brand positioning and interoperability problems have frustrated users, current and former employees who have worked on Microsoft’s AI products said.

Interoperability problems? With a Microsoft product?

Only a small proportion of subscribers to Microsoft’s enterprise suite use Copilot, and the percentage who favor it over Google’s Gemini or other tools has decreased in recent months, according to data reviewed by the Journal.

The stakes are high for Microsoft because Copilot is core to a push by Chief Executive Satya Nadella to transform Microsoft into an AI-first company, much as he transformed it into a cloud-first company around a decade ago. Copilot is one of Nadella’s top priorities, current and former executives said.

Microsoft shares tumbled after its earnings report last week sparked investor concern that growth in its most important unit, the Azure cloud-computing business, is slowing, and that its AI business is reliant on OpenAI while Copilot remains unproven. Shares fell nearly 3% Tuesday amid a slide in software stocks prompted by fresh concerns that AI tools will make enterprise subscriptions less necessary.

For other AI companies, we merely suspect they’re evil. For Microsoft (and Google), we already know they’re evil…

Good news for the central Texas economy: Samsung’s new Taylor fab is going to build AI chips for Telsa.

Tesla’s next-generation AI6 chip, designed to power the Full Self-Driving (FSD) system, will be manufactured at Samsung’s new, massive chip fabrication plant in Texas, strategically located near Tesla’s Model Y and Cybertruck production facilities.

They’re both on the outskirts of east Austin, though different parts of east Austin (Telsa’s plant is south, and Samsung’s new Taylor fab way north). Google maps say they’re about 27 miles apart as the crow flies, or 36 minutes apart if you take the 130 toll road.

“Samsung’s giant new Texas fab will be dedicated to making Tesla’s next-generation AI6 chip. The strategic importance of this is hard to overstate,” Elon Musk wrote on X late Sunday night.

Musk continued, “Samsung currently makes AI4. TSMC will make AI5, which just finished design, initially in Taiwan and then Arizona.”

“Samsung agreed to allow Tesla to assist in maximizing manufacturing efficiency,” he noted, adding, “This is a critical point, as I will walk the line personally to accelerate the pace of progress. And the fab is conveniently located not far from my house.”

As to Musk “personally walking the line to accelerate the pace of progress,” presumably in a full bunny suit, I fail to see how that’s going to help anything. Most modern fabs have extremely efficient, streamlined operations that aren’t amenable to improvement via random billionaires walking their floor.

Samsung confirmed that it will produce Tesla’s AI chips as part of a $16.5 billion chipmaking deal, marking a major win for its underperforming foundry division, according to Bloomberg.

A foundry is a fab that manufactures chips for other companies rather than it’s own designs. Samsung has both fabs for its own chips and a foundry business.

The AI6 chip will be produced at Samsung’s chip plant in Taylor, Texas. The new facility was partially funded through the Biden-Harris administration’s CHIPS and Science Act and is focused on manufacturing advanced logic chips for mobile devices, 5G, high-performance computing, and AI applications.

My previous critique of the CHIPS act can be found here.

Tesla’s partner in the deal, Samsung’s Taylor Fab semiconductor location — which broke ground in 2022 and is expected to be fully operational in the City of Taylor come 2026 — aims to increase the production of semiconductor-related initiatives that’ll “power next-generation technologies” including 5G, high-performance computing, and various forms of AI.

The South Korean company, Samsung Technologies, first planted its roots in Texas in 1996, in Austin.

Tesla has multiple locations across the Lone Star State, including its primary manufacturing hub and headquarters near Austin, the “Gigafactory,” which boasts over 10 million square feet in floor space or 2,500 acres.

Snip.

Samsung Electronics announced on Monday it had signed a $16.5 billion contract with a “large global company” — revealed by Musk in the aforementioned X posts, although kept anonymous by Samsung. The contract’s tenure spans from July 24, 2025 to December 31, 2033.

Musk clarified in another X post that he believes the $16.5 billion number is “just the bare minimum,” and that the “actual output” of this collaboration between Samsung and Tesla will be “several times higher.”

