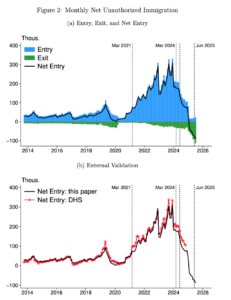

As I’ve stated before, Biden importing several million illegal aliens across the southern border raised housing prices, because increasing demand without increasing supply raises prices.

A working paper from the Federal Reserve Bank of Dallas concluded that the large influx of illegal aliens during the Biden administration drove up housing prices and rents.

According to the paper, roughly 7 million people illegally came to the United States between 2021 and 2024.

This spike of illegal immigration “raised local house prices and rents without expanding housing supply,” acting as a “demand shock to local housing markets.”

Using court records and border enforcement information alongside housing market data, the economists estimated that illegal immigration “can explain about 30% of the total growth in house prices and 20% of total growth in rents over the boom period for the average local market.”

“We’ve actually been saying this for a number of months now,” U.S. Rep. Beth Van Duyne (R–Irving) told CBS News. “I don’t think people sometimes understand the ramifications of having so many folks enter your country illegally in such a short period of time and the financial disaster that it causes.”

Although housing costs have begun to ease, prospective homeowners continue to face affordability challenges. The National Association of Home Builders calculated that in Texas, a $1,000 median price increase would price out roughly 15,000 households.

John Bonura and Selene Rodriguez from the Texas Public Policy Foundation are urging lawmakers to “ensure that scarce housing opportunities first serve the people to whom this country ultimately owes its highest obligation.”

You mean citizens rather than illegal aliens? Seems like the Democrats have those priorities reversed.

The paper can be found here, in which we find this breathtaking chart showing the effects of the Biden Administration’s deliberate attempt to leave the southern border unsecured:

Republicans need to drop direct mailers to everyone under the age of 30 this year, explaining that Biden’s illegal alien wave drove up housing prices, and that excessive regulation in blue cities and states restrict demand. Who knows, this little nugget of truth may even give some of them a clue as to why socialism doesn’t work…

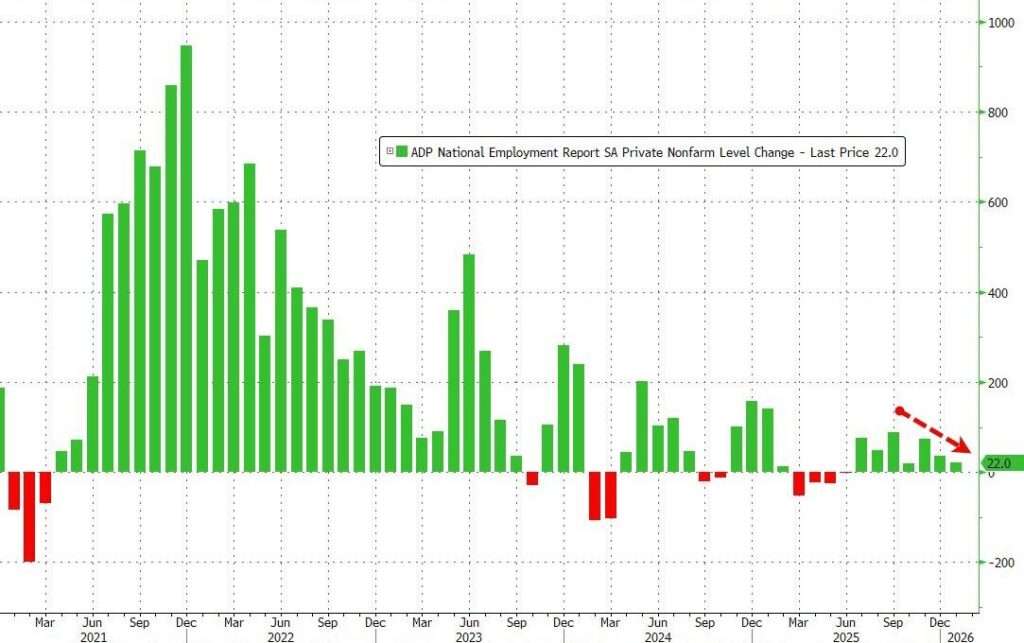

Statistics show that, one year into Donald Trump’s second term, the economic lassitude of the Biden Recession is still weighing down the American economy, as it isn’t creating jobs.

While we will not be getting the payrolls report this week (due to a very brief govt shutdown), ADP’s Employment report paints a poor picture for hiring (even if jobless claims paints a healthy picture for ‘not firing’) adding just 22k jobs (well below the 45k expected).

22 thousand jobs isn’t even a dead cat bounce, it’s a rounding error. And the low jobless claims are just because most of the workers fired/laid off during the Biden Recession have run out of eligibility.

Goods producing firms added just 1k jobs (Construction +9k, Manufacturing -8k – which has lost jobs every month since March 2024) while Services firms saw only 21k jobs added (with health care a standout, adding 74k job, while Professional Services lost 57k jobs).

“Job creation took a step back in 2025, with private employers adding 398,000 jobs, down from 771,000 in 2024,” said Dr. Nela Richardson Chief Economist, ADP.

Interestingly, small firms saw job additions while large firms saw job losses…

We’re not seeing the massive manufacturing job losses critics of President Trump’s tariffs predicted, but we’re also not yet seeing any gains from the lowering of foreign tariffs.

Job seekers are discouraged by a plague of ghost job listings intended to provide the illusion of growth, with no intention of anyone ever being hired.

Inflation is low, yet consumer confidence is at the lowest level in more than a decade. Stocks are booming, yet no one seems to be hiring. (This seems to be my personal experience as well.) Trump and congressional Republicans have managed to lower taxes, yet the “animal spirits” of the American economy do not seem like they’re been unleashed.

Is AI eliminating jobs? Maybe, especially in the service sector (those AI agents everyone hates have probably replaced some humans on support lines). But tech has been a job growth driver for much of this century, and an AI infrastructure build-out seems to be sucking up all available venture capital (and then some) with very little to show for it in the way of actual profits thus far.

Maybe job creation will only resume after California’s billionaires have finished fleeing to avoid the proposed wealth tax.

Would aggressive rate cutting by the Fed help? Probably, but outgoing Fed chair Jerome Powell seems to be pursuing rate cuts with all the vigor of Æthelred the Unready.

The American economy seems becalmed in Hell, and no one seems to know why.

Uncle Sam assembles another big stick for Iran, the radical leftwing networks in Minnesota continue to get exposed, silver shatters, two state Democrats get clipped in separate forgery cases, the rise of the Amelia memes, Microsoft update breaks everything (again), and are malls actually reviving?

And Neville Roy Singham’s fingerprints are visible everywhere.

It’s the Friday LinkSwarm!

As of right this moment, America hasn’t gone kinetic on the Mullahs yet, but we’re assembling an awful big stick.

USS Abraham Lincoln has gone dark, with no transponder or communication, signaling possible preparation for action against Iran.

A third US carrier strike group, USS George H.W. Bush (CVN-77), is moving into the Middle East theater.

Snip.

Some very interesting developments in the last 48 hours indicate something big is about to happen.

The EU all of a sudden has decided the next thing on their agenda is to declare the IRGC a terrorist group. Curious timing, that.

Minnesota agitators, including elected officials, have been organizing efforts to stalk, harass, and even hunt ICE agents in a Signal group chat that was infiltrated by Cam Higby and others.

It has been insane looking at the messages and the actual people involved.

And now DataRepublican has the donor list … you know, the people actually paying to make sure this all happens.

DataRepublican has also helpfully linked to their social media profiles.

You can download he data yourself. And DataRepublican has already turned in all the captured information to the Feds…

This is the story of how Minnesota became a political laboratory—first for the 2020 George Floyd protests, then for a sustained campaign against federal immigration enforcement. The players are the same. The money flows through familiar channels. And the strategy, according to those who designed it, was always meant to be replicated.

Snip.

Understanding how The People’s Forum operates requires following the money. And the money leads to Shanghai.

Neville Roy Singham is an American tech entrepreneur who sold his software company, ThoughtWorks, for approximately $785 million in 2017. He now lives in Shanghai, where, according to a 2023 New York Times investigation, he “works closely with the Chinese government media machine and finances propaganda worldwide.”

