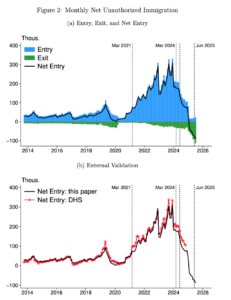

As I’ve stated before, Biden importing several million illegal aliens across the southern border raised housing prices, because increasing demand without increasing supply raises prices.

A working paper from the Federal Reserve Bank of Dallas concluded that the large influx of illegal aliens during the Biden administration drove up housing prices and rents.

According to the paper, roughly 7 million people illegally came to the United States between 2021 and 2024.

This spike of illegal immigration “raised local house prices and rents without expanding housing supply,” acting as a “demand shock to local housing markets.”

Using court records and border enforcement information alongside housing market data, the economists estimated that illegal immigration “can explain about 30% of the total growth in house prices and 20% of total growth in rents over the boom period for the average local market.”

“We’ve actually been saying this for a number of months now,” U.S. Rep. Beth Van Duyne (R–Irving) told CBS News. “I don’t think people sometimes understand the ramifications of having so many folks enter your country illegally in such a short period of time and the financial disaster that it causes.”

Although housing costs have begun to ease, prospective homeowners continue to face affordability challenges. The National Association of Home Builders calculated that in Texas, a $1,000 median price increase would price out roughly 15,000 households.

John Bonura and Selene Rodriguez from the Texas Public Policy Foundation are urging lawmakers to “ensure that scarce housing opportunities first serve the people to whom this country ultimately owes its highest obligation.”

You mean citizens rather than illegal aliens? Seems like the Democrats have those priorities reversed.

The paper can be found here, in which we find this breathtaking chart showing the effects of the Biden Administration’s deliberate attempt to leave the southern border unsecured:

Republicans need to drop direct mailers to everyone under the age of 30 this year, explaining that Biden’s illegal alien wave drove up housing prices, and that excessive regulation in blue cities and states restrict demand. Who knows, this little nugget of truth may even give some of them a clue as to why socialism doesn’t work…

Conflicting economic signals, more Democrat fraud uncovered, more criminal illegal aliens deported, Ukraine sinks more Russian ships and ignites more Russian oil refineries, more Winning, more media companies still try to cling to woke (but Victoria’s Secret wises up), and videos that will break your brain. It’s the Friday LinkSwarm!

Personally, it’s been an eventful week. I opened an IRA to move money into from a 401K so I can move some of it to my checking, but it always takes longer than they promise. And my dog managed to catch a skunk, who seemed to spray directly into his mouth from the way he was frothing. So I bought some carpet stuff to get the second-hand Eue de Skunk out of my carpets. (From the description of other people whose dogs have been skunked, I don’t think he got much of a dose except in his mouth and on his head, so I suspect I haven’t had it as bad as some people.)

The closely watched employment report from the Labor Department on Friday painted an upbeat picture of the jobs market. The economy added 93,000 more jobs in March and April than previously estimated and the unemployment rate held at 4.3% for a third consecutive month.

But: “Tech job cuts surge, hitting a nearly two-year high. Big Tech in May announced the most job cuts in almost two years — more than 38,000 in total, according to new data from Challenger, Gray & Christmas. The tech sector has announced 123,653 cuts in 2026, a 65% increase over the same period last year.” So the economy is doing great! Except for the part of it that could hire me…

Russ Vought at OMB has just overhauled $1 TRILLION in federal grants by adding: Strict E-Verify requirements, English-language rules, and political appointee oversight to ensure taxpayer dollars go to American citizens first.

Vought’s new proposal replaces automatic payouts with “pay for performance” standards. Grants can now be terminated for waste, fraud, underperformance, or pushing anti-American priorities like DEI, gender ideology, or Green New Scam programs.

No more blank checks and fraud complaints go STRAIGHT to inspectors general and U.S. Attorney Jeanine Pirro within 10 days.

Sounds like a great start, but the fact that the federal government is handing out $1 trillion in grants seems like a problem in and of itself…

Environmental Protection Agency Administrator Lee Zeldin says he has made several criminal referrals after uncovering a major political enrichment scandal that routed billions in Biden-era green energy grants to Democrat cronies. “It’s about self-dealing,” Zeldin tells Just the News.

Zeldin said he has canceled or stopped about $29 billion in EPA grants – including one for $2 billion to a nonprofit tied to longtime Georgia Democrat election activist and failed gubernatorial candidate Stacey Abrams – after unmasking a series of pass-through groups used to route taxpayer monies to the politically connected.

“As you look through all of these pass-through entities, you’re seeing so many connections to former Obama and Biden administration officials and Democratic donors, people who were former Cabinet members, other high-ranking administration officials,” he said during a wide-ranging interview Monday on the John Solomon Reports podcast.

Zeldin: “Blatant waste and abuse.”

Zeldin said he has referred several of the transactions to the EPA inspector general, the agency’s chief watchdog, and the Justice Department for possible prosecution or further investigation. “Those referrals have been made,” he said.

Zeldin said some of the allegations have their roots in legislation like the Inflation Reduction Act, when Congress and the White House were all in Democrat hands. “They included all of this funding in this so-called Greenhouse Gas Reduction Fund. And then they would work with these different agencies of the Biden administration to get it out to their unqualified friends. The whole thing just feels criminal,” he said. “[…] This is clearly something that falls into the category of blatant waste and abuse.”

Zeldin has repeatedly singled out the Biden administration’s $2 billion grant to Power Forward Communities, a nonprofit tied to the former Democratic gubernatorial candidate Abrams. The funds were awarded in 2024 to finance “residential decarbonization,” which was an effort to replace gas furnaces and other appliances with electric ones.

Abrams reportedly “played a pivotal role” in establishing the group, according to Fox News.

The award came under scrutiny after it was revealed Power Forward Communities had reported only $100 the year before the award. The Trump administration’s EPA announced in February 2025 it was taking measures to get the money back as part of an overall effort to claw back funding rushed out the door in the final days of the Biden administration.

There doesn’t seem to be a single federal agency the Democrat Party didn’t treat as a giant bag of graft.

“SCOTUS Allows Alabama Congressional Map Likely to Net GOP House Seat. Alabama’s 2nd Congressional District, currently represented by Democratic Rep. Shomari Figures, is now widely viewed as a likely Republican pickup.”

The Supreme Court ruled 6–3 on Tuesday night that Alabama may use a congressional map drawn in 2023 for this year’s elections, reversing a lower federal court’s decision that the plan unlawfully diluted the voting power of black residents.

This ruling reduces the number of majority-black congressional districts in the state from two to one and is widely expected to give Republicans one additional House seat in the upcoming midterm elections.

“Superseding Indictment Alleges SPLC Funded ‘Ku Klux Klan garments’ and ‘Cross-Burning Events.’ Asserts wide-ranging wire and bank fraud ‘to disguise the true nature, source, ownership, and control of the fraudulently obtained donated money the SPLC paid’ to extremist group members SPLC supposedly was fighting.”

From the Introduction to the Superseding Indictment:

The Southern Poverty Law Center’s (“SPLC”) stated mission included the dismantling of white supremacy and confronting hate across the country. However, unbeknownst to donors, some of their donated money was being used to fund the leaders and organizers of racist groups, including the Ku Klux Klan, the Aryan Nations, and the National Alliance. The SPLC’s paid informants (“field sources”) engaged in the active promotion of racist groups at the same time that the SPLC was denouncing the same groups on its website. The SPLC also had a field source who was a member of the online leadership chat group that planned the 2017 “Unite the Right” event in Charlottesville, Virginia. That field source made racist postings under the supervision of the SPLC and helped coordinate transportation to the event for several attendees. In order to covertly pay its field sources, the SPLC opened bank accounts connected to a series of fictitious entities. The covert nature of the accounts allowed the SPLC to disguise the true nature, source, ownership, and control of the fraudulently obtained donated money the SPLC paid the field sources. In order to keep the scheme going, the SPLC made a series of false statements related to the operation of the accounts.