There’s been a lot of (somewhat justified) concern over the dependence of American tech companies like Nvidia and Apple on Taiwan-based TSMC to fab their cutting edge sub-10nm chip designs. The problem has been foolishly phrased as “America can’t make chips anymore,” which is false, as American fabs churn out millions of chips every month. The problem is “lack of available domestic sub-10nm wafer starts,” a problem exacerbated by the fact that there are only three companies in the world that have the knowledge and resources to building cutting edge fabs, the cost of which is now pushing $20 billion.

Fortunately for Texas, Samsung is one of those three companies, and together with TSMC’s new fab in Arizona and Intel’s new fab in Ohio, a lot of those capacity constraint problems are being addressed.

President Trump announced his tariffs on countries, especially those that tariff goods from the United States.

President Donald Trump on Wednesday imposed sweeping new tariffs on all imported goods and unveiled a detailed list of reciprocal duties targeting more than 60 countries, asserting that the move is necessary to combat trade imbalances and restore U.S. manufacturing.

“This is Liberation Day,” Trump said during a Rose Garden ceremony, holding up a printed chart of countries and their new tariff rates. “For decades, our country has been looted, pillaged, raped and plundered by nations near and far, both friend and foe alike.”

The tariffs, which he described as “reciprocal,” fulfill a key campaign pledge and are aimed at pressuring trade partners to lower their own barriers. The administration expects the new rates to remain in place until the U.S. narrows a $1.2 trillion trade imbalance recorded last year.

But the extensive list of tariffs also threatens to upend the U.S. economy, as many — but not all — economists say they amount to taxes on American companies that will be passed down to consumers.

Trump held up a chart while speaking at the White House, showing the United States would charge a 34 percent tax on imports from China, a 20 percent tax on imports from the European Union, 25 percent on South Korea, 24 percent on Japan and 32 percent on Taiwan.

The centerpiece of the announcement is a 10 percent universal baseline tariff on all imports, effective immediately. For instance, Chinese imports are now subject to cascading tariffs of 10, 20 and 34 percent, for a total of 54 percent.

In addition, Trump’s administration imposed country-specific reciprocal tariffs on nations it accuses of unfair trade practices — including India, Vietnam, and the European Union, in adding to China. The rates are calibrated at approximately half the rate those countries impose on U.S. goods.

For example, China, which Trump said charges 67 percent in tariffs on U.S. goods when factoring in non-tariff barriers, will now face a 34 percent reciprocal tariff under the new system, in addition to the 10 percent baseline tariff and the 20 percent tariffs already in effect. Vietnam, assessed at 90 percent, will face a 46 percent tariff; India at 52 percent will now see 26 percent duties; and the EU, which imposes 39 percent, will be met with a 20 percent response, according to the White House chart.

This is a “devil in the details” issue that has a lot of ramifications depending on how the directives are written. But several of those countries are big players in semiconductors, so here’s a quick and dirty look at winners and losers if those tariffs stay in place a significant amount of time.

The main countries here, along with the reciprocal tariffs being applied to them:

Taiwan (32%)

South Korea (25%)

China (34%)

European Union (not a country, but they play one on TV) (20%)

Japan (24%)

Singapore (10%)

Israel (17%)

Save a few smaller, older fabs here and there, that’s pretty much 99% of semiconductor manufacturing, though Vietnam (46%) and the Philippines (17%) do a lot of semiconductor package assembly work, and the tariffs may apply to them, depending on wording.

So let’s look at the business Losers and Winners in the space. (Note: You might find this post useful, as it defines some of the semiconductor industry terms used here.)

Losers

TSMC: As the world’s biggest and most important chip foundry, the Taiwanese tariffs will hit TSMC hard. Their U.S. fab in Arizona isn’t ready for production yet, so all their chips will (theoretically) get hit with tariffs, assuming Trump doesn’t grant them a waiver because they’re already constructing a plant. But if they do go into effect, possibly even more heavily impacted will be:

TSMC customers, including Apple, Nvidia and AMD. All three get their very highest-end, cutting edge, sub-10nm chips fabbed there. For Apple, the M-series and A-series chips made there form the heart of all their Macs and iPhones. Likewise, Nvidia gets its highest end GPU/AI/etc. chips fabbed by TSMC. AMD’s most powerful CPU’s are also fabbed by TSMC, though some lower end chips are made elsewhere (like GlobalFoundries).