The Network Contagion Research Institute (NCRI), a Rutgers University-affiliated research organization, published a comprehensive report in May 2024 documenting what it calls the “Singham Network”—a web of nonprofits, fiscal sponsors, and alternative media outlets that share funding, personnel, and messaging.

According to NCRI, The People’s Forum received over $20 million from Singham and his wife, Jodie Evans (co-founder of the anti-war group CODEPINK), between 2017 and 2022. The money moved through a complex network of donor-advised funds and shell companies, including the Justice and Education Fund, the United Community Fund, and the Goldman Sachs Philanthropy Fund.

The People’s Forum has acknowledged receiving Singham funding. In a December 21, 2021 post on X (then Twitter), the organization defended its financial relationship with Singham against critics.

Congressional investigators have taken notice. On September 4, 2025, House Ways and Means Committee Chairman Jason Smith sent a formal letter to [People’s Forum Executive Director Manolo] De Los Santos demanding records and alleging that The People’s Forum had “acted as a foreign agent of the Chinese Communist Party” while enjoying tax-exempt status.

“Public reporting suggests that The People’s Forum has received over $20 million from Mr. Singham and his wife,” Smith wrote. “Multiple reports have found that The People’s Forum is part of Mr. Singham’s network of non-profit organizations that serve as his conduits to spread pro-CCP narratives.”

The Senate Judiciary Committee separately requested that the Department of Justice investigate whether The People’s Forum should register under the Foreign Agents Registration Act.

De Los Santos himself has deep ties to Cuba. According to his biography at the Black Alliance for Peace, he “was based out of Cuba for many years” and “worked toward building international networks of people’s movements and organizations.” The New York Post reported that De Los Santos first traveled to Cuba in 2006 and was there as recently as March 2024. He has been photographed meeting with Cuban President Miguel Díaz-Canel.

Footnotes excised. Snip.

What makes Minnesota different from other immigration flashpoints is the degree to which organizers have been explicit about their strategy.

The NCRI report notes that activists in the Singham network view the 2020 protests as proof that “the ability for mass struggle now exists inside the United States.” This framing treats George Floyd’s death not as a singular tragedy but as a tactical validation—evidence that the right combination of outrage, infrastructure, and outside support can produce transformational results.

De Los Santos’s April 2024 call to recreate “the violent protests of the summer of 2020” was not a slip of the tongue. It was a statement of doctrine.

The IDN’s establishment before Operation Metro Surge began—funded by nearly $1 million from the Bush Foundation—demonstrates pre-positioning rather than organic response. The explicit training of thousands in “rapid response” and “legal observation” tactics, the encrypted communication networks, the coordinated media strategies: none of this materialized spontaneously after Good’s death.

It was waiting.

The evidence assembled here—from congressional investigations, foundation records, tax filings, academic research, and organizers’ own statements—establishes that what is happening in Minnesota is neither spontaneous nor accidental.

The same network that helped turn George Floyd’s death into a national uprising has spent five years building the capacity to do it again. They have studied what worked in 2020, professionalized their operations, secured substantial funding, and pre-positioned infrastructure across Minnesota.

When Renée Good was killed on a Minneapolis street, that infrastructure activated precisely as designed.

Minnesota was chosen—first as the place where 2020 proved the model, then as the laboratory where that model would be refined and redeployed. The current crisis is not an accident of geography or politics.

A collection of far-left groups — led by a Communist activist network tied to CCP-linked millionaire Marxist Neville Roy Singham — is attempting to organize a nationwide anti-ICE school and business shutdown, with anti-Israel activist Linda Sarsour declaring that “we will bring this country to a halt.”

The general strike effort, scheduled for this Friday, is an attempt to replicate a Minnesota-wide anti-ICE shutdown which occurred last Friday and which was organized by many of the same far-left groups — but now with designs to do so on a national scale. The planned “National Shutdown” announced early this week includes plans for large-scale marches and a day of “no work, no school, no shopping” around the country.

The Manhattan-based Marxist revolutionary People’s Forum, the left-wing BreakThrough News media outlet, the Party for Socialism and Liberation (PSL), the far-left Code Pink anti-war group, and the Act Now to Stop War and End Racism (ANSWER) Coalition are all involved in either promoting or organizing the nationwide shutdown effort.

Just the News recently reported on how the forum, its propaganda machine, and the PSL were key players in pushing last week’s Minnesota-focused shutdown effort. Just the News also previously reported on how these and other radical activist groups have leadership links or financial ties to the funding network backed by Singham, whom others in his network call “Comrade.”

Social media used as organizing platform

The plans for Friday allegedly started with calls by a number of student groups at the University of Minnesota — the Somali Student Association, the Liberian Student Association, the Ethiopian Student Association, and the Black Student Union — who called for “Justice for Alex Pretti & Renee Nicole Good — NATIONWIDE SHUTDOWN” on Instagram on Sunday.

An investigation by Just the News shows that the forum was likely involved in creating the “National Shutdown” website which is now serving as an organizational hub for the coming Friday strike.

Did anyone notice a “nationwide shutdown” today? Mother Nature did a 100,000% better job shutting things down with Winter Storm Fern…

You gotta hand it to those Soros-sponsored district attorneys across the nation because when it comes to playing with fire, they play like they’ve never been burned.

The latest example is Philadelphia DA Larry Krasner. Not exactly a household name across the country,

But one that should be well-known to BattleSwarm readers.

Soros-linked groups have been his single largest financial backing source — helping him bypass traditional party fundraising and local contribution limits.

About a decade ago, Soros contributed about $1.7 million to the Philadelphia Justice and Public Safety PAC while Krasner was still a relative unknown in a seven-candidate race for district attorney. The Philly PAC is part of Soros’s nationwide Justice and Public Safety groups that fund “progressive” DAs in blue city contests.

According to public sources, in 2017, Soros’s donation to just one candidate accounted for nearly 30% of all campaign spending in the seven-person race. For his 2021 reelection, Soros groups gave Krasner another $1.2 million, including $259,000 for Philadelphia Justice and Public Safety PAC to run ads on Krasner’s behalf. Soros supported Krasner again last year, although I wasn’t able to find the dollar amounts before going to press.

Prior to getting all that Soros money to run for D.A., Krasner defended Black Lives Matter and Occupy Philadelphia members in court — and let’s just say Soros got his money’s worth. Or maybe it’s our money, given how intermingled Soros’s private funds are with taxpayer-funded NGOs purpose-tuned to push his causes.

Snip.

Here’s the quick and dirty transcript of Krasner talking about ICE officers: “This is a small bunch of wannabe Nazis — that’s what they are — in a country of 350 million. We outnumber them… If we have to hunt you down the way they hunted down Nazis for decades, we will find your identities, we will find you, we will achieve justice.”

What have I been repeating since the first attempt on President Donald Trump’s life last summer?

The left paints its enemies — we are no longer mere political rivals — as enemies, over and over, until some crazy decides to take justice into his own hands.

The FBI raided a Fulton County election office, evidently looking for evidence of the elction fraud carried out against president Trump in 2020. And it might be connected to…Nicolas Maduro?

Silver prices just plunged plunged over $30 an ounce today after a huge run-up. This means I’m either a genius when I sold a small amount of it last week (when prices were above where they are now), or an idiot for not selling all of it…

For three years, the world has waited for the Russian economy to implode. Instead, we watched a “Kalashnikov economy” defy gravity, fueled by high oil prices and a “friendship without limits” with Beijing. But as of January 2026, the gravity of basic math has finally caught up with Vladimir Putin.

The catalyst isn’t just the stalemate on the front lines; it’s a legislative “kill shot” from Washington and a quiet betrayal from the East. Between the new Graham-Trump Sanctioning Russia Act and a mounting domestic liquidity crisis, the Kremlin isn’t just running out of options—it’s running out of time.

The most significant development of 2026 isn’t a new missile system; it’s a tariff. The Graham-Trump Bill, greenlit by the White House on January 7, has fundamentally rewritten the rules of economic warfare. By threatening a mandatory 500% tariff on any country—including China and India—that continues to purchase Russian petroleum or uranium, the U.S. has finally weaponized the one thing Russia’s allies value more than cheap crude: access to the American consumer.

The shockwaves were instantaneous. On January 15, reports emerged that China’s largest state banks, including ICBC and Bank of China, began halting Ruble-denominated settlements. They aren’t waiting for the bill to be signed into law; they are pre-emptively cutting Russia loose to save their own export margins. When Beijing chooses its $500 billion trade surplus with the U.S. over its “strategic partner” in Moscow, the Russian war machine loses its primary life support system.