The Superseding Indictment summarizes the structure of SPLC’s alleged fraudulent operation:

10. Starting in the 1980s, the SPLC began operating a covert network of individuals who were either associated with violent extremist organizations or who had infiltrated such organizations at the SPLC’s direction. These individuals were referred to by some high-level employees within the SPLC as the “field sources” or the “Fs.” Upon entering into an agreement with an F, the SPLC assigned each F a unique number. The SPLC assigned these numbers in chronological order. The SPLC then paid the Fs with donor money.

11. Between in or about 2010 through in or about 2023, the SPLC secretly funneled approximately $4.1 million dollars in tax-exempt donor funds to a series of fictitious accounts described hereinafter. The general purpose of these fictious accounts was to pay Fs who were either leading or affiliated with multiple violent extremist organizations. Fs used the money donors gave to the SPLC to, among other things:

a. Attend extremist group rallies across the country;

b. Host extremist group rallies throughout the country;

c. Grow existing chapters of extremist groups;

d. Create new chapters of extremist groups;

e. Recruit new individuals into extremist groups;

f. Make donations to extremist group leaders;

g. Purchase materials for cross burnings;

h. Purchase materials to make Ku Klux Klan robes and hoods;

1. Create racist paraphernalia that extremist groups sold at rallies;

J. Publish extremist literature used in the recruiting of more members; and

k. Pay everyday living expenses, which allowed the Fs to focus on their extremistgroups rather than seeking other employment.

12. Certain SPLC employees knew that Fs used donors’ money to actively recruit new members and grow their violent extremist organizations.

There allegedly were fictitious entities set up to conceal what SPLC was doing:

15. To secretly funnel donors’ money to the Fs, employees at the SPLC, including a person who would become the SPLC’s Chief Financial Officer (“Employee-I”) and the person who would become Director of the SPLC’s Intelligence Project (“Employee-2”) among others, opened and/or modified a series of bank accounts at Bank-I and Bank-2 in the name of various fictitious entities, including the following:

a. Center Investigative Agency (“CIA”);

b. Fox Photography;

c. North West Technologies (“North West Tech”);

d. Tech Writers Group (“Tech Writers”);

e. Rare Books Warehouse (“Rare Books”);

f. Imagery Ink;

g. J&J Electronics;

h. Kelly ‘s Marine; and

1. Turner Personnel

16. These fictitious entities were never incorporated, had no bonafide employees, and conducted no legitimate business.

More at the link. But it certainly sounds like they were breaking a whole host of laws, including deceptive trade practices, and possibly tax fraud.

“Multiple Drone Strikes on ST-68 Radars, Pantsir SAM System and Big Logistics Hub.” There have been a lot of reports about how Ukrainian attacks are wrecking logistics well back of the front lines, and I should probably do a separate post on that when I have the time.

“Mala Tokmachka. Here, Ukrainians completely broke Russian forces who have now spent a historically long time trying to capture a tiny village.” “These repetitive assaults have been producing mounting casualties for more than four years now.” “The battle for the tiny Mala Tokmachka has turned into the longest battle in history, even exceeding the Siege of the major town of Leningrad in the Second World War, which lasted eight hundred and seventy-two days and was an important turning point and a win for the Soviets.”

“Latest ICE roundup nabs pedophiles, violent criminals. Under the Trump administration, DHS has sought to implement the president’s mass deportation agenda to remove as many as 22 million illegal aliens from the U.S.”

The Department of Homeland Security (DHS) on Monday unveiled the latest alien criminals in Immigration and Customs Enforcement (ICE) custody, which included pedophiles and persons convicted of violent crimes.

Snip.

Topping the list was Carlos Sanchez-Benitez of El Salvador, who was convicted for second-degree vehicular manslaughter.

Lauro Javier Miron-Tapia of Mexico was convicted for lewd acts with a minor child under 14 years old.

Daniel Alexis Casasola-Rivera of Mexico was convicted for a lewd act with a child under 14 years old.

Nun Hawi Tuam of Myanmar was convicted for aggravated sexual battery.

Franklin William Orellana-Maya of Honduras was convicted for sexual assault.

Yermy Hernandez-Castro of Honduras was convicted for aggravated assault with a deadly weapon.

Geovanny Gonzalez-Gonzalez of Nicaragua was convicted for aggravated assault with a deadly weapon, battery by strangulation.

Ivan Jayasi of Mexico was convicted for aggravated robbery with a deadly weapon.

Mario Zendejas-Gomez of Mexico was convicted for fourth-degree assault, obstructing law enforcement, and no contact order violation.

Miguel Sosa of Cuba was convicted for cocaine trafficking.

Oriol Mora-Arroyo of Mexico was convicted for attempted trafficking of a schedule II-controlled substance and carrying a concealed gun.

Juan Flores-Archaga of Honduras was convicted for third-degree burglary: illegal entry with intent to commit a crime.

Jhonathan Perla-Bonilla of Honduras was convicted for strongarm robbery and burglary of occupied conveyance.

Alexei Marti-Martinez of Cuba was convicted for grand theft.

Pedro Wladimir Contreras-Perez of Ecuador was convicted for larceny and licensing violation.

All of the UK seems furious over the death of Henry Nowak from stab wounds in police custody after his attacker accused his victim of being racist. “Police handcuffed Nowak, who had been stabbed by Sikh immigrant Vickrum Digwa, believing the Sikh man’s claim that Nowak had made a racist remark. Nowak told police he had been stabbed and couldn’t breathe, but officers simply left him on the ground as he lost consciousness and died.” So just like George Floyd, except Nowak was a real victim rather than a career criminal high on fentanyl.

The House Judiciary Committee said that it has uncovered new funding links between the Biden administration and left-wing groups that oppose the Israeli government, as well as groups with ties to terrorist organizations

A May 29 committee memorandum, which JNS obtained exclusively and which was addressed to committee members from the Republican-led committee staff, addresses “new information about the Biden-Harris administration helping to fund protests against the Netanyahu government.”

It alleges that U.S.-based organizations, including the Rockefeller Brothers Fund and the Tides Network, “provided over $5 million to groups that funded radical anti-Israel protests in the U.S. and Israel, and supported multiple terrorist-linked NGOs.”

Rep. Jim Jordan (R-Ohio), chairman of the committee, told JNS that the funding from the U.S. Agency for International Development, the State Department and other federal agencies raised questions about the misuse of federal dollars.

“You’re taking taxpayer money, you’re supposed to be doing good work,” the congressman said. “Why in the heck is it going to groups that are pro-Hamas?”

“Our government is sending American tax dollars to NGOs that are undermining our ally—our best ally—the State of Israel,” he told JNS. “That’s not how it’s supposed to work.”

The memo provides new details, after the committee released the initial findings of its investigation in 2025.

It describes a web of financial connections, in which the Biden administration “provided grant funds to groups that contributed directly and indirectly to the judicial reform protests that sought to undermine the Israeli government.”

“Documents suggest that the Jewish Communal Fund, and its grantees, Rockefeller Philanthropy Advisors and PEF Israel Endowment Funds, may have violated their tax-exempt status by funding groups engaged in radical anti-government campaigns in Israel,” the memo says.

“Another U.S. government grantee, Abraham Initiatives, similarly led anti-government protests in Israel and, according to a 2023 audit, the organization failed to comply with anti-terrorism procedures in a USAID-funded program,” per the memo.

Between 2016 and 2022, the Tides Network received $30 million from USAID, while Abraham Initiatives received about $2.05 million in government funds between 2018 and 2021.

Some of the money that the Biden administration provided to these groups was intended for projects unrelated to Israel.

In the case of Tides, the $30 million went to “a civil development program in regions of Africa, Asia, Latin America and the Pacific.”

The report argues that money intended for one project freed these organizations to fund activism in Israel to oppose the judicial reform efforts of the Netanyahu government.

“Money is fungible,” Jordan told JNS. “It’s tough to track exactly, but it looks like some of this money was also then being run through one or two NGOs, winding up on college campuses to promote all the crazy antisemitic, anti-Israel stuff on campuses.”

“Even worse yet, it looks like some of it maybe even funded organizations that had links to terrorism,” he said.

In one example, Rockefeller Philanthropy Advisors (RPA) “received millions of dollars in grants from the Biden-Harris Administration’s USAID, State Department and Department of Defense,” the committee memo says.

RPA then donated $557,000 to its “affiliate and partner,” the Rockefeller Brothers Fund (RBF), per the memo.