Tokyo Electron: Japan’s biggest semiconductor equipment manufacturer assembles pretty much all their equipment in their home country. 24% tariffs may make their equipment uneconomical compared to rivals Applied Materials and LAM Research.

South Korean DRAM manufacturers Samsung and SK Hynix: 25% tariffs will definitely impact sales in a market segment whose overall margins (robust in booms, and barely breaking even during busts) are thinner than others.

Every American electronics company that uses DRAM. Which is pretty much every American electronics company.

Every American AI boom company. Their data center costs are going up, while those of their foreign competitors are not.

Korean flat panel display manufacturers Samsung and LG Semicon, who between them control over 50% of the market.

Every American TV and monitor manufacturer, the vast majority of which have their devices manufactured overseas.

UMC: They’d fallen woefully behind TSMC for foundry work, and they won’t be winning much additional American business now.

Every company trying to build a sub-10nm fab in the U.S., as steppers from Netherlands-based ASML just got more expensive and the competition to obtain them might have increased.

Pretty much every fab in China just got more screwed…but they were pretty screwed (and trailing badly) before.

American fabless chip startups: Their costs for getting chips to market probably increased.

Winners

Applied Materials, LAM Research and KLA Tencor. Buying competing Tokyo Electron equipment just got more expensive, and a bunch of companies now have incentives to build fabs in America.

Intel: Assuming they’ve finally got their process technology sorted out (a big if), they’re well-positioned to take CPU market share from AMD and to grow their under-performing foundry business.

Micron (sort of): As the only American DRAM manufacturer, they can probably earn more per each chip produced domestically. But Micron has a lot of overseas fabs these days, and building new domestic DRAM fabs will take years.

GlobalFoundries: The costs of their global competitors just increased, so they can probably win more business for their domestic foundries…if they have the available wafer starts. But they have a lot of foreign fabs as well.

Samsung‘s US foundry business. Presumably the wafer starts for their Austin and Taylor fabs will see increased demand.

Maybe Texas Instruments, but I’m not sure how much mixed-signal and analog competition they have, and that’s their bread and butter.

Neutral

ASML: Being in the Netherlands and having TSMC as their biggest customer, you figure they’d be hurt, but no. You can’t get EUV steppers from anyone else, and I get the impression they’re building EUV steppers as fast as they possibly can already. Anyone building a cutting-edge fab will just have to pay more to get them.

Tower Semiconductor: Half their foundries are in Israel and half in the U.S., so I figure it’s a wash.

That’s my quick and dirty analysis. Of course, Trump is using tariffs like a battering ram to smash foreign tariffs, and if he’s immediately successful, there probably will only be minor hiccups in the global supply chain. But if not, a whole lot of disruption might lie ahead, and it usually takes a minimum of 3-5 years to bring a new fab online.

I know that any time I talk about semiconductors, a significant percentage of my readership’s eyes glaze over, but this is Big Freaking News.

Intel shares rose 6% in premarket trading after Reuters reported that Taiwan Semiconductor Manufacturing, or TSMC, had approached US chip designers Nvidia, Advanced Micro Devices, and Broadcom about taking stakes in a joint venture that would operate the struggling chipmaker’s factories.

Four sources told Reuters that the Taiwanese chipmaking giant would run Intel’s foundry division under the new proposal, producing chips tailored to customer requirements but not owning more than 50%. The sources added that Qualcomm has also been approached about the venture.

TSMC is far and away the largest chip foundry (a company that builds chips for other companies, but doesn’t design its own chips) in the world, and the one with a clear technological lead over everyone else. TSMC has the third largest market cap of any semiconductor company.

Broadcom is the second-largest semiconductor company in the world by market cap, and they have their fingers in a lot of different pies: networking, wireless, storage, you name it. They’re generally considered a fabless chip designer, but the company is such a weird amalgamation of other companies (what we call Broadcom used to be Avago until they acquired Broadcom in 2016) that they might still have a lower end fab or two lurking somewhere in the company. They also use TSMC as a foundry, though I’m not sure how extensively. They’ve also recently made a big move into software, acquiring CA Associates and VMWare, among others.