While the external walls are closing in, the internal floor is rotting. On New Year’s Day, Russia’s VAT officially jumped to 22%. This isn’t a sign of strength; it’s an act of desperation. The Kremlin is cannibalizing its own middle class to plug a federal budget revenue gap that fell 20% short of targets in 2025.

We are now seeing the first signs of a systemic banking fracture. In cities like Yekaterinburg and Novosibirsk, reports of ATM shortages are no longer fringe rumors—they are the physical manifestation of a “liquidity trap.” When the state raises taxes while inflation remains double-digit and interest rates hover near 20%, the result is a “medically induced coma” for the civilian economy.

Federal officials have charged two contractors with conspiring to disrupt Immigration and Customs Enforcement officers in Knoxville earlier this month.

The U.S. Attorney’s Office for the Eastern District of Tennessee unsealed a multi-count indictment on Friday against Tyler Shane Wells, 33, of Morristown, and 18-year-old Alexander Bonilla Servin of Smyrna.

They are charged with conspiracy to conceal and harbor illegal aliens, conspiracy to forcibly impede federal agents while engaged in performance of official duties, and conspiracy to prevent, by force, intimidation, or threat, federal agents from discharging their official duties from January 5 through January 13.

Bonilla-Servin is also charged with forcibly impeding federal agents engaged in the performance of their official duties.

Wells appeared in court on Friday and pleaded not guilty to the charges and a detention hearing is set for Monday. A trial date has been set for March 31, 2026.

Federal authorities accuse the two of plotting to block the entrance to a Hardin Valley construction site with Bonilla-Servin’s pickup truck in an effort to impede ICE agents. According to a Department of Justice release, the vehicle was put in position after federal agents were seen surveilling the site. Servin is also accused of hitting agents’ vehicle with the truck as it attempted to enter the site on January 13.

After more than a year of digging, Statehouse candidate Bailey Templeton’s most public records collection shows 1,085 Illinois children under 18 without SSNs had Medicaid bills of $66 million in 2025. That’s up 725% from $8 million for 450 children in 2021.

“It’s roughly $40 million spent on inpatient treatment, that’s a lot of time for children to be in hospitals,” Templeton told The Center Square Friday.

The data only generates more questions for Templeton.

“It raises questions about what would be called medical trafficking, where things are conducted on to children when they’re too young to be able to consent to these things,” she said.

Why, it’s almost like Democrats imported millions of illegal aliens and put them on welfare rolls…

Man tries to kill mayor in the Philippines with an RPG. (Never mind that The Sun calls it a bazooka.)

Idiot Hawaiian Democrat Senator Brian Schatz asks Marco Rubio a really stupid question, and Rubio hands him his ass:

“That’s statutory. The Helms Burton Act, the US embargo on Cuba, is codified. It was codified in law and it requires regime change in order for us to lift the embargo.”

Transportation Secretary Sean Duffy just dropped what I’ve been calling the nuclear option.

In an appearance on Katie Pavlich Tonight Thursday, Duffy made clear that withholding $200 million in federal funding isn’t the end of this fight. If California doesn’t come into compliance on the non-domiciled CDL issue, Duffy said, “we will eventually pull their ability to issue commercial driver’s licenses to anybody in California.”

Not just the 17,000 non-domiciled CDLs at the center of this fight. Every single CDL in the state.

I’ve written extensively about this standoff since the FMCSA released its audit findings last September, which showed that roughly 25% of California’s non-domiciled CDLs were improperly issued. I’ve covered the $160 million funding hit. I’ve warned about the decertification authority in 49 U.S.C. 31312 and 49 CFR 384.405, which most people in this industry didn’t even know existed.

This didn’t start with the Trump administration’s September 2025 emergency rule restricting non-domiciled CDLs to certain visa categories. That rule, which limited eligibility to H-2A, H-2B, and E-2 visa holders, has been stayed by the D.C. Circuit since November. The court found that petitioners were “likely to succeed” on their claims that the FMCSA violated federal law in its rulemaking.

The California problem predates all of that.

FMCSA’s August 2025 Annual Program Review found California had been violating federal regulations that existed long before Duffy took office. The state was issuing CDLs with expiration dates extending years beyond drivers’ lawful presence documentation. In one case that still makes my blood boil, California issued a driver from Brazil a CDL with passenger and school bus endorsements that remained valid months after his legal presence expired.

That’s not a new rule problem. That’s a California screwed-up problem.

California agreed in November to revoke all 17,000 improperly issued licenses by January 5, 2026. Then, on December 30, the California DMV unilaterally announced a 60-day extension to March 6, citing the need to ensure it doesn’t wrongfully terminate licenses for drivers who actually qualify.

Duffy’s response on X was blunt: “Gavin Newsom is lying.”

FMCSA never agreed to the extension. California proceeded anyway. On January 7, DOT made good on its threat and withheld approximately $160 million in National Highway Performance Program and Surface Transportation Block Grant funds. That’s on top of the $40 million already withheld over California’s refusal to enforce English language proficiency requirements.

California has more than 700,000 CDL holders. The state is home to the nation’s largest trucking workforce, with over 138,000 truck drivers moving freight through the ports of Los Angeles and Long Beach, the agricultural heartland of the Central Valley, and every retail distribution center feeding the country’s largest consumer market.

Under full decertification, California would be prohibited from issuing, renewing, transferring, or upgrading any commercial learner’s permits or commercial driver’s licenses until FMCSA determines the state has corrected its deficiencies. Previously issued CDLs would technically remain valid until their stated expiration dates, but here’s where it gets ugly.

Other states could refuse to recognize California credentials during the noncompliance period. FMCSA could issue guidance declaring CDLs issued by a noncompliant state invalid for interstate commerce. The Commercial Driver’s License Information System, which enables interstate verification, could flag every California license.

For the 700,000 CDL holders in the Golden State, decertification wouldn’t just be an administrative headache.

It would effectively ground them from operating in interstate commerce.

Blue state governors should stop trying to protect their precious illegal aliens and start following federal law.

TikTok has finalized a deal to create a new American entity, avoiding the looming threat of a ban in the United States that has been in discussion for years on the platform now used by more than 200 million Americans.

The social video platform company signed agreements with major investors including Oracle, Silver Lake and the Emirati investment firm MGX to form the new TikTok U.S. joint venture. The new version will operate under “defined safeguards that protect national security through comprehensive data protections, algorithm security, content moderation and software assurances for U.S. users,” the company said in a statement Thursday. American TikTok users can continue using the same app.

Tesla North America announced the completion of a major lithium refinery in Robstown, Texas, with Elon Musk calling it “the most advanced lithium refinery in the world.”

Robstown is just west of Corpus Christi.

In the promotion video, Jason Bevon, the site manager at the Gulf Coast lithium refinery, explains that the refining process used in Robstown is “inherently much more environmentally friendly.” The company claims that the process used by the refinery eliminates hazardous byproducts of the refining process and is more sustainable than traditional methods.

Bevon explained that the refinery “enables us to have access to the critical minerals for energy storage, for battery manufacturing, and ultimately for [electric vehicle (EV)] growth.”

“It enables us to accelerate Tesla’s mission by regionalizing supply chains for battery minerals and materials, by providing jobs, by cutting emissions from the transportation network that is required for these supply chains.”

“It really allows us to usher in energy independence for North America.”

Columbia University’s Center on Global Energy Policy explains that raw lithium needs to be processed into a “chemical in the form of lithium carbonate or lithium hydroxide, before being used in batteries,” which is done through refining. Currently, China dominates the global trade and production of key minerals, and leads the world in lithium refinement capabilities.

The need for lithium batteries has grown exponentially in recent years, with lithium batteries being required for EVs, smartphones, laptops, and renewable energy receptacles such as solar panels.

Also, you’re partially paying for it:

This political shift and the operation of the refinery are complemented by recent grants through the Texas Semiconductor Innovation Fund (TSIF), which was established when the Texas CHIPS Act, House Bill 5174, was signed into law in 2023. The TSIF totals “approximately $948 million in total appropriations” and is used for “semiconductor manufacturing and design,” according to the Texas Economic Development and Tourism Office.

Webb County’s sheriff and his assistant chief are facing federal charges for allegedly using office resources to create and profit from a disinfecting business during the COVID-19 pandemic.