RBF, in turn, has “donated $190,000 to Defense for Children International Palestine, an Israel-designated terrorist organization with ties to the U.S.-designated terrorist organization, the Popular Front for the Liberation of Palestine,” according to the memo.

RBF has also made donations to Jewish Voice for Peace, one of the main organizers of anti-Israel demonstrations in the United States, and to Alliance for Global Justice, a U.S.-based non-profit that the committee alleges has provided funding to the Samidoun Palestinian Prisoner Solidarity Network.

The Biden administration designated Samidoun as a front for the PFLP in 2024.

New York City Mayor Zohran Mamdani unveiled his administration’s new housing initiative on Tuesday to considerable fanfare. The plan, titled “Block by Block,” aims to build 200,000 new affordable housing units and preserve or stabilize another 200,000 over the next decade.

The administration’s website describes “Block by Block” as “a sweeping blueprint to tackle New York City’s deepening housing crisis with the urgency and scale the moment demands. Spanning the full breadth of housing policy, from new construction to tenant protections to public housing, homeownership and worker protections, the plan lays out a comprehensive strategy to make New York City more affordable for working people.”

The reality is that this plan would significantly expand the power and protections afforded to renters, fulfilling a promise Mamdani made repeatedly on the campaign trail.

It would also impose steep penalties on landlords who allow their buildings to fall into disrepair and, in some cases, even transfer ownership of neglected properties.

The mayor smiled broadly as he announced his administration’s astounding plan to seize and redistribute properties owned by neglectful landlords — a proposal taken right out of the Marxist playbook.

“Through our new citywide campaign, Fix the City, we will focus on the worst landlords in New York City,” the mayor said, to much applause. “When necessary we will take aggressive legal action to remove negligent owners and property managers.”

He continued, “And for buildings that have suffered chronic neglect, we will work to transfer ownership to responsible stewards – stewards that include community land trusts, nonprofits or even the tenants themselves.”

If you’re wondering how low the administration might actually set the bar for “neglect,” and what new regulations and/or coercive tax measures it may impose on current property owners to achieve its goals, you’re not alone.

And how much of this “neglected” property belongs to his political enemies?

173 House Democrats vote against resolution honoring police amid rising attacks

House Democrats split over a resolution backing law enforcement as assaults on officers surged last year.

Just 29 House Democrats on Wednesday voted for a GOP-authored measure paying tribute to the “extraordinary sacrifice” law enforcement officers make and criticizing the defund the police movement for jeopardizing public safety.

Meanwhile, 173 Democrats voted with House Minority Leader Hakeem Jeffries, D-N.Y., against the resolution, while every GOP lawmaker present supported it.

7News confirmed that a man accused of sexually assaulting a woman in the stairwell of an Arlington parking garage is in the country illegally.

U.S. Department of Homeland Security Assistant Secretary Lauren Bis told 7News Reporter Nick Minock that Cristobal Liobardo Vasquez-Sanchez is from El Salvador and had prior charges for rape, sexual assault, property damage, drug possession, and larceny.

Sounds like a good candidate for deportation back to El Salvador’s notoriously fun gang prison.

Speaking of tattooed Democrat lunatics, “Dem congressional candidate charged with terrorist threats after pulling gun on government officials.” “Kirill Basin, 40, allegedly threatened two Maui County workers during the terrifying incident at around 9:30 a.m. on Friday before fleeing the building in Wailuku, Civil Beat reported. The longshot candidate for Hawaii’s 2nd Congressional District was arrested at his home around 12:30 p.m. on a terrorist threatening in the first degree charge.”

Talafreakco.exe: “I’ve never seen a politician memorize his lines like James Talarico and it’s creepy as heck.”

This guy thinks God is non-binary and loves abortion and transing the kids in the name of Jesus, but this right here is the creepy cherry on top of the leftwing cake:

There’s being a robot, and then there’s … this. Do you think Talarico plugs himself into his charging unit at night, or does someone do it for him?

And the cherry on top is you know that he’s absolutely lying about those random “I’m not a Democrat” voters coming up to him…

Disgraced Ex-California Dem Rep. Eric Swalwell is so sleazy that he’s even involved in secondhand sleaze: “Rep. Jimmy Gomez’s mystery makeout IDed as Eric Swalwell’s chief of staff.”

The mystery woman Rep. Jimmy Gomez admitted to making “mistakes” with is his best buddy Eric Swalwell’s former chief of staff, The Post can reveal.

The married California Democrat had an 11-month-old child at home when he was caught in a moment of passion with Swalwell’s minxy congressional aide Yardena Wolf three years ago.

Gomez, the founder of the Dads Caucus in Congress, confessed Tuesday in a statement that he cheated on his wife after The Post’s reporting on the encounter with Wolf, which kicked off a House Ethics Committee investigation, yielding fresh tips on his conduct.

Wolf, at the time 29, and Gomez, then 48, were spotted having an intimate moment against a car outside a party at Swalwell’s home north of the Capitol in the summer of 2023 — about two years into her tenure as Swalwell’s top staffer.

There’s also this: “[Wolf] co-founded an AI fundraising company with Swalwell in 2024.” That’s evidently Findraiser.AI. “Findraiser uses AI to search your donor database so you don’t have to.” Creating a tag for it now so I’ll have it ready when the inevitable scandal hits… (Hat tip: Dwight, in comments.)

A rebuke for the media types who accuse Republican voters of mindlessly doing Trump’s bidding: “Zach Lahn, who went viral for confronting Obama in 2009, beat Trump’s pick for Iowa governor.”

Lahn took down multiple established GOP politicians, including Randy Feenstra, who had the coveted Trump endorsement. Lahn had an endorsement from TPUSA and MAHA Action, but was not expected to win. He also won the coveted … Steak ‘n Shake endorsement?

Lahn strongly promoted the message of “Iowa First,” with a focus on agricultural pesticides, health, and Chinese influence. He also rejected outside funding (the internet is noting in particular that he rejected funding from AIPAC).

I wouldn’t necessarily count AIPAC backing as pro or con, save for the fact that they’ve backed some real squishy moderate Republicans lately (Dan Crenshaw and Tony Gonzales come to mind).

This is bad news: A confirmed case of New World Screwworm in south Texas.

U.S. Secretary of Agriculture Brooke Rollins says a single confirmed case of New World screwworm is contained, as state and federal officials move quickly to quarantine the area.

During a Thursday press call, Rollins reported that the single screwworm case was confirmed in a three-week-old beef calf on Wednesday in La Pryor, south of Uvalde. The U.S. Department of Agriculture immediately created a unified incident command team with the Texas Animal Health Commission and deployed the USDA Animal and Plant Health and Inspection Service to the area.

A 20-kilometer control zone was established around the detection site, and an expedited, targeted release of 4 million sterile New World screwworm flies a week is planned for the immediate area.

Texas State Veterinarian Dr. Lewis Dinges told the press that his staff have reported that the infested calf is improving and they have not found any other infested animals on the premises. There has also been no recent movement of animals onto or off the premises.

Dinges encouraged Texans to monitor their animals as often as possible and keep a close eye on any open wounds.

A quarantine has been issued on all warm-blooded animals within the control zone.

“Animals will still be able to move,” said Dinges. “We just need to make sure that they are moving safely and not moving the screwworm with it.”

It’s a nasty, nasty critter, and extreme measures are justified in keeping it from spreading.

The departure triggered immediate criticism of New Jersey’s tax and regulatory environment. Michele Siekerka, president and CEO of the New Jersey Business and Industry Association, called the announcement “not surprising, but it is no less sad.” Siekerka pointed to New Jersey’s 11.5% corporate tax rate — the highest in the nation, confirmed by the Tax Foundation’s 2026 state comparison — and noted that the number of Fortune 500 companies headquartered in New Jersey has declined from 22 in 2018 to 15 in 2025.

“These are the results of decades of anti-business policies in the state,” Siekerka said. “These are not accidents, nor are they coincidences.”

Assemblyman John Azzariti, a Republican representing the 39th District, was more pointed: “Texas didn’t win Samsung by accident. They won because they have spent years creating an environment where businesses want to invest, grow and create jobs. Meanwhile, New Jersey continues to raise costs, add regulations and send the message that employers are little more than a revenue source for government.”