Nvidia is a fabless chip designer (the sort of company that contracts with foundries to fab their chips) that went heavily into high end GPUs (the chips that render video for your PC, in Nvidia’s case geared toward high end games and other highly demanding tasks), then crypto-mining chips, and more recently into chips geared for AI applications, all very lucrative market segments, which has made Nvidia not only first among semiconductor market cap, but among the largest companies by market cap in the world (along with Apple and Microsoft). Nvidia has their chips fabricated by TSMC, as well as some by Samsung and GlobalFoundries, which was spun off from…

Advanced Micro Devices, which used to be an Integrated Device Manufacturer (or IDM, a company designs their own chips and builds them in their own fabs) creating Intel-compatible CPUs, but eventually spun off their fabrication plants as GlobalFoundries because they couldn’t keep up with Intel’s capital spending. AMD also has some of their highest end chips fabricated by TSMC. If AMD were to help take over Intel, it would be an extremely ironic ending to a longtime rivalry.

Qualcomm is a lot like Broadcom: A mostly fabless design house with its fingers in lots of different pies, and they’re about the sixth largest semiconductor company by market cap. Broadcom tried to acquire Qualcomm in 2017-18 and was blocked by the Trump45 administration.

Intel is an IDM, and for decades was the undisputed “chipzilla” of the semiconductor world. Intel’s CPUs were the dominant processor for the vast majority of the last 40 years and a huge ingredient for helping create the PC revolution. Intel used to be the technology process leader as well, but somewhere along the way they screwed up their sub-10nm process nodes, allowing TSMC to take the process technology crown. Indeed, they screwed up so badly that they’ve been forced to have TSMC fab some of its highest end chips. Despite having a vast number of fabs, Intel’s market cap has slipped down to 16th among semiconductor companies.

Back to the piece:

The sources noted that the Trump administration is exploring ways to revive Intel and strengthen US manufacturing under the ‘America First’ agenda. They added that TSMC’s joint venture pitch to chip designers took place before the company, alongside President Trump, announced plans last month to invest $100 billion in semiconductor manufacturing in the US, building on its existing $65 billion investment in its Phoenix, Arizona, factories.

Any deal between TSMC and Intel would be subjected to approval from the Trump administration.

If the Trump Administration’s goal is to increase available sub-10nm wafer starts (and it should be) and maintain American control of Intel’s fabs, then this proposal is a win-win. Intel’s fabs plus TSMC’s tech would create a foundry powerhouse. It wouldn’t happen overnight (nothing in semiconductors happens overnight), but probably in 12-24 months, depending on how quickly the new entity can acquire the necessary pieces of equipment to upgrade Intel’s fabs to thee new tech (I’m guessing that the availability of ASML steppers will, as usual, be the gating factor). And all this without the tens of billions in taxpayer subsidies for the CHIPS Act.

If this goes through, it would have mostly winners, with a few losers:

Winners

Every company that’s part of the deal. TSMC gets to radically expand production capacity without spending $20 billion+ to build a new fab. Nvidia, AMD, Broadcom and Qualcomm gain a lot more capacity for expanding production of their high end chips. Ditto for Apple (who’s not part of the deal, but who is TSMC’s biggest customer and a big demand driver for cutting edge fab capacity) and every other consumer of sub-10nm chips.

AMD additionally gets the egoboo of partially taking over its longtime hated rival and confirming it’s crown as the x86/x64 chip manufacturer of choice. Plus their then-risky decision to spin off GlobalFoundries looks like a genius move in hindsight.

The Trump Administration, which gets to take credit for vastly increasing American Foundry capacity at zero additional taxpayer expense and keeps Intel under American control.

Semiconductor equipment manufacturers like ASML, Applied Materials, LAM Research, Tokyo Electron and KLA (short term). It’s likely most or all of those companies (along with smaller players like Axcelis and Teradyne) will receive a bump in extra sales from leveling up Intel’s fabs to run TSMC’s process.

American chip startups: With so much high end capacity becoming available, existing and potential chip startups are going to look like more attractive investment capital opportunities.