Sheriff Martin Cuellar Jr., 67, and Assistant Chief Alejandro Gutierrez, 47, have both appeared before a federal grand jury after turning themselves in. Their indictments have now been unsealed, revealing that they both are accused of misappropriating Webb County Sheriff’s Office funds between 2020 and 2022.

Cuellar is the brother of U.S. Rep. Henry Cuellar (D-Laredo).

According to the indictment, around April 2020 Cuellar opened a for-profit business called Disinfectant Pro Master (DPM), which used resources belonging to the WCSO. He reportedly enlisted Gutierrez and Ricardo Rodriguez, an assistant chief, to assist in the start of the venture that provided disinfecting services to local businesses, residents, and the local school district.

Federal prosecutors allege none of the three made any personal investments in the startup company but used county resources, vehicles, and equipment. DPM also reportedly used county funds on multiple occasions to purchase supplies for the company. Staff from the sheriff’s office were often utilized to conduct the company’s operations during their regularly scheduled shifts according to the indictment.

The indictment also claims records show that payroll was not ever issued from the company to compensate the staff that was utilized to carry out its business.

During its operation, DPM received multiple contracts with local businesses, including a $500,000 contract with the United Independent School District, where Rodriguez served on the school board.

The company eventually closed in August 2022 after UISD did not renew its contract following media coverage and public scrutiny at a school board meeting over the contract being awarded to a board member’s company.

During the duration of the company’s operation, Cuellar, Gutierrez, and Rodriguez each reportedly received over $175,000. It is alleged in the indictment that Cuellar used his revenue to purchase a 10-acre property in Laredo.

As you might expect, Martin Cuellar is a Democrat.

Dwight documents not one but two of state-level Democrat congresscritters (state rep Ayshia “Ajay” Pittman in Oklahoma and former state senator Sonya Jaquez Lewis in Colorado) being involved in forgery scandals.

Nose-ringed leftist “Grace Carol Brown is charged with arson and burglary, and is ‘accused of smashing an exterior window, unlawfully entering the Comal County (TX) Republican Party headquarters, and starting a deliberate fire inside the building’ overnight on January 13/14.”

Oh, for fuck’s sake! “Parents say their trans son killed himself because his church employer wouldn’t let him wear French maid outfit, cat ears.”

Simon Whistler on Every Saudi Gigaproject in Vision 2030. Neom is still a ridiculous pipe dream, and Whistler is far too easily impressed with “zero carbon” claims, but some of these projects are actually worth doing and on-track.

Keir Starmer’s Labour government created the character of Amelia, a purple-haired nationalist Goth girl, for a lame Flash-style game to “combat far right extremism” (i.e., anyone who objects to importing illegal alien Islamist rapists into the UK), but now that she’s been adopted and memed by the right, that move backfired big time.

Louis Rossmann reports that downgrading to an earlier operating system bricks the latest OnePlus Android phone. I’d never heard of OnePlus, but it turns out it’s a Chinese brand, so you shouldn’t be buying it in the first place…

Surprise! American shopping malls aren’t dying off.

Shopping malls, long an economic and cultural fixture of American life, are facing sustained pressure but are not disappearing altogether.

Instead, the sector is undergoing creative destruction, as traditional mall formats give way to new concepts that reflect shifting consumer behavior and market conditions, according to recent industry data.

A research report by Capital One Shopping (COS) outlines the magnitude of the challenge facing the mall sector, citing rising mall closures that remain vacant for an average of nearly four years, as well as vacancy rates that are 112 percent higher than the overall retail vacancy rate.

COS also estimates that as many as 87 percent of large shopping malls could close over the next decade.

At the same time, COS data indicate a reversal of earlier trends. From 2021 through 2025, mall openings exceeded mall closures, suggesting adaptation rather than terminal decline. In 2025 alone, 9,410 new mall stores opened, nearly double the number that closed.

Additional evidence of revival appears in a recent article published by Growth Factor. Author Clyde Christian Anderson reported that indoor mall foot traffic in March 2024 rose 9.7 percent year over year, open-air shopping center traffic increased 10.1 percent, and outlet mall traffic climbed 10.7 percent—each exceeding pre-COVID-19 pandemic levels.

Every book I bought in 2025, most from early in the year when I still had a contract job and money in the bank…

Happy Halloween! Biden’s FBI turned January 6 investigations into a vast monitoring program aimed at Republicans, the Schumer Shutdown continues, a whole of disturbing illegal alien sex offenders, Milei wins again in Argentina, Russian floating crane does what Russian ships do best, the autopen scandal deepens, and one really weird gun.

It’s the Friday LinkSwarm!

Arctic Frost was an operation by the Biden FBI to use the half-assed January 6 riot to turn the federal government into a Stasi aimed at Republicans, including “Nearly 200 Subpoenas Targeting 400 GOP-Linked Individuals, Entities.”

The Biden-era FBI’s “Arctic Frost” investigation into President Trump and the broader GOP’s role in the January 6, 2021 Capitol riot was more wide-ranging than previously known, according to newly released documents showing the bureau issued nearly 200 subpoenas targeting more than 400 Republican entities and individuals as part of the probe.

Senator Chuck Grassley (R., Iowa) released records on Wednesday showing 197 subpoenas were issued to individuals and businesses during the FBI’s “Arctic Frost” investigation targeting 430 GOP individuals and entities. He obtained the records through protected whistleblower disclosures.

Financial institutions, Trump-aligned political organizations and operatives, conservative think tanks, and payroll companies were among the subpoena recipients, according to a list compiled by the Senate Judiciary Committee. Federal investigators sought communications between the targeted individuals and media companies, prominent Trump-world officials, and legislative staff. The investigative efforts also encompassed MAGA fundraising efforts and donors.

Several GOP members of the Senate Judiciary Committee, the panel Grassley leads as chairman, spoke at a press conference Wednesday afternoon unveiling the new information.

“What is revealed in those 1700 pages of documents, those 197 subpoenas, is nothing short of a Biden administration enemies list,” Senator Ron Johnson (R., Wis.) said.

ohnson said he knew most of the 38 individuals from his state on the Biden administration’s “enemies list” and urged his fellow lawmakers to assist the Trump administration with getting to the bottom of the FBI’s conduct.

“This extended far beyond President Trump and extended to President Trump’s supporters not only here in the United States Senate but more broadly,” Senator John Cornyn (R., Texas) lamented.

“Merrick Garland was a member of Joe Biden’s cabinet. He was willing to do whatever Joe Biden and his political operation wanted him to do, including destroying President Trump,” Cornyn added.

The “Arctic Frost” investigation looked into the role President Trump played in the Capitol riot. The probe eventually morphed into special counsel Jack Smith’s Washington, D.C., criminal case against Trump. Then-Attorney General Merrick Garland and then-FBI Director Christopher Wray personally signed off on the investigation when it was launched in 2022, according to a decision memo Grassley divulged last week.

Snip.

A ninth GOP Senator, Ted Cruz of Texas, was also targeted during the “Arctic Frost” investigation, Axios first reported. Several of the GOP lawmakers in the FBI’s crosshairs promoted Trump’s false claims about the 2020 presidential election being stolen from him. The attempts by Trump’s allies to contest the 2020 election formed the basis of Smith’s D.C. criminal case and criminal prosecutions in the swing-states Trump lost to former President Biden. Numerous individuals targeted in “Arctic Frost” later faced criminal charges for their failed attempts to overturn the 2020 election results.

“Jack Smith was a fundamentally corrupt prosecutor. This was a political enemies list from the beginning,” Cruz said. “This is an executive who believes it is justified spying on their opponents in the legislature because they convinced themselves the ends justified the means.”

Smith attempted to subpoena AT&T to obtain Cruz’s cellphone communications and the company’s legal counsel declined to comply, Cruz said. He praised the company for standing its ground against Smith’s attempt to gain his phone records. Cruz said that Washington, D.C., federal Judge James Boasberg signed an order prohibiting AT&T from informing Cruz of the subpoena for a year because of the potential for Cruz to destroy evidence or intimidate witnesses.

And Cruz has sent me three fundraising emails based on it this week alone.

Victory in Portland. “Antifa Retreats From Portland ICE Facility After Police Dismantle Encampment.”

The decentralized anti-fascist warriors in the Portland-area cell, aligned with the radical Democratic Party, were in full retreat overnight after officers from the Portland Police Department cleared out their encampment in front of the Immigration and Customs Enforcement facility in the Portland metro area.