Azzariti cited a pattern: in addition to Samsung, Mercedes-Benz USA, Honeywell, Hertz, and Sealed Air have all departed the state.

Speaking of relocating to Texas: “ExxonMobil Receives Shareholder Approval for Texas Move . The approval comes after Attorney General Paxton filed a lawsuit against a shareholder advisory firm that attempted to discourage the move.”

“Murder charge dropped for Arkansas sheriff nominee who killed teen daughter’s rapist.” No jury in the world…well, at least outside California and London. “The case against Aaron Spencer was dismissed by a judge on Thursday afternoon after law enforcement lost a dash camera memory card that may have captured the fatal October 2024 shooting of 67-year-old Michael Fosler.” (Hat tip: Dwight.)

Two Republicans and two Democrats in the Senate and House of Representatives are co-sponsoring proposed legislation designed to protect the Fourth Amendment’s bar of warrantless government searches and seizures of private citizens’ email content.

“The Fourth Amendment is clear: the government must get a warrant before searching an individual’s private property, including written communications. As today’s world has grown increasingly digital, that principle should apply just as strongly to an email inbox as it does to a desk drawer or file cabinet,” Rep. Warren Davidson (R-Ohio) said in a jointly issued June 2 statement.

“That’s exactly why I’m proud to cosponsor the Email Privacy Act — to ensure our freedoms carry into the digital world and that all communications are protected as the Founders intended. Congress must pass this commonsense legislation, so Americans’ rights are fully respected in the 21st century,” Davidson added.

Under current statutes, law enforcement authorities such as the Department of Justice (DOJ) are able to acquire email content that is at least 180 days old, thanks to the now-outdated storage capacity limits in force when Congress passed the Electronic Communications Privacy Act in 1986 and in subsequent amendments….

Joining the Ohio Republican in the House in co-sponsoring the Email Privacy Act are Rep. Suzan Delbene (D-Wash.), Senator Mike Lee (R-Utah), and Senator Ron Wyden (D-Ore.).

Usually when the Evil Party and the Stupid Party get together to pass a bill, it’s both Evil and Stupid, but this sound like the rare case where they’re working on something that’s actually needed.

Heh:

🚨 LMAO!! President Trump just dropped this absolute GEM: He's filling the newly improved Lincoln Memorial Reflecting Pool with leftist tears

“Things From Another World — the cult-favorite comic and collectibles chain owned by Dark Horse Comics — is shutting down all of its stores after 46 years in business.” Unmentioned in the article is that Dark Horse was bought by Swedish gaming company Embracer Group in 2022, and they’re busy Borging Dark Horse with a bunch of other media companies for an anticipated spinoff called “Fellowship Entertainment” with a bunch of Lord of the Rings licensed companies.

Should we seriously consider the possibility that Claude, or any large language model, might be conscious? And if it has feelings, is it capable of receiving moral instruction?

No. Absolutely not. Generative AI is harmful enough when we understand it as a conventional technology, but if we confuse fluency at generating text with consciousness or moral agency, we’re at risk of assigning responsibility to entirely the wrong parties whenever anyone uses a chatbot.

Ted (who is a very smart cookie) then goes into great detail why they’re not conscious.

Rick Beato on the Fender disaster. “If you were to go to any music store, Guitar Center, and pull a Fender Strat off the shelf and go play it at a gig, well, I wouldn’t recommend it, because the chances of it playing well are extremely low. That’s why there are so many other companies like Sire, PRS, Charvel, tons of companies that make Strat style guitars that are far better than normal Fenders that you buy at your local Guitar Center.”

Happy Anti-Communism Week everyone! (In addition, of course, to May 1st being one of two Victims of Communism Day.) The #SchumerShutdown ends with a whimper, a whole lot of SNAP fraud has been uncovered, more Democrats committing fraud, Chip Roy wants a complete immigration halt, Ukraine hits a bunch more Russian oil refineries, some semiconductor shenanigans, another company leaves Delaware for Texas, some tech companies in trouble, an interesting new pistol design, and a novel theory on “AI-related layoffs.”

It’s the Friday LinkSwarm!

As a side note, the mosquitos have been brutal the last few days. Possibly because it’s been a very warm (though largely dry) November, and the bats have already migrated south.

President Donald Trump on Wednesday night signed a continuing resolution at the White House that ends the record-breaking 42-day federal government shutdown.

The Senate passed the resolution on Monday and the House passed it earlier Wednesday evening. The resolution will keep the entire government funded through Jan. 30, and extends funding for military construction, Veterans Affairs, the Department of Agriculture, and Congress beyond that, through Sept. 30.

Trump slammed Democrats for causing the shutdown by refusing to go along with a clean continuing resolution for over a month, and urged voters to remember the party responsible for causing the six-week-long chaos during next year’s midterms.

“Republicans never wanted a shutdown and voted 15 times for a clean continuation of funding,” Trump said. “The Democrats shutdown has inflicted massive harm … So I just want to tell the American people, you should not forget this when we come up to midterms and other things. Don’t forget what they’ve done to our country.”

The resolution gives backpay to many federal workers and reinstates employees who were fired during the shutdown, but does not include an extension of Affordable Care Act subsidies despite it having been a key Democratic demand in the shutdown. The subsidies are set to expire at the end of the year.

And what did Chuck Schumer get for shutting down large portions of the federal government for more than a month? Two things: “Jack” and “Squat.”

I hear that if you call Senate Minority Leader Chuck Schumer’s office, the hold music is Cheap Trick’s “Surrender.”

Last Tuesday night, Democrats were jubilant, convinced they had just inflicted the first of many consequential defeats upon their detested foes, President Trump and the Republican Party. And now here we are, six days later, and Democrats are once again disappointed, infuriated, and at each other’s throats.

For the past 41 days, Republicans have had 53 senators willing to reopen the government, joined by Catherine Cortez Masto of Nevada, John Fetterman of Pennsylvania, and “independent” Angus King of Maine, who caucuses with the Democrats. But it requires 60 votes to cut off debate and bring the legislation to the floor for a vote, and thus to reopen the government, Republicans needed at least four more Democrats to change their mind.

Last night, five additional Democratic senators agreed to vote to reopen the government — and in the eyes of their fellow Democrats, effectively surrendered. Tim Kaine of Virginia, Dick Durbin of Illinois, Maggie Hassan of New Hampshire, Jacky Rosen of Nevada, and Jeanne Shaheen of New Hampshire shifted their positions.

Those eight agreed to reopen the federal government at current funding levels through January 30, and in exchange, all they needed was a pledge from Senate Majority Leader John Thune of South Dakota to hold a vote on legislation to extend the Obamacare exchange premium subsidies by the second week of December.

There are one or two other deal-sweeteners in there for Kaine, notably an attempt to reverse more than 4,000 federal layoffs the Trump administration announced in the shutdown, and language to prevent future layoffs through January 30.

Snip.

Republicans just got the government reopened in exchange for a promise of a vote — not even promise of passage! — and rehiring government workers who were on the job on September 30. That’s a very small price to pay, and Republicans didn’t have to get rid of the filibuster, the ultimate short-term gain, long-term loss for Republicans in the Senate.

Across three-fifths of the United States, the Trump administration has found half a million people receiving SNAP benefits twice over and 5,000 dead people receiving them. In deep blue states, the fraud is probably much worse.

It is important to clarify that 20+ states out of the 50 did not comply with the federal government’s request for information on SNAP beneficiaries, likely because they are trying to hide how many illegal aliens are illicitly receiving food stamps. So the horrifying numbers revealed by U.S. Secretary of Agriculture Brooke Rollins on Laura Ingraham’s Fox News show, The Ingraham Angle, are actually incomplete, and will probably be much higher if the administration can make radical Democrat states provide the necessary data.

Snip.

The secretary continued to list off food stamp recipient statistics: “80% [are] able-bodied Americans, meaning they can work, they don’t have small children at home, they’re not taking care of an elderly parent. They can work, and they choose not to work, of course, because they’re getting significant benefits from the taxpayer.”

We need to restore shame to able-bodied adults living on the public dole.

(Hat tip: Stephen Green at Instapundit.)

A Texas congressman is proposing a “freeze” on all immigration until the federal government fixes the country’s broken system.