ARM Holdings: ARM doesn’t make chips, they’re an IP design house that licenses their functional chip blocks to other chip designers. Just about every foundry and IDM is a licensee (yes, including Intel and TSMC), so unleashing more chip designs will almost certainly result in more royalties for ARM. (Nvidia tried to buy ARM in 2020, and regulators quashed that idea good and hard.)

Intel investors, who will either get a big lump-sum payment or shares in the new, probably far more profitable company (depending on how the buyout is structured).

Even Intel wins long-term by unleashing existing fab capacity to take on new business not tied to its faltering CPU manufacturing model. And actually, with TSMC’s process, Intel has a chance to recover in the CPU space as well.

Losers

Samsung: Along with TSMC and Intel, Samsung (which has both IDM and foundry components) has some of the best sub-10nm process tech in the world. They gain a whole lot of unleashed competition and stand on the outside looking in.

Intel‘s dreams of reclaiming their spot at the top of the heap, and suffering the indignity of being partially owned by AMD. How the mighty have fallen.

Every Chinese fab, which goes from “very far behind” to “even further behind.”

Semiconductor equipment manufacturers (long term): They better enjoy the out-of-band upgrade money from retrofitting Intel’s fabs, as it will likely mean a significant delay in anyone building a new cutting edge wafer fab for quite a while. And having two of their biggest customers team up is probably going to put them under a lot of downward pricing pressure.

GlobalFoundries (and other trailing edge foundries) might lose some business, but there’s very little overlap between Intel/TSMC cutting edge processes and GlobalFoundries trailing-edge fabs. Ditto UMC.

Are there anti-trust concerns with such a heavy accumulation of cutting edge process technology? Oh yeah. Big time. But almost all of those concerns were already there in some form or another thanks to the interconnected “cooperation” nature of the industry. All those companies going in with TSMC were already getting chips fabbed by TSMC. Samsung could try to claim that the deal would result in TSMC having a de-facto monopoly on sub-10nm foundry business, but it wouldn’t start with one, and that business isn’t the whole of foundry business (though it is the most profitable part), much less semiconductors as a whole.

Given that this would go a long way toward achieving Trump’s goal of increasing cutting edge fab capacity in America, I would imagine that the Trump47 administration could very well be persuaded to let this deal go through.

What a freaking epic (and tiring) week! I waited until Fox and Decision Desk had declared Trump the winner past 1 AM Wednesday morning, and then had to get up a few hours later to get ready to work. So we’ve got more election fallout, Israel bags more terrorist scumbags, Elon Musk and Ron Paul may team up to fight government waste, Texas continues to purge wokeness from public institutions, and a song mystery is solved.

Last time around, Trump squandered his momentum. He passed the tax bill that the establishment GOP wanted, after which they didn’t need anything from him and turned to obstructing him….

Like airplanes on a runway. Trump’s approach this time around should be what he should have done last time: Shock and awe. Shut down departments, fire bureaucrats, exercise emergency powers, all so fast that the establishment’s responses are saturated. Javier Millei’s whirlwind assault in Argentina should be the model, sometimes in specifics but also in general approach. Bureaucrats move slowly; Trump should move fast.

Elon Musk says he can cut $2 trillion easily; do it. Also, set bureaucrats competing with each other for what funds remain. Divide and conquer.

The FBI’s files on its policing of domestic dissent should be opened up, as should the details of the NSA’s illegal domestic spying. Trump should have outsiders investigate possible (likely) prosecutorial misconduct in the January 6 prosecutions – something judges have already raised – and fire those responsible, as well as subjecting them to what other legal consequences may apply. The lesson that the deep state can’t intervene in domestic politics needs to be driven home, and the only way to do that is to ruin a lot of lives on the part of people who deserve to have their lives ruined, from the top of the Justice Department and the intelligence agencies to the bottom. Likewise those involved in social media censorship programs, “Operation Chokepoint” style economic warfare, and the like. Abuse of government power against the citizenry should be treated as a criminal matter, because it is.

Trump should also announce that the federal government is waiving qualified immunity on the part of such officials.

There are lots more ideas – you can submit your own in the comments below, and the much-maligned Project 2025, though not actually a Trump initiative, contains some – and Bloomberg is already warning that if elected Trump will dismantle the White House’s gun control ministry. Oh no!