Nick Shirley, who is an independent journalist and who met with President Trump at the White House earlier this month for a round table on Antifa, wrote on X, “ANTIFA HAS BEEN DISMANTLED IN PORTLAND After 140 days of controlling and camping on this street in Portland, Antifa has officially been cleared out as the police FINALLY stepped in and cleared the encampment.”

“Inside the encampment, they had loads full of medicine, medical gear, party supplies, a fridge, BBQ, etc ANTIFA’s 140 days of control have officially come to an end,” Shirley said, with an accompanying video showing inside the encampment that housed gender-confused purple-haired people who hate the Western world and capitalism.

Federal Reserve drops interest rates by a quarter point. Feel the excitement…

Democrats have badly weakened their party with left-leaning ideas and rhetoric, growing only with self-described “white liberals” while losing ground with other voters, according to a new center-left group’s report shared first with Semafor.

The group, called Welcome, consulted hundreds of thousands of voters over six months for its broad findings, including that 70% of voters think the Democratic Party is “out of touch.” Most voters, the group found, believe the party over-prioritizes issues like “protecting the rights of LGBTQ+ Americans,” and “fighting climate change” while not caring about “securing the border” or “lowering the rate of crime.” (Welcome began as a PAC in 2022, then founded a nonprofit with the same name for political research.)

Elected Democrats will receive copies of the report after its Monday publication, followed by events to promote it in DC and New York. The report urges party members to abandon some of the progressive language about race, abortion, and LGBTQ issues that Democrats began using after the 2012 election — and recommends the nomination of more candidates willing to vote with Republicans on conservative immigration and crime bills.

“The Democratic Party had better listen — for the good of our nation,” former Illinois Rep. Cheri Bustos, who ran the party’s House campaign committee when it lost seats in 2020, wrote in her endorsement of the report.

Inspired by The Politics of Evasion, an influential 1989 paper that inspired the party’s more centrist shift under Bill Clinton, the 70-page Deciding to Win document argues that Democrats must be “willing to break with unpopular party orthodoxies.” Its prescription for getting the party out of its current wilderness isn’t simple: avoidance of “both a pivot to corporate centrism and the pursuit of progressive ideology purity.”

Greg Schultz, who managed Joe Biden’s 2020 primary campaign but was replaced for the general election, worked with Welcome to shape the report.

“For the last 20 years, Democrats have just misunderstood how you actually win elections,” he told Semafor. “I thought Biden had proven in the 2020 primary that the base of the Democratic Party is a 58-year old woman without a college degree. But when you hear people in DC say ‘the base,’ they mean white intellectuals that live in a few coastal cities.”

The report directly challenges Democrats’ predilection for the interests of “highly educated and affluent voters,” arguing that their influence “may be responsible” for the party’s closer association with left-wing politics.

Sort of sounds like Weigel’s friends are finally noticing what Republicans were saying at least as far back as Obama’s first term. But wait!

“We have much to learn from the relentless focus of Bernie Sanders, Alexandria Ocasio-Cortez, and Zohran Mamdani” on those fronts, the authors write.

The risk they see is in Democrats moving left on other progressive policies, which even some in the party establishment have done while criticizing Mamdani and other democratic socialists. From 2013 to 2024, between the beginning of Barack Obama’s second term and the end of Joe Biden’s sole term, the report offers clear metrics to show how the party changed its language and gave support to left-wing bills that had little chance of passage.

So they only want the Democrat Party to be a little bit pregnant with socialism and social justice. Yeah, good luck with that, heretic. (Hat tip: Stephen Green at Instapundit.)

Two rogue Democrat judges think they can bypass the executive and judiciary branches and order specific programs funded during the Schumer Shutdown. “On Friday, US District Judge John McConnell of Rhode Island announced that he would order the US Department of Agriculture to distribute a pool of contingency funds ‘as soon as possible.’ While minutes before, Boston US District Judge Indira Talwani ruled that the US government must announce by Nov. 3 whether they would authorize at least partial funding for the program using around $6 billion in contingency funds – and if so, when will they do it.”

Mexican authorities in August, with the use of DNI intelligence, captured an infamous human trafficker who would lure pregnant women to steal their babies and organs.

She would then sell the stolen babies and organs on both sides of the border, which is how the United States got involved.

Aguilar was part of the Jalisco New Generation drug cartel.

California Democratic Gov. Gavin Newsom’s pimp shield law, pushed by Democratic legislator Rep. Scott Weiner, has helped foster a disturbing new sex market on Figueroa Street in Los Angeles, featuring prostitutes as young as 12 and 13 years old. For far too long, the “kiddie stroll,” as it’s known, has gone unreported because major media outlets refused to cover it, allowing it to flourish under the watch of Democratic politicians.

But now it’s time to shine a light in the darkness and expose the truth about what’s happening to these poor young girls and why nothing has been done to bring the harrowing evil to an end.

An article from the New York Times Magazine is finally covering this horrific scene in Los Angeles, though they’ve conveniently neglected to cover anything concerning the prostitution law Newsom’s administration passed.

“For the 77th Street Division, which covers the northern half of the Figueroa Corridor, prostitution had always been a problem. But in recent years, the officers had seen the magnitude of child sex trafficking explode,” wrote reporter Emily Baumgaertner Nunn.

“Gangs that had long sold drugs began to take advantage of Figueroa’s lucrative opportunity. With a dozen girls, one trafficker could easily make $12,000 a night. ‘Drugs are sold once and gone forever, but girls can be resold indefinitely,’ said [police sergeant Alvaro] Navarro, who had been in the division for two decades. Motel owners who noticed the parades of customers but feared the gangs’ retribution kept quiet,” Nunn continues.

There’s little doubt that much of the silence and fear of gang retaliation for speaking out against this vile form of human trafficking stems from the lack of police presence on California streets, particularly in Los Angeles. Democrats in the state slashed funding for police and tied officers’ hands, making it harder to pull these girls — who are just children — out of sex trafficking.

In fact, Nunn points out that the sex-trafficking unit in the city was disbanded due to budget cuts, which means each division within the police department has fewer resources available to tackle the issue. There are supposed to be a total of six investigators looking into human trafficking. Now there’s only one.

Children suffer abuse in ways too sick and twisted to imagine, and thanks to anti-cop policies from radical leftists trying to appease minorities for votes, leaders ignore it instead of acting. This is truly a miscarriage of justice. It’s immoral and evil.

“Their jobs grew even more challenging when California repealed the law allowing the police to arrest women who loitered with the intent to engage in prostitution. The repeal, known as SB 357, was intended to prevent profiling of Black, brown, and trans women based on how they dressed. But when it was implemented in January 2023, the effect was that uniformed officers could no longer apprehend groups of girls in lingerie on Figueroa, hoping to recover minors among them.

Now officers needed to be willing to swear they had reason to suspect each girl was underage — but with fake eyelashes and wigs, it was nearly impossible to tell. One girl told vice officers that her trafficker had explained things succinctly: ‘We run Figueroa now,’ he said,” Nunn writes in her article.

By the end of 2023, the city attorney started referring to Figueroa as the “Kiddie Stroll” because many of the girls working the street were under 13.

The Democrat Party is now objectively pro-rape and pro-pedophilia.

“ICE continues arresting ‘worst of the worst‘ illegal migrants accused of sexual crimes.”

The Department of Homeland Security (DHS) on Tuesday told Just The News exclusively that Immigration and Customs Enforcement (ICE) officials are continuing to arrest the “worst of the worst” illegal migrants, despite a government shutdown.

The latest arrests include illegal migrants who have been convicted of crimes such as lewd and lascivious acts on a minor, aggravated criminal sexual assault with bodily harm, aggravated kidnapping and possession with the intent to distribute.

Monday’s arrests include a Cuban illegal migrant in Florida who was convicted of lewd and lascivious act on a minor, a criminal illegal migrant from Mexico, convicted of aggravated criminal sexual assault with bodily harm, and aggravated kidnapping in Illinois, and an illegal migrant in Tennessee who was convicted of sexual assault.

“Nothing—not even the Democrats’ government shutdown—will slow us down from arresting the worst of the worst criminal illegal aliens,” Assistant DHS Secretary Tricia McLaughlin said in a statement. “Yesterday, the brave men and women of ICE arrested pedophiles, rapists, and kidnappers. These are the types of predators ICE is taking off of America’s streets every single day. DHS will stop at nothing to make America safe again and remove these violent illegal offenders from our streets.”