U.S. Rep. Chip Roy (R–TX) said Wednesday he is introducing a bill called the “Pause Act” that will freeze all immigration until Congress achieves certain objectives, including reforming chain migration and birthright citizenship and ending H-1B visas.

He said the nation’s record-high foreign-born population is creating “a cultural problem about who we are as Americans.”

Roy, who is in a four-way race to be the Republican nominee for Texas attorney general in 2026, explained his proposal on The Benny Show.

In addition to the immigration freeze and related reforms, Roy called for revisiting Plyler v. Doe, a case originating in Texas that resulted in a 1982 U.S. Supreme Court decision requiring states to fund the education of illegal alien children.

Roy also said his bill would require vetting people for their adherence to Sharia law.

“Why are we importing any human being that is adherent to Sharia law, which is totally contrary to the Constitution, and our values, and Western civilization?” Roy asked host Benny Johnson.

“In Texas, we’ve been dealing with the brunt of the illegal immigration influence. But now we’re seeing, I think, the ramifications of the H-1B system and how it has been abused, in addition to chain migration and diversity visas, which we’ve been trying to fix for a long time, and we’ve been unable to do so,” said Roy.

Mostly agree with this, though there would probably have to be a way for individual exceptions to be made (say, a foreign Christian under a death threat from jihadists, or a Russian or Chinese defector, or a foreign NBA draft choice). But it should be so narrow as to require the personal approval of DHS Director Kristi Noem…

There are Somalis in Minnesota who wouldn’t vote for far leftist Somali Omar Fateh because he was from a different Somali clan, and they want members of the rival clan kicked out of the country…

They also hit multiple targets in Novorossiysk, including both the oil terminal and the S-300/400 system defending it. Also, there’s no way I can donate €100 right now, but I really want one of those “This Is Fine” patches…

Orchestrating Over 180 Anti-Trump Lawsuits Through CREW: As co-founder of Citizens for Responsibility and Ethics in Washington (CREW), Eisen led hundreds of ethics complaints and lawsuits against the Trump administration, often perceived as partisan harassment that politicizes oversight and strains constitutional separation of powers.

Snip.

Involvement in USAID Funding Scandal: Accused of ties to $17M misappropriation via family-linked NGO, raising corruption concerns in foreign aid.

Plenty more at the link.

(Heavy sigh) Look, I’ve been avoid the whole stupid Tucker Carlson thing because he hasn’t been a particularly important part of the mediascape for a while, and plenty of other people were already dog-piling him. Yet, this week he seemed to turn up some pretty interesting information on would-be Trump assassin Thomas Crooks. Namely that he was a pro-Trump supporter…until he radically changed his tune in early 2020.

On July 19, 2019 Crooks writes: “Ilhan Omar and others are invaders and should honestly be killed and their dead bodies sent back.”

On July 20, 2018, Crooks writes: “If youre saying trump is a bad president you arent a patriot as trump is the literal definition of Patriotism”

Seven hours after that comment, Crooks writes: “I hope a quick painful death to all the deplorable immigrants and anti-trump congresswoman who dont deserve anything this countru [sic] has given them”

Later that evening he wrote: “Everyone of the Trump hat-ing democrats deserve to have their heads chopped of and put on steaks for the world to see what happens when you fuck with America”

These types of comments continued for months, “and became increasingly violent.”

“If any of the democratic candidates win. They wont be in there for long. Because unlike the dems we have guns and lots of them”

He also quoted Mao – writing “The only real political power comes from the barrel of a gun.”

The Change:

In early 2020 as the pandemic shifted into the headlines, crooks “radically” changed – writing of “trumps stupidity.”

He then began to mock the idea of the deep state – writing that “The deep state is simply made up of anybody who dis-agrees with the right wing. Conversation over.”

In Feb. 2020, Crooks called out Trump supporters as “brainwashed,” and a “cult.”

Later that day, Crooks called Trump a racist.

And in April 2020 when the COVID panic was in full swing, Crooks became pro-lockdown, writing “It seems that you people don’t understand that sometimes Public safety comes before your Personnel rights.”

He then wrote: “…going to a chinese new years party in america isn’t putting you at risk for corona virus because believe it or not viruses don’t spread through race like Tucker Carlson probably told you.”

In May of 2020, Crooks called Republican concerns over voter fraud “ignorant.”

He then wrote a comment that sounded like a “digital manifesto,” Carlson reports.

“they only way to fight the gov is with terror-ism style attacks, sneak a bomb into an essential building a set it off before anyone sees you, track down any important people/politicians/military leaders etc and try to asasinate them. Any sort of head fight is suicide and even ambush/surprise attacks likely aren’t going to end well.”

Sounds like another “known wolf,” doesn’t it? And the assertion that “there’s no deep state” (combined with what else we know about the assassination) makes you go “Hmmm.”

Senator Mike Lee (R-UT) is pushing back on the idea that the Affordable Care Act (ACA), known as Obamacare, has made health insurance costs more affordable, saying, “Obamacare makes everyone else poor.”

Lee shared a graphic, first posted by President Trump on Truth social, showing how major health insurance company stocks have performed since the ACA was enacted in 2010 to November 2025.

The seven major health insurance companies depicted on the graph show gains of anywhere from 414% to 1177% in their stock prices between March 2010 and November 2025.

Health insurance companies are making money hand over fist—not because they’ve discovered new & innovative ways of making Americans healthier, but because Obamacare insulates them from competition while giving them massive subsidies

Lee called out the insurance providers, noting that they’re “making money hand over fist” but not because they are providing “new & innovative ways of making Americans healthier.”

Instead, Lee says, these health insurance companies are prospering due to the bureaucratic barriers that prevent new competition and from massive subsidies from the federal government.

The Saudis are getting ready to purchase 48 F-35s.

California Governor Gavin Newsom’s former chief of staff Dana Williamson was arrested Wednesday in an FBI corruption probe and charged with multiple counts of bank and wire fraud.

Federal authorities accused Williamson, 53, of participating in a scheme to funnel campaign money from former federal Secretary of Health and Human Services Xavier Becerra into a personal account. Sean McCluskie, Becerra’s former chief of staff, was named as a co-conspirator.

“This is a crucial step in an ongoing political corruption investigation that began more than three years ago,” U.S. Attorney Eric Grant said in a statement. “As it always has, the U.S. Attorney’s Office will continue to work tirelessly with our law enforcement partners to protect the people of California from political corruption.”

Williamson and McCluskie stole $225,000 between February 2022 and September 2024 from Becerra’s dormant state campaign fund, the federal indictment says. The Department of Justice investigation into the matter began three years ago, under former President Joe Biden’s administration, FBI Sacramento Special Agent in Charge Sid Patel said.

“The news today of formal accusations of impropriety by a long-serving trusted advisor are a gut punch,” Becerra told local outlet KCRA 3.

Williamson was hit with 23 charges, including conspiracy to commit fraud, conspiracy to defraud the United States and obstruct justice, subscribing to false tax returns, and making false statements, the U.S. Attorney’s Office said.

Democratic political consultants are so money-hungry they’ll rake graft off other Democrats. Big fleas have little fleas…

Man, it sure seems like a lot of prominent Democratic politicians are committing mortgage fraud. ‘Rep. Eric Swalwell (D-Calif.) was hit with a federal criminal referral for alleged mortgage and tax fraud related to his purchase of a $1.2 million home in Washington, DC, that he claimed as a primary residence.” As Dwight notes: “You may remember Eric Swalwell for such hits as ‘banging a Chinese spy‘” and “threatening to use nuclear weapons against gun owners.”

So a Chinese fraudster connected to Communist intelligence services wandered in from Canada and bought a trailer park next door to a stealth bomber base in Missouri.

This is not the opening line of a surreal joke.

Whiteman Air Force Base is home to our tiny fleet of B-2 bombers, and yet an RV park just a mile away “is one of several properties near U.S. military interests acquired by a web of shell companies, which are ultimately owned by a couple who live in Canada and belong to organizations controlled by disgraced Chinese tycoon and self-described former CCP intelligence ‘affiliate,’ Miles Guo,” according to a bombshell Daily Caller report.

Someone in the federal government needs to get this fixed. Get a warrant to toss the entire trailer park to see what spectrum warfare equipment they might be using, then seize the place under eminent domain for national security reasons.