The specifics aren’t really the point here, though I should probably post another essay just about those. But the point here is rapid action across a wide variety of fronts. Trump should take advantage of the precedents that Biden has set for far-reaching executive action, though you can bet that when he does the press will pretend this is the first time anything like that has ever been done.

The story of how Harris pocketed record sums while failing to gain support from voters will be studied by campaigns for decades to come. Democrats who successfully pressured octogenarian President Joe Biden to pass the torch to the former California senator are now conducting an internal autopsy of the 2024 race, in which Trump raised and spent hundreds of millions of dollars less than Harris.

“A billion dollars paled in comparison to the increased prices Americans were seeing across the country,” Tom Fitton, president of the conservative group Judicial Watch and a longtime Trump ally, told the Washington Examiner. “Voters weren’t fooled.”

The Harris campaign and its affiliated committees dropped more than $654 million on advertising from July 22 to Election Day, whereas Trump spent $378 million, or 57% less, in the same category, according to data from AdImpact.

Future Forward, the $500 million “ad-testing factory” and super PAC that supported Harris, was a reliable clearinghouse for checks from wealthy Democrats such as Reid Hoffman, George Soros, Michael Bloomberg, and Dustin Moskovitz. And anonymous donations, or so-called “dark money,” also benefited Harris at a faster and more substantial clip than Trump thanks to lax federal laws that progressives often criticize but, nonetheless, exploited in 2024.

The Harris campaign declined to comment on its finances. A fuller portrait will be public after the election, as the Federal Election Commission mandates post-general election reports for candidates within 30 days.

In mid-October, the Harris campaign disclosed that it had spent over $880 million this election, almost $526 million greater than the roughly $354 million that the Trump campaign had disclosed spending, according to a Washington Examiner analysis of federal filings. Much of the Harris campaign’s spending was allocated for digital media advertising, polling, and travel from state to state, including to a private jet company called Advanced Aviation.

Payroll and the taxes that accompanied it accounted for $56.6 million of the Harris campaign’s spending. In comparison, the Trump campaign reported spending $9 million on payroll — employing hundreds fewer staff members.

There was also the army of political, digital, and media consultants who were paid over $12.8 million by the Harris campaign, filings show.

One vendor, Village Marketing Agency, received over $3.9 million and reportedly worked to recruit thousands of social media influencers to boost Harris online. Others that scored lucrative consulting gigs from the campaign included the likes of Precision Strategies, a Democratic-aligned marketing agency; Ethos Organizing, founded by former Ohio Democratic Party director Malik Hubbard; and the Biden-allied SKDK communications firm.

Snip.

“Event production” was also a staple spending area of the Harris campaign, which notably hosted a star-studded lineup of musicians from Lady Gaga to Katy Perry for an election eve rally.

The campaign paid more than $15 million, according to federal filings, to companies for such services.

There was $1 million for Oprah Winfrey’s Harpo Productions on Oct. 15 in West Hollywood, California.

Winfrey, a top Harris ally, appeared at a town hall with the vice president in September and was at her final rally in Philadelphia before Election Day.

Viva Creative, a marketing agency that has touted its work with Oprah, comedian Trevor Noah, the Washington Nationals baseball team, and American Express, scooped up $1.8 million from the Harris campaign for event production from September to October. A company called Production Management One in Maryland received $1.7 million, with large payments also going to Vox Productions, Temple University, Wizard Studios North, the Park Hyatt Chicago, and other entities for event production, filings show.

Then there was Majic Productions, a Wisconsin-based company, which has worked the NBA playoffs, the Super Bowl, and at the Bellagio Hotel & Casino in Las Vegas. The Harris campaign paid that company $2.3 million.

A source familiar with the matter told the Washington Examiner that the Harris campaign spent six figures on building a set for Harris’s appearance on the popular Call Her Daddy podcast with host Alex Cooper. The interview came out in October and was reportedly filmed in a hotel room in Washington, D.C.

In the end, San Francisco mayor London Breed’s recent efforts to crack down on homelessness and crime weren’t enough to save her from the wrath of voters frustrated by years of disorder and talk of a “doom loop” in the famously progressive city.