Another illegal migrant from Mexico, identified as Adan Martinez-Gonzalez, was arrested in Texas after being convicted of aggravated kidnapping. Mexican illegal migrant Nicanor Hernandez-Gutierrez was apprehended by ICE and was previously convicted of possession with intent to distribute a quantity exceeding five kilograms of cocaine.

Former DOE nuclear engineer Matt Von Swol notices something that’s been floating around for years; the insane number of minorities (mexicans and blacks) who are booked as “WHITE” when they get arrested – something which obviously manipulates ‘inconvenient’ crime stats – something that TPUSA’s Andrew Kolvet noted have been “widely corrupted to serve a racist agenda.’

“I searched through thousands of arrests in my county and every single Hispanic individual who has been arrested is labelled as “WHITE”” Van Swol posted on X.

We cannot trust crime stats in America. They have been widely corrupted to serve a racist agenda. https://t.co/UEpwDbnv2F

It’s axiomatic in Washington, D.C., that changes that are undertaken by administrative action alone are easy to reverse.

There’s no doubt that if a Democratic president wins next time, he or she will undo much of what Trump has done through executive action, but will he or she be able to take it all the way back to where it was before?

I don’t think so. It will certainly be goodbye to the Gulf of America and the Department of War, and ICE raids will stop immediately. But Trump has struck blows against long-standing progressive priorities that were pursued in a piecemeal fashion, meant to build up and become irreversible over time. On these, it will be hard for the left to recover — in other words, Trump has broken the progressive ratchet.

How does the ratchet work? It begins with small, unobjectionable, or perhaps even salutary steps, coupled with assurances that potential downsides or extreme outcomes will never come about. Then, over time, incremental moves are made in the same direction until the unreasonable policy that we’d been assured would never happen is entrenched reality.

It is the work of decades, and it depends on no one ever pushing things back in the other direction (that would be reactionary) and everyone’s accepting the endpoint as a fait accompli.

To wit: First, women flying in combat roles. Then, women in ground combat roles, with the proviso that training and standards will stay the same. Then, gender-normed physical fitness tests and lower standards for everyone.

First, race-neutral civil rights laws, then temporary affirmative action, then permanent quotas and set-asides, then a widespread corporate and educational architecture devoted to promoting racialist practices and ideology.

First, respect and rights for gay people, then respect and rights for trans people, then everyone in America having to designate their pronouns, people getting shamed and fired for “misgendering” trans people, “gender-affirming” surgeries for minors, males competing in female sports, and the active encouragement of nonconforming sexual identities in the schools.

Trump has yanked the other way so far on these ratchet issues that it’s not clear when or how the left can get them back to the status quo ante.

It took so long to get there in the first place that snapping back to politicized training standards, pervasive DEI, or the most outlandish forms of the trans agenda will be very difficult.

Also, the sense of inevitability that the ratchet created, and the sense of helplessness on the part of opponents, has now been shattered.

Finally, there’s the problem that plausible deniability has been lost. The ratchet allowed for radical social change to be sheathed in incrementalism and in the righteousness of the starting point — DEI was on a continuum with civil rights; watered-down physical standards on a continuum with the inclusion of women in combat roles who needed no special accommodation.

Now, a revanchist Democratic administration would have to proceed directly to the most controversial and unpopular parts of the left’s agenda.

Top Biden administration officials misused executive authority and took actions without then-President Joe Biden’s authorization as his mental acuity declined, a House investigation found.

President Biden’s inner circle hid the extent of his mental decline from the American people and exercised executive authority by abusing the presidential autopen and taking advantage of a lax chain-of-command, according to a report released Tuesday by the House Oversight Committee.

“The Biden Autopen Presidency ranks among the greatest scandals in U.S. history. As President Biden declined, his staff abused the autopen and a lax chain-of-command policy to effect executive actions that lack any documentation of whether they were in fact authorized,” the report reads.

“The Committee has found that there was, in fact, a cover-up of the president’s cognitive decline and that there is no record demonstrating President Biden himself made all of the executive decisions that were attributed to him,” the report adds.

The Biden White House worked to conceal the extent of his mental decline through scripted messaging, controlled public appearances, and limited access. Staffers controlled Biden’s daily activities, appearances, and workload to prevent the public from seeing his diminishing mental capacity, the report says.

For the most part, Biden’s staff dismissed the possibility that the American people were concerned about his mental faculties. In a similar manner, Biden’s staff attributed his disastrous June 2024 debate performance to a bad cold and minimized Biden’s struggles on that fateful night.

The Oversight Committee investigated the coverup of Biden’s mental capacity with a specific focus on the Biden administration’s autopen usage at the end of his term. According to the committee, Biden officials used presidential authority and initiated executive actions without direct authorization from Biden himself, including using the autopen to sign executive orders without written approval.

Top Biden administration officials misused executive authority and took actions without then-President Joe Biden’s authorization as his mental acuity declined, a House investigation found.

President Biden’s inner circle hid the extent of his mental decline from the American people and exercised executive authority by abusing the presidential autopen and taking advantage of a lax chain-of-command, according to a report released Tuesday by the House Oversight Committee.

“The Biden Autopen Presidency ranks among the greatest scandals in U.S. history. As President Biden declined, his staff abused the autopen and a lax chain-of-command policy to effect executive actions that lack any documentation of whether they were in fact authorized,” the report reads.

“The Committee has found that there was, in fact, a cover-up of the president’s cognitive decline and that there is no record demonstrating President Biden himself made all of the executive decisions that were attributed to him,” the report adds.

The Biden White House worked to conceal the extent of his mental decline through scripted messaging, controlled public appearances, and limited access. Staffers controlled Biden’s daily activities, appearances, and workload to prevent the public from seeing his diminishing mental capacity, the report says.

For the most part, Biden’s staff dismissed the possibility that the American people were concerned about his mental faculties. In a similar manner, Biden’s staff attributed his disastrous June 2024 debate performance to a bad cold and minimized Biden’s struggles on that fateful night.

The Oversight Committee investigated the coverup of Biden’s mental capacity with a specific focus on the Biden administration’s autopen usage at the end of his term. According to the committee, Biden officials used presidential authority and initiated executive actions without direct authorization from Biden himself, including using the autopen to sign executive orders without written approval.

National Review previously reported on internal emails showing the White House’s process for deciding on commutations for violent criminals was chaotic and insular. The Biden administration did not consult with the families of the victims of the violent criminals as part of its clemency process.

Another instance the report mentions is the pardons Biden issued in the final hours of his presidency to members of his family. No records exist for the in-person meeting that led to the decision to grant those pardons.

Rather, Zients verbally authorized the use of the autopen after an aide of his transmitted the decision to issue the pardons. Zients did not know who actually applied the autopen and did not confirm with President Biden that he approved the pardons. The aide sent an email on Zients’s behalf expressing approval of the Biden family pardons.

If Biden didn’t issue the pardon, the pardon is invalid.

Free marketeers have good reason to cheer, or at least sigh with relief, with Milei’s party doing well in the Argentinian midterm elections…

In the middle of the month, this newsletter explained why the Trump administration traded $20 billion in U.S. dollars for the equivalent amount in Argentinian pesos. The Argentinian currency, which had already lost a lot of its value, was dropping perilously over fears President Javier Milei’s party might lose the midterm elections and the country would revert to its previous reckless big-spending habits. The currency trade, spearheaded by U.S. Treasury Secretary Scott Bessent, represented an economic lifeline to Argentina and a metaphorical bet that Milei’s party would do well in the midterms, and keep the country on a smaller-government, more free-market-oriented path.

Secretary Bessent, collect your winnings. From the Wall Street Journal:

With nearly 99 percent of votes counted, Milei’s Freedom Advances party won almost 41 percent of the national vote, more than doubling its representation in Congress. That means his party and allies secured at least one-third of the seats in both chambers — the critical threshold that allows Milei to preserve his veto power and defend his sweeping decrees.

The result, stronger than most polls had predicted, gives Milei fresh political momentum after months of unrest over deep spending cuts and a grinding recession last year. It also shores up his standing with Washington and the International Monetary Fund, which have tied future financial support to the survival of his austerity experiment. Market analysts expect Argentine bonds and the peso to rally when trading opens Monday, reflecting relief that Milei still has political traction after taking office two years ago.