BREAKING: The Attorney General of Kansas just charged Mayor Jose Ceballos of the City of Coldwater for illegally voting as a noncitizen in several elections.

Not only did he get elected city councilman & mayor as a noncitizen, he also voted. WOW! The six charges come immediately… pic.twitter.com/amhsJJvaZW

‘We now have tools, thanks to the current White House, that we haven’t had in over 10 years,’ said Kansas Secretary of State Scott Schwab, ‘that we can check through the SAVE program, to find out if folks end up on our voter rolls. And they could be a legal resident, but they’re not a citizen. We want to make sure that gets clarified.’

Deport him.

Least you think I’m never critical of President Trump, I want to note that his trial balloon for 50 year mortgages is a really bad idea. It’s not a way to build wealth, and the only party getting rich off that deal is the banks. Financially, you’d be better off living in a van for a few years until you can afford a real mortgage.

This certainly has a whiff of scandal: “Houston ISD Sues Texas Attorney General to Block Release of Emails with California PR Firm. The district wants to keep communications with a PR firm from becoming public.”

Houston Independent School District (ISD) filed a lawsuit against Texas Attorney General Ken Paxton to block the release of emails between the district and Los Angeles public relations firm Bryson Gillette.

Bryson Gillette is former Obama aide Bill Burton’s public relations firm run by Democratic operatives. White House Press Secretary Jen Psaki was a senior adviser there.

Bryson Gillette was involved with the district’s rebranding in May. Houston ISD’s Chief of Public Affairs and Communications Alex Elizondo told an advisory committee that the district had a brand identity that “isn’t inviting or super compelling.”

A Houston ISD spokesperson said the rebrand came at no additional cost to the district and coincided with the rollout of new district and campus website designs scheduled for August.

According to the suit, ABC13 News requested one month of emails between Houston ISD and Bryson Gillette on May 8, which the district received on May 9. On May 21, the district asked Paxton to withhold documents and submitted the required materials to the Office of the Attorney General (OAG) asserting attorney-client privilege.

The OAG issued a ruling on August 12, ordering Houston ISD to release the records and stating that attorney-client privilege did not apply.

Houston ISD filed a lawsuit in Travis County on September 11, looking to block the emails from release.

California Gov. Gavin Newsom has repeatedly slurred a federal judge by name, echoing President Trump’s history of diatribes against judges even before the current Democrat started copying the former Democrat’s social media style and insulting nicknames.

The perceived contender for the 2028 Democratic nomination for president may cluck his tongue again when he sees the latest order from U.S. District Judge Roger Benitez in a lawsuit against The Golden State’s alleged mandate on school districts to hide from parents their children’s asserted gender identity at odds with sex.

The President George W. Bush nominee ordered state Attorney General Rob Bonta and the California Department of Education to “show cause” on why they should not be sanctioned for “misleading” Benitez so he would remove them from the suit by teachers who allege their school district muzzled them and parents of “gender incongruent children.”

The state defendants’ motions to dismiss and opposition to the plaintiffs’ motion for summary judgment claimed that CDE had “withdrawn and conclusively replaced” an FAQ page that contained the challenged policies, which they claimed was the “only basis” for being named defendants and thus made the case moot, Benitez wrote.

“However, evidence demonstrates that the CDE may have merely moved the challenged content of the FAQ page to a new, required ‘PRISM’ training module,” as documented by the plaintiffs’ lawyers at the Thomas More Society, the judge said, ordering state defendants to explain their behavior Nov. 17 in court.

“From day one, officials from the local school district all the way to the governor’s mansion have tried to deflect responsibility” but “have now been caught not only lying to California taxpayers but attempting to mislead the Court to escape accountability,” TMS Executive Vice President Peter Breen said in a statement.

Based on early voting and some voting day results, no candidate secured over 50 percent of the votes cast, so the two highest vote recipients will move on to the runoff election, the date of which remains to be set by Gov. Greg Abbott.

The North Texas Senate seat was vacated when former state Sen. Kelly Hancock (R-North Richland Hills) resigned and was appointed by Abbott to fill the vacancy as the Texas Comptroller of Public Accounts.

Snip.

Wambsganss was endorsed early on in the race by Lt. Gov. Dan Patrick, who has vocally opposed expansion of casino gambling in Texas. She has also received support from Texans United for a Conservative Majority (TUCM), which opposes gambling expansion as well. Texans for Lawsuit Reform, a group not frequently on the same side of an electoral battle as TUCM, has also supported Wambsganss.

The Substrate startup has been doing the rounds in the news lately, thanks to its proposition of making chips using particle accelerators and X-rays instead of conventional EUV lithography, claiming it can eventually have angstrom-sized features at only $10,000 per wafer—in U.S. fabs, no less.

Oooo, where to begin? IBM tried experimenting with x-ray lithography in the 1980s and 90s, and found the rays were too energetic to use because they damaged wafers.

And technically, semiconductor equipment manufacturing already has particle accelerators: they’re called ion implanters and they’re used for gate dopants. Axcelis (formerly Eaton Semiconductor) and Applied Materials (both companies I worked for in the 1990s) make good money selling them, and there are a whole bunch of limits-of-physics reasons why you can’t use them for lithography. (Historical trivia: Applied Materials used to have their own in-house designed ion implanters, but their current offerings trace back to a competitor named Varian they bought in 2011.)

Those are bold claims, and an article by Fox Chapel Research (FCR) is seriously questioning whether they pay off.

The write-up is the first of two parts, and takes aim at not just the seemingly outlandish technological claims, but also at the track record of the venture’s founders, as well as the overall messaging on Substrate’s website. The start-up is backed by various investment funds, namely but not only Founders Fund, of whom Peter Thiel is part of.

The report says the founders are James and Oliver Proud, who reportedly have no experience in the semiconductor industry, nor do any of the investor funds. James’ latest venture was apparently the Sense sleep tracker, a product that had its inception on Kickstarter to the tune of $2.5m, but didn’t materialize until funding rounds raised over $50m. After release, the tracker was found to be borderline useless by reviewers and drew many comparisons to a scam.

ClowfishTV floats an interesting theory: A lot of those “AI-related” layoffs are just companies using that as an excuse to purge the woke from the ranks.

For more than half a century, Delaware stood as America’s corporate capital, renowned for its business-friendly laws, respected Chancery Court, and consistent legal rulings. But in recent years, leftist activist lawmakers and politicized judges have undermined that very foundation, sparking an exodus of major companies seeking stability and fairness to more welcoming states like Texas and Nevada.

On Wednesday morning, Coinbase joined the growing exodus, announcing on its website and in a Wall Street Journal op-ed by Chief Legal Officer Paul Grewal that it is moving its state of incorporation from Delaware to Texas.

“For decades, Delaware was known for predictable court outcomes, respect for the judgment of corporate boards, and speedy resolutions,” Grewal wrote in the op-ed.

However, he pointed out that recent inconsistent Chancery Court rulings and reliance on ad hoc legislative fixes do not create a sustainable business environment.

“Our decision to leave is about ensuring more predictable opportunities for the company, our shareholders, our customers and the new on-chain ecosystem we’re building,” he noted, adding, “Texas offers efficiency and predictability, in part thanks to recent corporate-law reforms that enhance governance flexibility and legal predictability.”

Grewal concluded, “Delaware wasn’t always the go-to choice for companies. At one point it was New Jersey, and before that New York. We’ve reached another inflection point in corporate law. The more states that can credibly attract companies, the better—and we’d like to see Delaware step up to stay in the mix. But as for Coinbase, you can find us in Texas….”

The exodus list from Delaware increases:

Tesla: Moved to Texas.

SpaceX: Moved to Texas.

Trump Media & Technology: Moved to Florida.

Dropbox: Moved to Nevada.

TripAdvisor: Moved to Nevada.

Roblox: Moved to Nevada.

Pershing Square: Moved to Nevada.

The Trade Desk: Moved to Nevada.

AMC Networks: Moved to Nevada.

Madison Square Garden Sports: Moved to Nevada.

Fidelity National Financial: Voted to move to Nevada.

So was a Delaware judge letting Elon Musk know how much he hated him for supporting Trump worth it?