After 14 rounds through the city’s ranked-choice voting process, Breed lost decisively to Daniel Lurie, a more moderate Democrat and a wealthy heir to the Levi Strauss fortune.

Lurie was ahead from the first round, and after 14 rounds led with 56.2 percent of the vote to Breed’s 43.8 percent, according to the San Francisco Department of Elections.

With San Francisco actually restoring sanity, pretty soon Austin will be the only crazy leftwing city left in America…

“UK Conservative Party elects ‘anti-woke’ Kemi Badenoch as new leader. The UK’s Conservatives on Saturday elected Kemi Badenoch as their new leader, replacing Rishi Sunak after the party’s poor performance in July’s general election. Badenoch, a staunch “anti-woke” advocate, faces the challenge of uniting a divided party while redefining its future.”

Israel seems to be on another winning streak. Israeli Commando Raid Captures Hezbollah Naval Commander….The terrorist, identified by Lebanese media as Imad Amhaz, chief of Hezbollah’s naval operations, was picked by Israeli commandos from the town of Batroun, some 100 miles into the terrorist-held hostile territory.”

Today, the Board of Regents of Texas A&M University System pushed back against “shared governance” with woke faculty members. They voted to end 52 low-performing programs, including an LGBTQ minor.

Over the course of many months, State Rep. Brian Harrison (R-Midlothian) repeatedly criticized DEI courses and the LGBTQ studies minor at Texas A&M. In September 2024, a university spokesperson confirmed that they would deactivate 38 certificates and 14 minors, including the Lesbian, Gay, Bisexual, Transgender, and Queer Studies minor.

On November 7, the Board of Regents unanimously approved the deactivation of these programs by voice vote.

The only question is why it took so long to fight back against the woke mind virus…

Want to be infuriated? “A federal disaster relief official ordered workers to bypass the homes of Donald Trump’s supporters as they surveyed damage caused by Hurricane Milton in Florida, according to internal correspondence obtained by The Daily Wire and confirmed by multiple federal employees.”

“The Grift Is Ending: ESG Fund Managers Being Told To “Keep Their Lawyers Very Close.”

Green New Boom: “Lithium-Ion Battery Recycle Plant Explodes in Missouri.”

RIPeanut. “Outrage Ensues After Beloved Rescue Squirrel Seized By NY, Euthanized.”

Speaking of sickening, you might want to skip to the next LinkSwarm entry if you don’t want to hear about horrific child abuse: “Animator Bolhem Bouchiba was sentenced to 25 years in prison for ordering the torture of children on live streams, paying parents to abuse their own kids.” Now he works for Disney.

Remember all that money to was supposed to flow to semiconductor companies that fabbed chips in America thanks to the CHIPS Act? Well Intel has seen exactly jack and squat from it. Intel CEO Pat Gelsinger: “As we said on our [earnings] call, we are disappointed by the time it is taking to get it done: it is well over two years since the CHIPS Act passed and over that period I have invested $30 billion in U.S. manufacturing and we have seen $0 from the CHIPS grants.” What are the odds that the money has actually been raked off into the usual Democratic pockets? (Hat tip: Ace of Spades HQ.)

Followup: “For five years, Mickey Barreto lived in Room 2565 at the storied New Yorker Hotel without paying a dime. But the free ride ended when he was not only evicted, but also charged earlier this year with a criminal scheme to claim ownership of the Midtown Manhattan hotel. Now, two doctors and prosecutors have said that he is not mentally competent to stand trial, and a judge has given him seven days to find inpatient psychiatric care.” (Hat tip: Dwight.) (Previously.)

Kotaku lays off more writers, though ultra-woke leftist Alyssa Mercante evidently left on her own. Evidently they’re down to six fulltime staffers.

Everything you know is wrong. “A new peer-reviewed study led by Sydney-based researchers Stephen Woodcock and Jay Falleti has found that the time it would take for a typing monkey to replicate Shakespeare’s plays, sonnets, and poems would be longer than the lifespan of our universe.”

“Democrats Admit Trump Actually Won In 2020 And Is Now Unable To Serve Third Term.” “We probably should have been more up-front about the fact that we stole the election and Biden was never president, but oh well. Hindsight is 20-20. I guess Kamala wins by default now, right?”