“Ukrainian drones hit the Mariysky oil refinery in Mari El, the Stavrolen chemical plant and the Novospasskoye oil depot.”

Greece sends Ukraine the big guns. “Greece is transferring 60 U.S.-made M110A2 203mm self-propelled howitzers to Ukraine, along with 150,000 shells and thousands of Zuni rockets.”

Finally: “Texas Higher Ed Board Officially Bans In-State Tuition for Illegal Aliens.” Rick Perry was a very conservative governor in many ways, but backing subsidized tuition for illegal aliens was one of his stupidest ideas.

Ken Paxton takes a scalp. “Dallas Doctor Surrenders License After Texas AG Sues For Prescribing Gender Transition Drugs To Minors.” “Paxton announced on Oct. 24 that Dr. May C. Lau has given up her state medical license but that the legal case over her alleged violation of Texas’s ban on gender transition treatment for minors is still ongoing.”

“California’s Retirement Fund Lost 71% Of $468M Investment In Clean Energy And Won’t Say How.” “According to state records analyzed by the Center Square, the CalPERS Clean Energy & Technology Fund (CETF), launched in 2007, has seen its value fall from a total commitment of $468.4 million to $138 million as of March 31, 2025. That represents a loss of more than $330 million, even after paying $22 million in fees and costs to private equity managers.” I’m sure the right pockets got lined. For Democrats, losing taxpayer money is ephemeral, but virtue signaling is forever.

Oklahoma: “State Rep. Ajay Pittman suspected of embezzling campaign funds, forgery, court records show.” Guess the party.

The Peace President keeps on winning. “President Trump participates in a peace treaty, trade and critical mineral agreement signing with the Prime Minister of the Kingdom of Cambodia and the Prime Minister of the Kingdom of Thailand.”

“A staffer for Democratic Massachusetts Gov. Maura Healey was hit with drug trafficking charges after authorities intercepted eight kilograms of cocaine being delivered to a state office building. LaMar Cook, who has served as deputy director of Healey’s western Massachusetts office since 2023, was charged with trafficking over 200 grams of cocaine, unlawful possession of a firearm, and unlawful possession of ammunition related to the bust, Hampden District Attorney Anthony Gulluni announced Wednesday. Multiple parcels containing about 21 kilograms of cocaine have been seized by Massachusetts State Police throughout the investigation into Cook.” Why yes, eight kilos of Peruvian Marching Powder is indeed more than 200 grams. Indeed, that’s the sort of quantity that might keep Hunter Biden supplied into the spring…

Biden’s autopen pardons are the gift that keeps giving. “Thirty-one-year-old Khyre Holbert—a convicted felon whose 20-year crack cocaine and firearm-possession sentence was commuted by former President Joe Biden at the end of his term—was slapped with a felon in possession of a firearm and ammunition charge following his alleged participation in a shooting in Omaha, Nebraska.”

Slam Frank is “Holocaust victim Anne Frank reimagined as a pansexual Latina with non-binary lover and neurodiverse family in controversial NYC musical.” Maybe NYC deserves Mamdani…

I had to disable the ancient Word Press Stats package that stopped working and was screwing up my dashboard. So I lost all my blog hit history, which is irksome, as I received more than five million hits. On the plus side, it seems to save drafts much more quickly, and it also seems to be recording more views than the old stats did. I also wonder if the old stat package was responsible for some of the slow load times people occasionally experienced.

This week: More Charlie Kirk assassination fallout, more Ukrainian oil infrastructure strikes, Fani Willis gets permabanned, Planned Parenthood want to trans your children, the Democrat party’s racism problem, Lina Hidalgo calls it quits, more of that voting fraud that doesn’t exist, and YouTube screws up, then refuses to admit it

Tyler Robinson, the alleged assassin of Charlie Kirk, was living with his transgender romantic partner in the leadup to the assassination, Utah Governor Spencer Cox confirmed to CNN.

The roommate was “a male transitioning to female,” Cox said, noting that “this partner has been incredibly cooperative, had no idea this was happening, and is working with investigators right now.”

Snip.

While officials have not yet released the name of the roommate, public records show that Lance Twiggs, a 22-year-old, reportedly in the process of transitioning from male to female, lives at the same address as Robinson. The Post reported that a family member of Twiggs confirmed they were living together.

Cox told the Wall Street Journal that the suspect was “deeply indoctrinated with leftist ideology.”

Robinson was also evidently a furry. So a gay tranny-loving furry killed Charlie Kirk. Some things are beyond parody…

“Anyone Who Blames ‘Both Sides’ After Charlie Kirk’s Murder Is A Liar And Coward.”

the Official Party of Wanton Assassination is busy making the case that there is extreme political violence “on both sides.” Immediately after the shooting, buffoonish Democrats like Hakeem Jeffries, Chuck Schumer, and Elizabeth Warren marched out to the microphones with convoluted messages about coming together and stopping violence on both sides.

By now, the drumbeat of bothsidesism in the aftermath of Kirk’s assassination has become a cacophony. “Bothsidesism” is what I am calling the irresistible urge for morally corrupt politicians (on both sides!) and journalists to lay half the blame for Kirk’s brutal murder at the feet of the right.

In fact, the worst Bothsiders — even worse than the sneering Democrats who can barely contain their glee that Kirk is dead, even as they scold us for not being interested in “unity” — are sniveling Republicans and so-called conservatives.

“There are monsters in your midst too,” intoned The New York Times’ David French, who persists in claiming to be conservative.

As proof, they will present their list of “right-wing violent attacks.” To give this barebones list more heft, they will go as far back as the Oklahoma City bombing, as that cretinous GOP Sen. James Lankford did on CNN. Lankford even had the gall to open his interview with Dana Bash by bringing up “white supremacy.” On Fox and Friends, Ainsley Earhardt tried to bait Trump into conceding that there are extremists on the right, too. Thank God he refused to take it.

This outrageous formulation must be crushed into dust, immediately. There is no moral equivalency. The Bothsiders are on the wrong side.

Why are Bothsiders wasting time blaming the right after a vicious murder committed by a leftist? Shouldn’t they be vociferously defending the innocent? The answer is that they’re cowards. They are too scared to call out Democrats for creating, supporting, and ignoring the evil that has taken root in their party.

Instead of courageously calling out their friends, colleagues, coworkers, and media allies, these pathetic Republican Bothsiders will spout long lists of examples of “right-wing political violence.” This allows them to avoid doing what has to be done: laying bare the left’s deep hatred of conservatives that has been allowed to fester for decade after decade.

By insisting that “both sides” are guilty of violence, they are giving the vicious left a way out. It’s a lifeline — a magical force field that immediately exonerates them. Democrats can then neatly avoid having to address the malevolent violence and hatred in so many of their voters. When it’s “both sides,” you get to escape accountability. When it’s “both sides,” the guilty get to escape a hard look in the mirror.

And just to belabor the point, here is why nearly everyone on the right is so united about political violence as a left-wing problem. First, Matt Walsh posted a short list of all the left-wing violence the right has had to endure in just the past few years:

BLM riots

Antifa

Church shootings

Trump assassination attempt [two of these!]

Pro life pregnancy center fires

Tesla vandalism

Attacks against ICE agents

Attacks against police

Attacks against federal courthouses

Allow me to add to this: multiple transgender shootings and threats by transgender activists. Plus, don’t any of these Bothsiders remember that our cities turned into a nightly warzone of fires, shootings, and Molotov cocktails from 2020-2021? It got so bad outside the White House that the president had to be moved to a secure location.

Don’t forget “Punch a Nazi” and “Punch a TERF” rhetoric either. Yes, men who identify as transgender, some of the most violent of the various Democrat shock troops, have attacked women as TERFs, or trans-exclusionary radical feminists, for years.

And we endure plenty of ancillary political violence. It was left-wing violence that forced Kyle Rittenhouse into a trial for self-defense. It was left-wing violence that forced Daniel Penny into a trial for being a hero. It was left-wing violence that wrecked countless statues, monuments, and businesses.

Just days after the assassination of Charlie Kirk, the left is working overtime to hide the truth and create fantasies about his death.

Specifically, leftists alleged that conservatives were going to “pounce” on the death to wage protests and boost radical agendas in the manner of what followed George Floyd’s death.

Here are some of the lies that such a ridiculous narrative entails.