“750-meter-long Chinese bridge partially collapses just weeks after opening.” From a landslide, but I’m betting the usual Chinesium/tofu drugs construction quality didn’t help…

At its Midlothian Data Center, alongside a number of state officials, Google announced a $40 billion data center infrastructure investment in Texas.

Sundar Pichai, CEO of Google and its parent company Alphabet, said that the investment will go toward the construction of three data center campuses located in Armstrong and Haskell counties.

Armstrong County is southeast of Amarillo. Haskell County is north of Abilene. Both counties have a whole lot of nothing there.

“They say that everything is bigger in Texas – and that certainly applies to the golden opportunity with AI,” Pichai stated.

“This investment will create thousands of jobs, provide skills training to college students and electrical apprentices, and accelerate energy affordability initiatives throughout Texas.”

Gov. Greg Abbott said the new Google AI data center announcement is “a Texas-sized investment in the future of our great state.” U.S. Sens. John Cornyn (R-TX) and Ted Cruz (R-TX) were also in attendance, along with Congressman Jake Ellzey (R-TX-06) and a number of other local officials.

“Google’s $40 billion investment makes Texas Google’s largest investment in any state in the country and supports energy efficiency and workforce development in our state,” Abbott added. “We must ensure that America remains at the forefront of the AI revolution, and Texas is the place where that can happen.”

Google has already officially broken ground on two other data centers in the state: one in Midlothian in 2019, and the other in Red Oak in 2023. The technology company has since announced further investments into data and cloud infrastructure to the tune of $2.7 billion.

This most recent announcement of a $40 billion investment will focus on building out infrastructure to support the three new data centers. Some of that investment includes building up new and existing energy storage facilities, advanced water use operations, and partnering with universities to offer technology training and education.

My reservations about Google’s AI notwithstanding, that will offer a bunch of real jobs for real Texans…assuming the AI bubble doesn’t burst before they get built.

Speaking of tech firms in trouble, video game maker Ubisoft (makers of Prince of Persia and Assassin’s Creed games) has not only postponed an earnings report, they’ve suspended stock trading. I can’t recall a single instance where that was a good sign. The last time we mentioned Ubisoft, they were pissing off Japanese gamers for including a black samurai in one of their games…

Ian McCollum looks at the new Rideout Arsenal Dragon, a low-bore-axis, lever-delayed pistol. It’s funky looking and has some interesting features, including complete non-tool disassembly. However, the price point would make it way too expensive to consider even if I had a job, he experiences several firing malfunctions testing it (though it is a prototype), and I fear the tiny little tabs it uses may not hold up under heavy use. Still a pretty interesting design.

There’s been a lot of media articles that the runaway Texas House Democrats are going to cave, but it hasn’t happened yet. The Trump Administration continues to rack up success after success at the border, Ukraine hits more Russian oil facilities, once again Adam is full of Schiff, more illegal alien sex traffickers nabbed, and China finally picks on someone its own size.

The Department of Homeland Security (DHS) has said that the U.S.-Mexico border is experiencing “all-time lows” of illegal immigrant crossings after President Donald Trump’s administration ramped up efforts to secure the southern border.

On August 1, DHS released preliminary numbers for the month of July that report to show nationwide encounters are 90 percent lower than during the Biden administration, in addition to the “lowest single-day apprehensions in history” — on July 20, DHS reported just 88 apprehensions at the southern border and 116 across the country.

“History made, again. The numbers don’t lie — this is the most secure the border has ever been,” said DHS Secretary Kristi Noem. “President Trump didn’t just manage the crisis — he obliterated it. No more excuses. No more releases. We’ve put the cartels on defense and taken our border back.”

The numbers released from DHS reflect previous assessments made by U.S. Customs and Border Protection (CBP), which said in July that nationwide apprehensions have hit a “new historic low” following a “dramatic shift” in policy focus since President Donald Trump entered office.

According to the Migration Policy Institute, encounters at the U.S.-Mexico border have dropped to levels not observed since the 1960s.

Progress. “Trump Purges 275,000 Illegal Aliens From Social Security.”

Months after President Trump signed a Presidential Memorandum targeting illegal aliens and other ineligible individuals from collecting Social Security Act benefits, the president told reporters at the White House on Thursday afternoon that nearly 300,000 illegals have been removed from the government program that provides financial benefits to eligible citizen taxpayers and/or lawful permanent residents (green card holders).

“Last month, I signed the One Big Beautiful Bill, and allowed No Tax on Social Security for our great seniors … and to protect our benefits, we’ve already kicked nearly 275,000 illegal aliens off of the Social Security system,” Trump told reporters.

Recall that on April 15, the president signed a memorandum directing federal agencies to take immediate action to purge the Social Security system of illegals and fraudsters.

As Maureen Steele via American Greatness elegantly noted earlier this year, “We don’t need an executive order to bar illegals from Social Security – we need a government that obeys the law.”

Let’s not forget that the Biden-Harris regime facilitated the invasion of illegal aliens, allowing millions of these third-worlders to siphon dollars and essential services from citizens and lawful permanent residents – in what some have described as a classic Cloward–Piven strategy.

The Federation for American Immigration Reform estimated that taxpayers spend more than $182 billion annually to cover costs associated with 20 million illegal aliens and their children, which includes $66.4 billion in Federal expenses plus an additional $115.6 billion in state and local expenses.

The free lunch for the Democratic Party’s illegals is coming to an end.

A Democratic whistleblower told the FBI that Senator Adam Schiff authorized the leak of classified information related to the Russia collusion investigation in 2017 in an effort to discredit President Trump, newly-released documents show.

The whistleblower, who worked for Democrats on the House Intelligence Committee for more than ten years, first reported Schiff’s alleged behavior to the FBI in 2017, when Schiff was leading the committee’s Russian collusion investigation.

FBI Director Kash Patel confirmed on Monday that he had handed over the documents, first obtained by Just the News, to Congress. “We found it. We declassified it. Now Congress can see how classified info was leaked to shape political narratives – and decide if our institutions were weaponized against the American people.”

The FBI interviewed the whistleblower most recently in June 2023, at which point the unidentified intelligence officer said he had been part of an all-staff meeting called by Schiff in which the then-California representative “stated the group would leak classified information which was derogatory to President of the United States Donald J. TRUMP. SCHIFF stated the information would be used to Indict President TRUMP.”

“[The whistleblower] stated this would be illegal and, upon hearing his concerns, unnamed members of the meeting reassured that they would not be caught leaking classified information,” the report added.

The whistleblower expressed concerns that Schiff’s actions were “treasonous” and “illegal.”

District Judge Paul A. Engelmayer (Obama) wrote in his order that the government’s premise that unsealing the records would shed light on meaningful new information was “demonstrably false,” and that “unsealing the grand jury materials would not reveal new information of any consequence.”

“Contrary to the Government’s depiction, the Maxwell grand jury testimony is not a matter of significant historical or public interest. Far from it,” he wrote. “It consists of garden-variety summary testimony by two law enforcement agents. And the information it contains is already almost entirely a matter of longstanding public record.

Translation: Either it implicates powerful Democrats, or else we need to keep the issue alive to try to dirty up President Trump.

Truth: “White House Deputy Chief of Staff on Redistricting Battle: ‘We all know Democrats cheat.”

White House Deputy Chief of Staff Stephen Miller is blasting Democrats for complaining about the current redistricting uproar and accuses them of stealing dozens of House seats by counting illegal aliens in the last census.

Miller told Newsmax that Democrats brought in tens of millions of “invaders” into the nation through their open borders policies to “rig the results of the census” and the apportionment of congressional seats.

Miller pointed out that even though Republicans won a landslide in the House popular vote, they only picked up a 4-seat majority due to Democratic gerrymandering, manipulation and rigging of congressional districts.

He contrasted the gains of this last election with the 2010 election, in which the Republicans won a much smaller majority in the popular vote, yet gained 63 seats in the House.

President Trump on Monday announced plans to place the Metropolitan Police Department under federal control and to deploy several hundred National Guard troops and more than 100 FBI agents to the streets of Washington, D.C., to assist local law enforcement in fighting crime.

“I’m announcing a historic action to rescue our nation’s capital from crime, bloodshed, bedlam, squalor and worse,” Trump said during a press conference on Monday. “This is liberation day in D.C., and we’re going to take our capital back.”

“Our capital city has been overtaken by violent gangs and bloodthirsty criminals, roving mobs of wild youth, drugged out maniacs and homeless people,” he said.

Trump said the murder rate in D.C. is higher than some of the “worst places” in the world, including Bogota, Colombia.

Trump has the authority to take over the Metropolitan Police Department under the District of Columbia Home Rule Act, which includes a provision that grants him the ability to take over the department when there are “special conditions of an emergency nature.” As part of the federal takeover, Attorney General Pam Bondi will lead the department, while Terry Cole, the new DEA Administrator, will be the interim federal commissioner of the department.

On Friday, the Trump administration dispatched federal law enforcement officers to tourist hotspots around D.C. Trump has also threatened to federalize the district if crime rates do not fall and on Monday, he said he would send in the military, if needed.

Attorney General Pam Bondi rescinded several DC police executive orders Thursday that restricted officers from arresting illegal migrants – vowing that the nation’s capital will not be a sanctuary jurisdiction under President Trump.

“DC will not remain a sanctuary city. Actively shielding criminal aliens will not happen,” Bondi declared in an interview with Fox News host Sean Hannity.

The attorney general’s comments came as she issued a new directive voiding commands issued – as recently as earlier Thursday – by DC Metropolitan Police Department Chief Pamela Smith.

Smith is not the sharpest knife in the drawer. “DC police chief [Pamela Smith] asks what ‘chain of command’ means after question from reporter.”

Hilarious news this week: “Two Chinese ships collide while chasing Philippine Coast Guard boat.” A Chinese Coast Guard ship collided with a Chinese Navy ship. And yes, there is video:

A power bill crisis is gripping parts of the U.S. Mid-Atlantic and is set to worsen, threatening to financially crush households as long-range forecasts point to a brutally cold winter. What began in Baltimore, Maryland – as first covered in our reporting one year ago- has now spread to New Jersey, where residents are furious over skyrocketing electricity costs.

The common denominator in both states? A disastrous green energy agenda, pushed by radical leftist lawmakers, is dismantling reliable and cheap fossil fuel power generation in favor of unstable solar and wind. This has unleashed a power bill armageddon on working-class and middle-class households, as well as mom-and-pop businesses, all while baseload power demand surges in the era of AI data centers.

Fox News is beginning to latch onto the power bill crisis theme, starting with coverage of New Jersey residents who are absolutely furious over exploding power bills. This new development could severely damage the state’s Democratic leaders in the upcoming elections.

This all started when New Jersey’s Board of Public Utilities approved a 17 to 20% rate hike for power bills in June. Many residents were shocked when they opened their bills at the end of last month.

“$200 more, I know my electrical bill,” one Jersey woman told Fox News reporter CB Cotton, adding, “I was shocked. So to say the least, I’m very disappointed. This is killing us, and every time you turn around it’s something more. You only get little pleasures in life that you enjoy, and my air conditioner is one of them.”

Perhaps Democratic Gov. Phil Murphy’s decision to shutter the state’s nuclear and coal plants, without a one-to-one replacement for lost capacity on the grid, was a catastrophic error that is only now coming home to roost. He also prioritized offshore wind farms and other green energy projects, which have left the grid more fragile than ever.

“Just like the old gypsy woman every Republican ever said!”

The International Brotherhood of Teamsters, disillusioned and even disavowed by Democratic leaders, is showing Republicans some love in the midterms. The union’s donations are evidence of a realignment that could outlast President Trump’s term unless Democrats embrace at least some union-friendly policies like tariffs.

Prior to 2024, the Teamsters backed almost no Republicans. This year, the Democrat, Republican, Independent Voter Education PAC gave the maximum, $5,000, to each of 22 House Republicans and backed several Senate candidates, Politico reports. They also gave $50,000 to the Republican Attorneys General Association.

After dumping millions into the 2024 election cycle and coming up short, Las Vegas Sands appears ready to roll the dice again.

New financial disclosures show that Texas Sands PAC, the Texas-based political arm of the casino giant, has more than $9 million in cash on hand heading into the upcoming election season. That money comes almost entirely from Miriam Adelson, the billionaire owner of Las Vegas Sands and majority owner of the Dallas Mavericks. Despite its name, Sands does not operate casinos in Las Vegas or anywhere in the United States; its operations are exclusively in China and Singapore.

While the group has largely held off on spending in recent months, records show it contributed $1.8 million to members of the Texas House during the 2024 cycle—$1.34 million to Republicans and $457,500 to Democrats. That spending mirrors the strategy the group employed last time: pour money into protecting lawmakers who supported its push to legalize casino gambling in Texas.

That effort didn’t go as planned.

Despite getting casino legislation to the floor of the Texas House in 2023, Sands watched its momentum collapse in the primaries. Voters rejected the very lawmakers who had sided with the casino giant. Former House Speaker Dade Phelan, the top recipient of Sands money, was forced into a runoff. Meanwhile, 14 Republican House members who voted for casino legislation either lost re-election or chose not to seek it.

Sands and Adelson attempted to salvage the cycle with a massive last-minute push. The Texas Defense PAC, funded entirely by Adelson, poured more than $7 million into runoff races in an effort to rescue Phelan’s allies. But again, the money didn’t translate into wins.

Now, Sands is recalibrating.

Although no major new contributions have been reported yet this cycle, those connected to the group have continued to work in some statewide campaigns.

Former State Sen. Kelly Hancock, who is now running for state comptroller, has hired John Jackson to run his campaign.

Until earlier this year, however, Jackson served as Sands’ head political consultant in Texas. He previously managed campaigns for Gov. Greg Abbott and U.S. Sen. John Cornyn.

Hancock did not respond to a request for comment on whether he supports the group’s efforts to bring government-monopoly casinos to Texas.

Neither Don Huffines or Christi Craddick—the other two candidates currently in the race—have casino operatives leading their campaigns.

Hancock is not the only one with senior staff tied to the casino operator.

Jordan Berry, a recent registered lobbyist for Sands, also serves as a campaign consultant to numerous candidates in the state legislature, including State Sen. Mayes Middleton (R–Galveston) in his campaign for attorney general. Berry’s lobby registration with all his clients ended on June 23.

City-owned Kansas City grocery store closesdespitebecause of millions of dollars in subsidies.

Not this shit again: “Judge Rules Against Little Sisters of the Poor in Obamacare Contraception Case.”

A U.S. district court decided on Wednesday to strike down a 2017 federal regulation that exempted religious employers from the Affordable Care Act’s mandate for employer-sponsored health insurance to cover the cost of contraception.

If the ruling holds, religious non-profit organizations such as the Little Sisters of the Poor, the defendants in the case, may now be required to file for an accommodation process with the government that still maintains employees’ access to contraception without the religious organization having to pay. For-profit employers would have access to no religious exemption from the mandate whatsoever.

Judge Wendy Beetlestone, chief judge for the Eastern District of Pennsylvania, found that the Trump administration’s 2017 rule expanding religious exemptions from the contraception mandate was “arbitrary and capricious,” thus violating statutory authority. Consequently, she declared the rule vacated.

The left can’t stop attacking the Little Sisters of the Poor because it is intolerable to them that there is an legitimate source of moral authority apart from the state. Catholic nuns must be forced to pay for contraception (and abortions) as a token of their submission to social justice. Every. Knee. Must. Bend.

I know you’ll be shocked to learn that Beetlestone is an Obama appointee…

So on Monday, I get a text from my property management company saying that they’ve retained an outside security company to address the numerous complaints about loitering and drug sales in the neighborhood.

‘Beginning today, you will see these security personnel around the properties and in the neighborhood, goes on and on about procedures.’

Okay. Today’s Wednesday. It’s two days later, I get an email from my property management, and they said,

‘We’re disappointed to share that the security company that was hired has pulled out of the neighborhood. After a day and a half of doing recon and observing activity in the neighborhood, they decided the problems with crime exceed their resources to control. We will continue to work with organizations and neighborhood and explore other options to improve public safety and so on.’

Funny what happens when a Democrat-run locale decides to “defund the police” because a random black drug user died…

“Commissioner Ramsey Seeks Removal of Harris County Judge Lina Hidalgo. Following a vote to censure Hidalgo, Ramsey said, ‘It is time to consider replacing Judge Hidalgo.'”