One, Charlie Kirk is not conservatives’ George Floyd. There were no mass riots after his death of the sort that followed Floyd’s demise.

Floyd’s death was used by the left to justify five months of rioting, arson, murder, looting, and attacking police officers.

The postmortem respect for Kirk’s singular life was not characterized by $2 billion in property damage, the torching of a police precinct, a federal courthouse, and an iconic church, 35 deaths, and 1,500 injured law-enforcement officers.

Instead, thousands of people peacefully joined his Turning Point USA organization and promised to redirect their lives toward peaceful political engagement.

Two, after Kirk’s death, no prominent Republican or conservative is encouraging ongoing mass (and often violent) protests in the manner of high-profile leftists like Kamala Harris.

Snip.

Three, Charles Kirk was not George Floyd. He was a law-abiding, religiously devout, political organizer, happily married with two children. Kirk was a media figure and head of a huge 501(c)(3) nonprofit whose brand was calmly debating students who disagreed with him.

Floyd should not have died while in police custody. But Floyd’s comorbidities were many. When arrested, he was under the influence of fentanyl and methamphetamine, with a heart condition and recent Covid infection.

He was a career felon, with eight previous criminal convictions, who had in the past staged a violent home-invasion robbery and pointed a knife at the abdomen of one of the female occupants.

In contrast, when Kirk was killed, he was not on drugs. He was not resisting police officers. And he was not trying to pass counterfeit currency. Instead, he eschewed violence and tried to engage in polite dialogue with students of different views.

Four, Kirk was not, as alleged by the left, murdered by a right-wing shooter. His death was not an example of right-on-right violence. Just the opposite was true. The shooter, Tyler Robinson, was on record with his family expressing hatred for the conservative Kirk.

Robinson engraved his bullets with both Antifa-like “anti-fascist” messaging and transgender references. He lived with his transgender partner, who was a leftist. Robinson’s aim was to end Kirk’s peaceful conservative career because he hated his politics and popularity and feared his influence.

Five, the left used the death of Floyd to promote its hard-left and otherwise unpopular agenda—defunding the police, cashless bail, decriminalization of theft, and DEI mandates. It manipulated outrage, chaos, and months-long violence to ram through radical cultural and top-down legal changes that otherwise had little popular support.

“The Fake News Media, Democrats and Radical Left are Lying about Charlie Kirk. They use their lies to justify and excuse Charlie Kirk’s brutal murder and their culpability for it for winding up the radical leftist fringe with their violent rhetoric.”

Leftist political violence is on the rise with Fake News Media, Democrat politicians, activists and the far left using more and more radical, violent rhetoric. I wrote about the violent rhetoric (and leftist political violence) on this substack, several times (see also here and here). I also observed previously that the far left consider political violence a tool and that the violent rhetoric serves to “trigger” the radical leftist fringe into acting out violence. The visceral response Americans had to the brutal assassination of Charlie Kirk only days ago made the media, Democrats and their enablers “circle the wagons” and start fabricating lies and misinformation about Charlie Kirk. I debunk a couple of the nastier lies in this article.

Snip.

AT NO TIME did he say “black women” lack brain processing power. He said several prominent liberal women who admitted they were assisted by affirmative action were admitting they lacked the “brain processing power to be taken really seriously.”

The comments at issue were made on the July 13, 2023 episode of Charlie Kirk’s podcast. During the show, Charlie discusses affirmative action. Affirmative action was a particularly hotly debated topic at the time due to the United States Supreme Court’s decision in Students for Fair Admissions v. Harvard wherein SCOTUS found the use of race-based affirmative action programs at Harvard and the University of North Carolina violated the Equal Protection Clause of the 14th Amendment.

After the Supreme Court’s opinion in Harvard a number of prominent black Democrats publicly supported affirmative action and stated they were personally assisted in their careers by affirmative action. Among these were the late Sheila Jackson Lee, a Democrat Congresswoman from Texas, former First Lady Michelle Obama and former MSNBC correspondent Joy Reid.

Snip.

The Charlie Kirk Called for Stoning Gay People LIE

Literally hours after his murder, prominent leftists started circulating false claims that Charlie Kirk advocated for or supported stoning gay people to death. Chief among the purveyors of this misinformation was famous author (and radical leftist) Stephen King.

Snip.

Did Charlie Kirk “Advocate” for Stoning Gays?

No, of course not. In fact, Charlie Kirk advocated repeatedly for caring for gay people and encouraged and supported gay conservatives. (This link is to a gay conservative Charlie supported. His video is worth watching and includes video of Charlie Kirk answering questions from gay people.)

Charlie Kirk was a Christian and believed in the Bible. Based on Scripture, Charlie knew homosexuality was a sin. Naturally, this enraged the far left. To justify or excuse Charlie’s murder the far left FABRICATED the claim that Charlie Kirk “advocated” for “stoning gays.” All Charlie Kirk did was reference Scripture. Here is what happened.

Charlie Kirk and Jack Posobiec hosted a podcast called Thoughtcrime. During a Thoughtcrime episode on June 8, 2024, Jack and Charlie (along with a couple of other frequent conservative contributors to the show) discussed a social media personality named Miss Rachel and her endorsement of Pride month (gay pride). Miss Rachel’s social media and blogging content focuses largely on kids and parenting. Miss Rachel made a post about suppoting Pride month and invoked the Bible in the process, citing the admonitions on the Book of Matthew to “love your neighbor.” Miss Rachel implied, but did not expressly say, anyone who is against Pride Month, is not being a good Christian.

In response, Charlie Kirk pointed out you love someone by “. . . by telling them the truth and not by confirming or affirming their sin.” He then suggested Miss Rachel read the rest of the Scriptures and pointed out the Book of Leviticus calls for a man who lays with another man to be stoned, making the point Miss Rachel was cherry-picking Bible verses. He also pointed out the Bible says to love God, one must love his law and that the Book of Leviticus lays down God’s law about sex.

“Stephen King himself agreed his own post was untrue and apologized for the post.”

The Fake News Media, the Democrats and the left generally are in panic mode working to spread lies about Charlie Kirk in an effort to blunt public opinion against their radical, violent rhetoric and leftist violence. These two lies are the worst in my view. There are many more other lies being spread about Charlie Kirk by the left. Keep that in mind as you read any media reports.

Florida’s Commissioner of Education Anastasios Kamoutsas reminded teachers and administrators that they can be fired for violating the state’s code of ethics. “An educator who is designated with ensuring the health, safety and welfare of students in schools making comments celebrating violence at a school is very concerning.” (Hat tip: Stephen Green at Instapundit.)

More transtifa news: “The man who pleaded guilty to attempting to assassinate Supreme Court Justice Brett Kavanaugh identifies as a transgender woman, according to newly revealed court documents. In a recent court filing, Nicholas Roske’s defense attorneys call their client “Sophie” and explain in a footnote that they will use female pronouns to refer to him ‘out of respect.'”

A few years back we got really serious about studying cash transfers, and rigorous research began in cities all across America. Some programs targeted the homeless, some new mothers and some families living beneath the poverty line. The goal was to figure out whether sizable monthly payments help people lead better lives, get better educations and jobs, care more for their children and achieve better health outcomes.

Many of the studies are still ongoing, but, at this point, the results aren’t “uncertain.” They’re pretty consistent and very weird. Multiple large, high-quality randomized studies are finding that guaranteed income transfers do not appear to produce sustained improvements in mental health, stress levels, physical health, child development outcomes or employment. Treated participants do work a little less, but shockingly, this doesn’t correspond with either lower stress levels or higher overall reported life satisfaction.

Homeless people, new mothers and low-income Americans all over the country received thousands of dollars. And it’s practically invisible in the data. On so many important metrics, these people are statistically indistinguishable from those who did not receive this aid.

Read on for more detailed methodologies, but the results (or lack thereof) are consistent with all other experiments of this type, all the way back to the SIME/DIME experiments of the late 1960s. (Hat tip: Sarah Hoyt at Instapundit.)

The State Department announced Wednesday its decision to close the remnants of the Global Engagement Center, an office the Biden administration rebranded last year after it came under scrutiny for contributing to the censorship of conservatives online.

“The United States has ceased all Frameworks to Counter Foreign State Information Manipulation and any associated instruments implemented by the former administration,” principal deputy spokesperson Tommy Pigott said in a statement, referring to the Global Engagement Center’s new title.